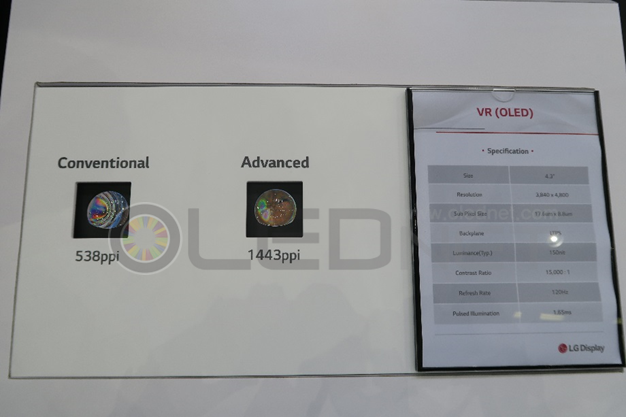

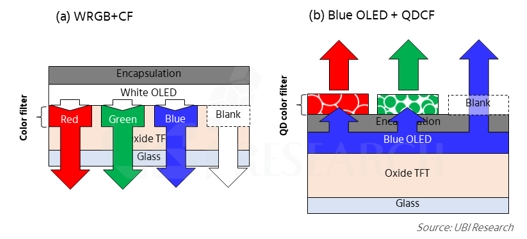

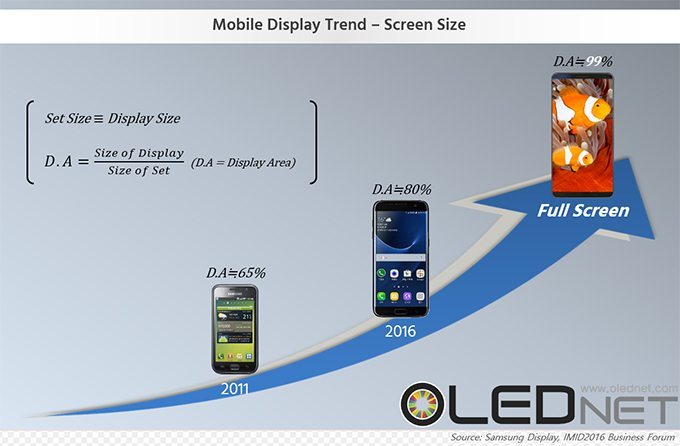

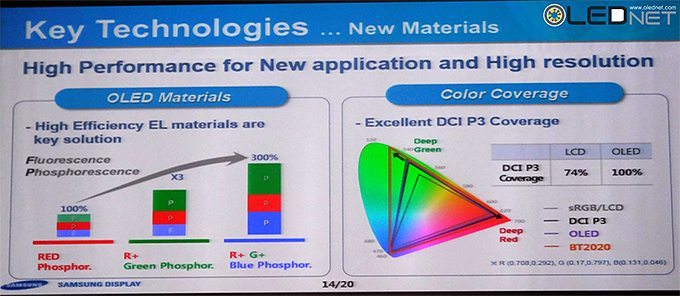

By adopting OLED display in virtual and augmented reality devices, which are leading the fourth industrial revolution in recent years, users can experience more realistic and lively images with faster response time, richer color and higher contrast ratio comparing to LCD.

OLED displays for virtual and augmented reality have been widely used in all industries including games, advertising, and education, and related applications have recently been actively pursued.

