[Light building 2016] Osram OLED Rear Lamp

Osram is showcasing its OLED rear lamp for cars at Light+Building 2016

Osram is showcasing its OLED rear lamp for cars at Light+Building 2016

LG Display is showcasing its latest advanced OLED light products and solutions at Light+Building 2016

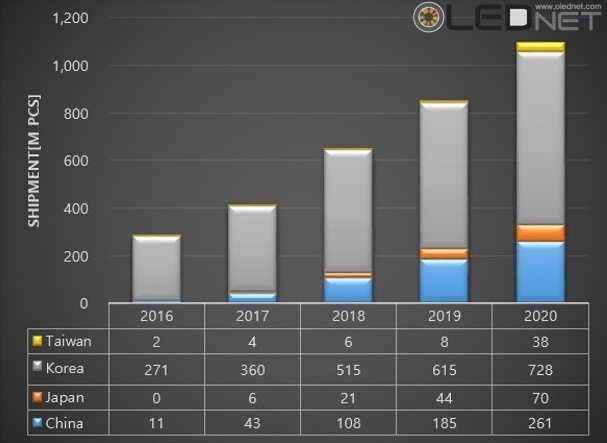

2016-2020 Global AMOLED Panel Market Shipment [1 Million] (source : UBI Research)

This year, Korea is expected to secure overwhelming leadership position within the global AMOLED panel market with 95% market share.

According to 2016 OLED Display Annual Report, recently published by UBI Research, approximately 270 million units of AMOLED panel are to be produced from Korea in 2016, approximately 95% of the global shipment.

For AMOLED panel market revenue, Korea is estimated to occupy 96% of the total market in 2016 with US$ 14,218 million. Korea is expected to maintain approximately over 70% of the market share until 2020, and lead the global market for several more years.

This is analyzed to be due to active response by Korean display companies against AMOLED application expansion by influential global smartphone companies.

Samsung Electronics is forecast to sell over 47 million units of AMOLED panel equipped Galaxy series in 2016. The projection that Apple will also apply AMOLED panel to future iPhone series for product differentiation is gaining traction.

Several companies, including LG Display and Samsung Display, are carrying out active investment for AMOLED panel mass production line from H1 2016.

Other than Korea, China is showing rapid movement within the global AMOLED market. China is estimated to produce approximately 11 million units of AMOLED panel in 2016, and occupy approximately 4% of the global shipment, marking the second place after Korea’s 95%. China is estimated to increase the market share each year and reduce the gap with Korea; in 2020, China is expected to hold 24% of global AMOLED panel shipment in 2020.

China’s AMOLED panel market revenue is also forecast to show significant growth with approximately US$ 500 million in 2016 to US$ 13,700 million in 2020, a 20% of the total market.

2016 OLED Display Annual Report forecasts that the global AMOLED market is to record approximately US$ 15,000 million in 2016, and grow to approximately US$ 70,000 million in 2020.

2016년~2020년 AMOLED 시장 출하량(출처:유비산업리서치 2016 OLED Display Annual Report)

올해 전세계 AMOLED 패널 시장은 한국이 95%의 점유율을 차지하며 압도적인 주도권을 확보할 전망이다.

유비산업리서치에서 최근 발간한 ‘2016 OLED Display Annual Report’에 따르면 2016년 한국에서 생산될 AMOLED 패널의 양은 약 2억7천만개로 전세계 출하량의 약 95%를 차지할 것으로 예상된다.

AMOLED 패널 시장 매출액 역시 한국이 2016년 미화 142억1800만달러로 전체시장의 96%를 차지할 전망이며 오는 2020년까지 약 70% 이상의 시장 점유율을 유지, 향후 수년 이상 세계 시장 주도권을 쥘 것으로 보인다.

이는 글로벌 유력 스마트폰 업체들의 AMOLED 적용 확대에 대해 국내 디스플레이 업계가 적극 대응하고 있기 때문인 것으로 분석된다.

삼성전자는 2016년 AMOLED 패널이 적용된 갤럭시 시리즈를 4,700만대 이상 판매할 것으로 전망된다. 애플 역시 제품 차별화를 위해 향후 아이폰 시리즈에 AMOLED 패널을 적용할 것이라는 예상이 우세한 상황이다.

LG디스플레이, 삼성디스플레이 등은 이 같은 수요에 대비하기 위해 2016년 1분기부터 AMOLED 패널 양산 라인 투자에 본격적으로 나서고 있다.