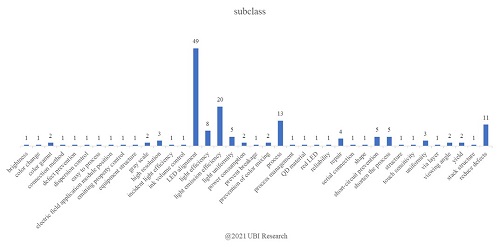

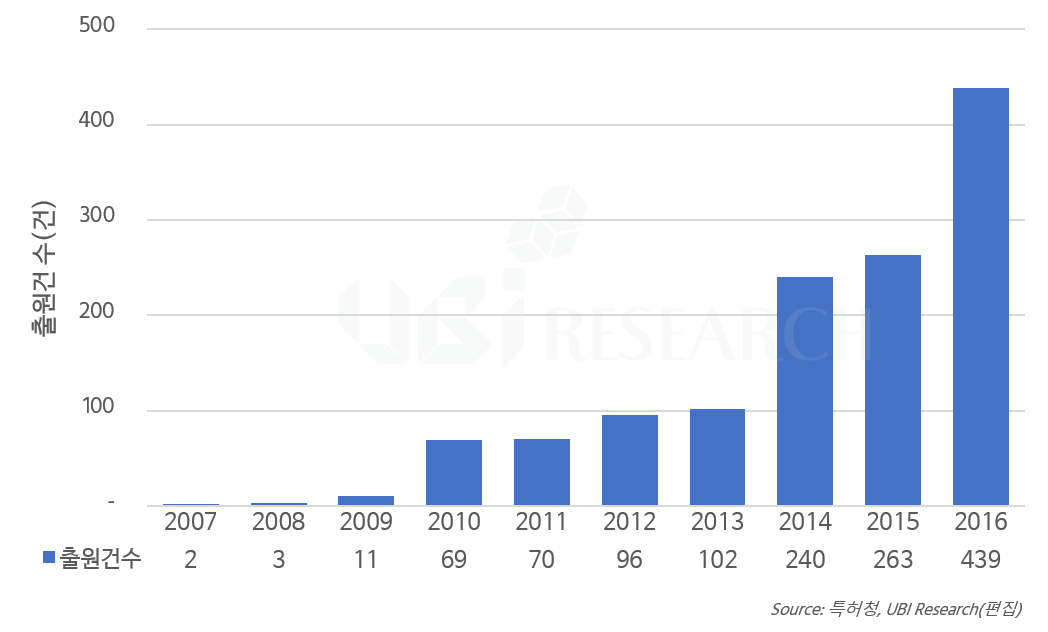

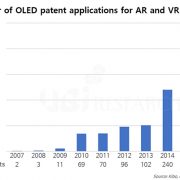

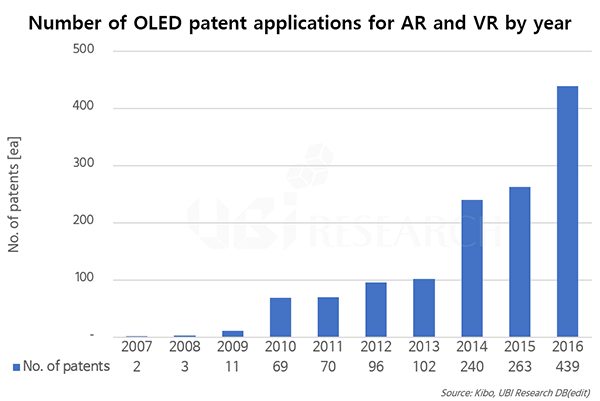

According to the Korean Intellectual Property Office (KIPO), the filing of OLED display for virtual and augmented reality is on an increasing trend each year, in particular, the number of related applications has greatly increased over the last 3 years.

<OLED display application trend for virtual and augmented reality, Source: Korean Intellectual Property Office>

According to the recent filing status by year, there are 240 applications in 2014, 263 in 2015, and 439 in 2016, and applications for OLED display technologies for virtual and augmented reality have increased rapidly from 2014.

The reason for the recent increase in applications for virtual and augmented reality OLED display fields is that the development of various conditions such as resolution, response time, usability, comfort, and price is required as a preliminary task for popularization of virtual and augmented reality devices and OLED displays can realize realistic images and are easy to design with flexibility, which is why they can meet these needs much better than existing LCDs.

Also, given the prospect that the virtual and augmented reality market will increase to about $ 80 billion by 2020, OLED displays suitable for virtual and augmented reality devices are being developed in various forms such as flexible, rollable, bendable, and stretchable displays, and it is expected that applications for OLED display technology for virtual and augmented reality will continue to increase accordingly.