한국을 제외하고 전세계 AMOLED 시장에서 가장 빠른 행보를 보이는 국가는 중국이다. 중국은 2016년 AMOLED 패널을 약 1,100만개 생산, 전세계 출하량의 약 4%를 차지할 전망이며 95%인 한국에 이어 2위에 오를 전망이다. 중국은 매해 점유율을 늘려가며 오는 2020년에는 전세계 AMOLED 패널 출하량의 24%를 차지, 한국과의 격차를 줄여나갈 것으로 보인다.

중국의 AMOLED 패널 시장 매출액도 2016년 미화 약 5억달러에서 2020년 137억달러로 20%의 글로벌 점유율을 차지하며 큰 폭의 성장세를 그릴 것으로 예상된다.

한편 유비산업리서치의 본 보고서에 따르면 2016년 글로벌 AMOLED 시장은 미화 약 150억달러 규모를 형성하고 오는 2020년에는 약 700억달러 규모로 성장할 전망이다.

Japan Display (JDI) officially announced OLED mass production. The press, including the Sankei Shimbun and the Nikkei, reported that on January 22 JDI revealed their plans to begin mass production of OLED panel to be used in smartphone from 2018.

JDI continued development with the aim of LTPS TFT and WRGB OLED technology applied high resolution AMOLED panel mass production for mobile device, and revealed the results through exhibitions in recent years.

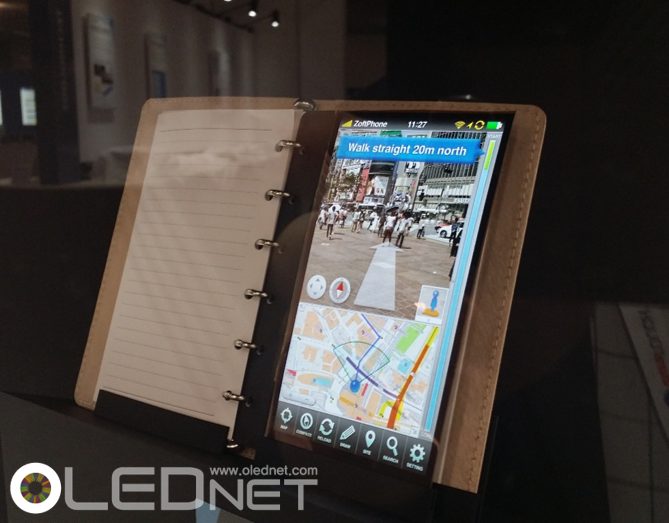

In Display Innovation 2014 (FPD International) and SID 2015, JDI have presented 5.2 inch FHD flexible AMOLED panel. Particularly, in SID 2015, JDI showed a notepad equipped with flexible OLED panel.

JDI is likely to mass produce flexible AMOLED following the current mobile device market trend. Although the mass production technology was not mentioned, due to the client demands, it is estimated that either the RGB method, which is being used by LG Display and Samsung Display, or WRGB method, which is being developed by JDI, will be selected.

At present, only Samsung Display and LG Display can mass produce flexible AMOLED panel, but Chinese companies are fast in pursuit. There is much interest in how this JDI’s mass production announcement will affect the future OLED market.

Japan Display(JDI)가 OLED 양산을 공식화했다. 산케이신문, 니케이산업신문 등 외신에 따르면 JDI는 1월 22일 JDI기술전시회에서 오는 2018년부터 스마트폰에 적용될 OLED 패널 양산을 시작하겠다고 밝혔다.

JDI는 LTPS TFT와 WRGB OLED 기술을 적용한 고해상도의 mobile device용 AMOLED panel 양산을 목표로 하고 개발을 지속해왔으며 최근 몇 년간의 전시회를 통해 그 성과를 공개했다.

JDI는 Display Innovation 2014(FPD International)와 SID2015에서 5.2inch FHD flexible AMOLED panel을 전시하였으며 특히 SID2015에서는 flexible OLED panel를 수첩에 적용해 공개한 바 있다.

JDI는 현재 mobile 기기용 시장의 트랜드에 따라 flexible AMOLED 양산이 유력하며, 양산기술에 대해서는 언급을 하지 않았지만 고객사의 요청에 따라 현재 LG디스플레이와 삼성디스플레이가 사용하는 RGB방식 또는 JDI가 개발중인 WRGB 방식 중 선정 될 것으로 예상된다.

현재 flexible AMOLED panel을 양산할 수 있는 업체는 삼성디스플레이와 LG디스플레이가 유일하지만 중국 업체들이 빠르게 추격해오고 있는 추세이며, 이번 JDI의 양산 발표가 앞으로의 OLED시장에 어떤 영향을 미칠지 많은 관심이 모아지고 있다.