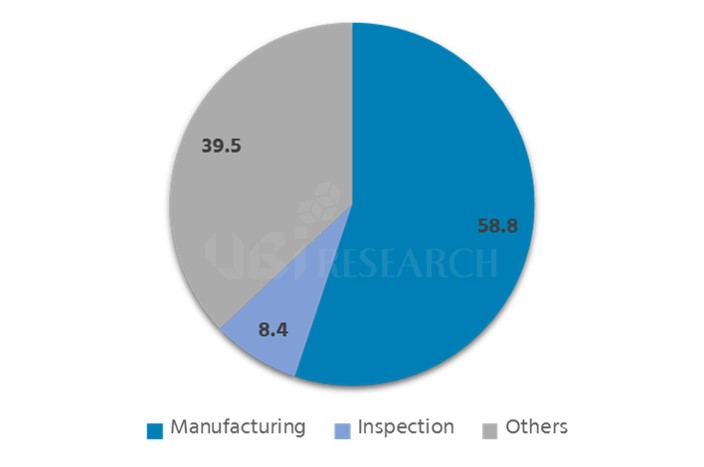

For the filing status of OLED display technology for virtual and augmented reality (2007 ~ 2016), there are 774 cases (60%) of large companies, 142 cases (11%) of medium and small-sized companies, 72 cases (6%) of universities and research institutes, 70 individual cases (5%) 237 foreigner cases (18%).

By major application companies, 465 cases of LG Electronics, 216 cases of Samsung Electronics, 51 cases of Microsoft Corporation, 29 cases of Samsung Display, 20 cases of SK Planet, 17 cases of Qualcomm, 17 cases of LG Display, It can be seen that related technology is dominated by domestic companies.

As for the status of OLED display application field for virtual and augmented reality applications, there are 426 cases of personal entertainment (game, theme park, experience), 169 cases of defense (war simulation, weapons development, fighter pilot), 141 cases of advertisement, 131 cases of medical treatment (3D simulation, virtual endoscopy, simulation), 123 cases of healthcare, 117 movies, etc., indicating that OLED display technologies for virtual and augmented reality are most actively used in the game and defense industries.

“OLED displays, which are developed mainly for personal use products such as TVs and mobile phones, are expected to expand into new industries as well as virtual and augmented reality based on their superior image presentation capabilities,” said Kim Jong-Chan, head of the screening team in the Korean Intellectual Property Office (KIPO). In addition, we expect to see increased applications related to technologies to address performance improvement challenges, such as extending the life of OLED displays and extending the operating temperature range. “.

In order to strengthen the patent competitiveness of OLED display field, KIPO has regularly held “IP Together” event as part of communication and cooperation between industry and patent office, and will continue to provide related information through the “Revised Patent Law Seminar”.

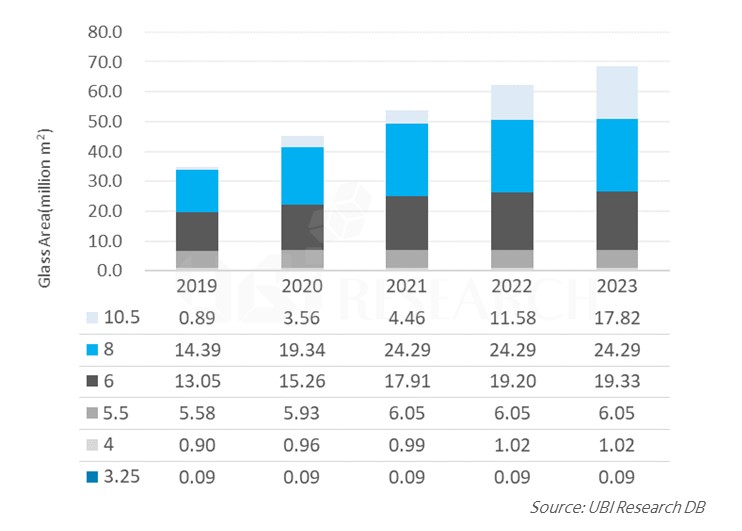

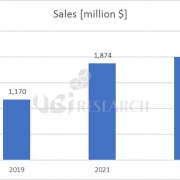

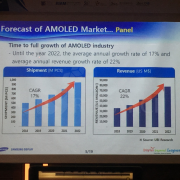

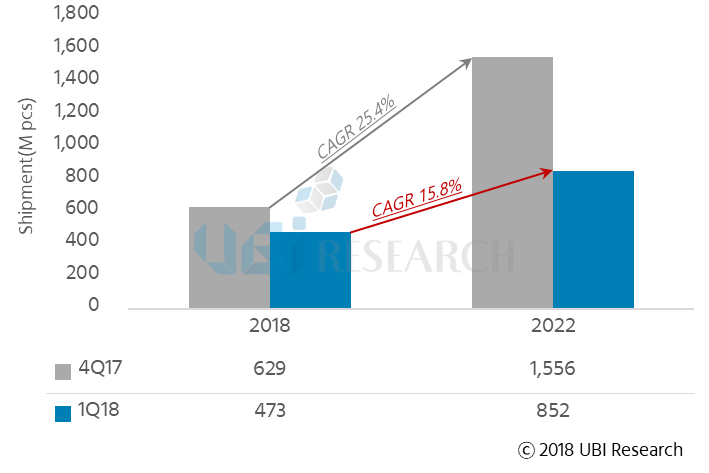

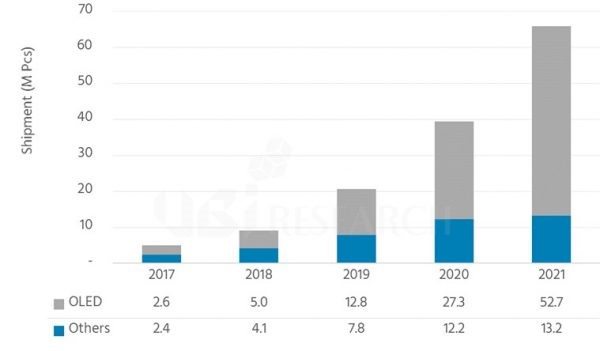

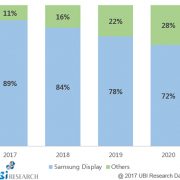

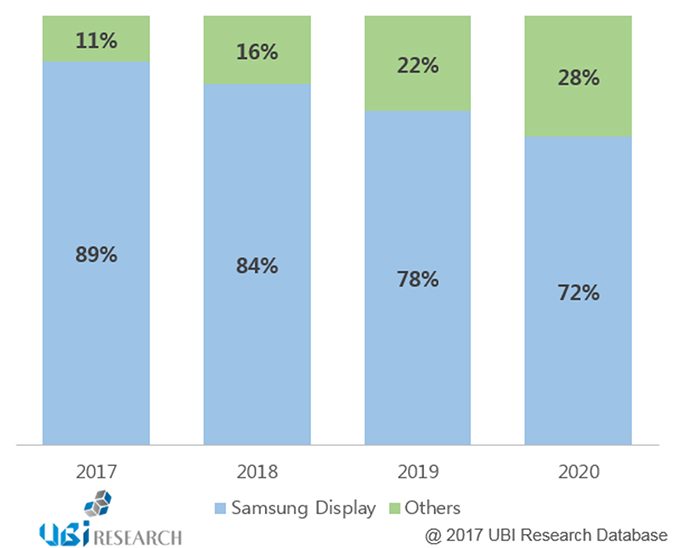

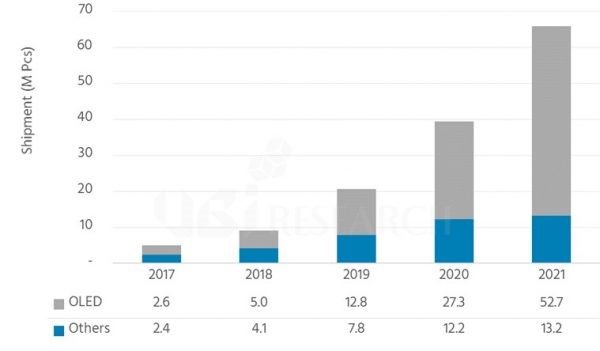

On the other hand, according to the ‘Display Market Report for AR and VR’ published by UBi Research, OLED for AR and VR are expected to be shipped by 2.6 million units in 2017, accounting for 52% of the market share and 52 million units in 2021 accounting for 80% of the market share.

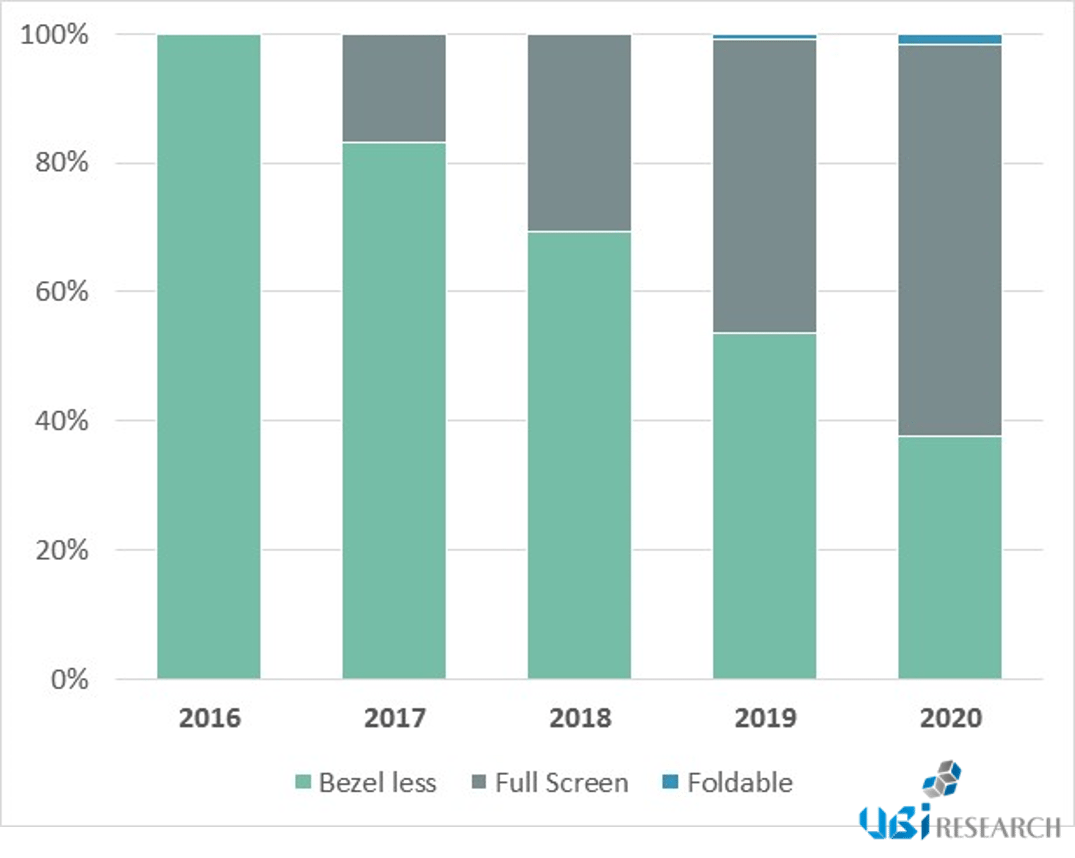

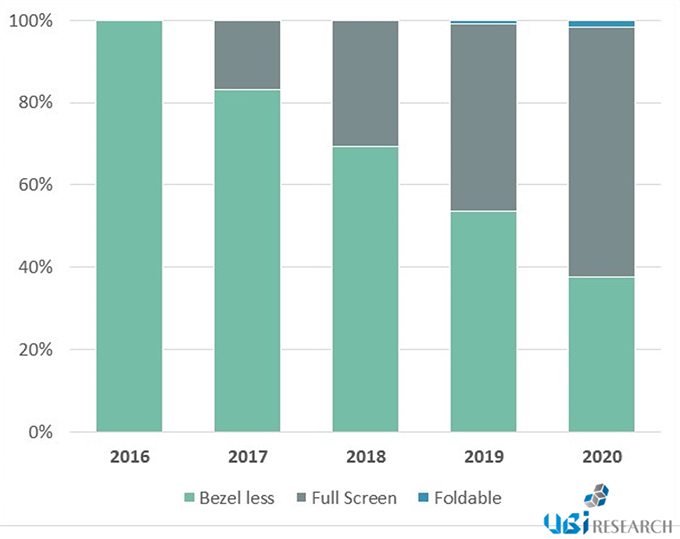

<Shipment forecast by display type for AR and VR, Source: UBI Research>