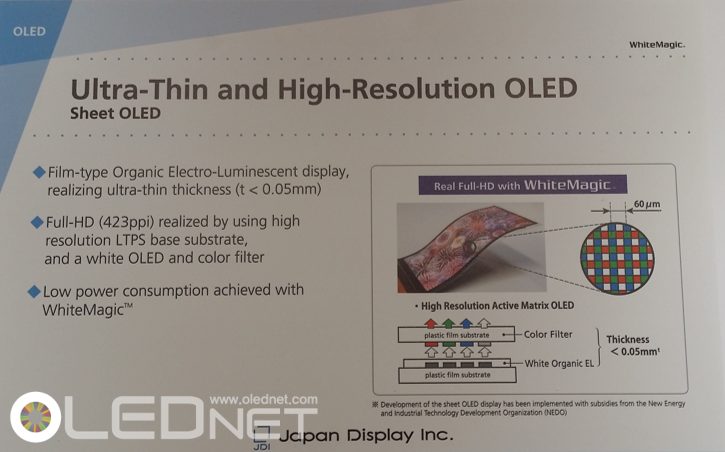

JDI’s 5.2inch FHD flexible AMOLED panel, SID 2015

The 3rd section of the 1st OLED Frontier Forum (Jan 28), OLED’s Future, held a panel discussion with government, industry, and academia experts discussing OLED industry development strategy, such as next generation technology development, convergent areas, and personnel training, and future forecast. OLEDNET summarized the answers that each expert gave to the questions of the panel chair (Professor Changhee Lee, Seoul National University).

Jun-hyung Souk (Professor, Sungkyunkwan University)

For SDC mobile, as the OLED depreciation is ending the OLED production cost is becoming almost the same as LCD. If OLED related experts stay within Korean industry as well as the technology, Korea can continue to lead for 4-5 years. In order to achieve the continued leadership, differentiation through flexible R2R has to be carried out, as well as the materials and encapsulation technology development.

Sung-Chul Kim (CTO, SDC)

As a-Si is an existing technology, there is no room for further advancement. Sharp’s difficulty in panel business is due to lack of technology research on the panel. Because one technology can only be used for approximately 7 months, diverse technology development is required.

In-byeong Kang (CTO, LGD)

Fast organizations cannot but win. Therefore, rapid change to OLED from LCD is needed. As difficult is the technology, cooperation between academia and industry is needed. Now is the time when this cooperation for next generation technology development is more in demand. LGD is putting in much effort for OLED profitability.

Sung-Jin Kim (Vice President, Toray Advanced Materials Korea)

Cooperation between materials and manufacturing equipment companies is important in solution process materials development. Particularly, how to control dry process is an important issue. Also, Kim expects the current solution process materials development to show tangible results in 3-5 years.

Junyeob Lee (Professor, Sungkyunkwan University)

Solution process is favorable for materials optimization. From the initial concentration on polymer materials, recently small molecule materials focused soluble materials development is being carried out, and how to implement common layer is an issue. Emitting layer is using the small molecule materials that are being used as evaporation materials. The difference is the higher cost as the solvent is used. Also, as there is an issue (formulation problem) when used in large area, solution is required.

Kyoung-Soo Kim (Vice President, Korea Display Industry Association)

Expert acquirement is a key issue. Through upgraded cooperation between industry and academia, and industries, cooperation between panel, manufacturing equipment, and materials has to progress into a positive cycle. Also the open platform regarding new OLED application is needed.

Young-Ho Park (PD, Korea Evaluation Institute of Industrial Technology)

Flexible display competitiveness acquirement is a big concern. Programs for challenging R&D, and high added value product/technology development, and R&D infra establishment (highly cost-effective R&D) have to be considered.

Sung-Chul Kim, Samsung Display’s CTO, at the 1st OLED Frontier Forum (Jan 28) gave a presentation ‘AMOLED Technical Issue and Future’ and discussed OLED technological issues of the past and present.

Kim pointed out the fact that glass substrate is not always necessary for OLED as the most different factor compared to LCD, and emphasized flexible OLED where plastic substrate is used. Kim reported that flexible OLED issues include window’s durability and coating, touch panel’s electrode materials and flexibility, reduction of number of encapsulation layers and flexibility, and backplane’s low stress structure and OTFT application. He revealed that developing spherical stretchable display, which the user can zoom in, is also included in the product roadmap.

Regarding transparent/mirror display, Kim announced that this is the direction that OLED should head toward and added that layout design development suitable for different application areas is needed. Specifically, the transparent display should be developed to increase the transmittance area and decrease the TFT area, and the mirror display to optimize the ratio between the total reflection and half-reflection areas.

Additionally, in order to produce high resolution OLED, Kim mentioned that innovation in terms of pixel operation and backplane structure is needed. He emphasized compensation circuit and that whether high resolution display can be manufactured cheaply and using simple structure is the key.

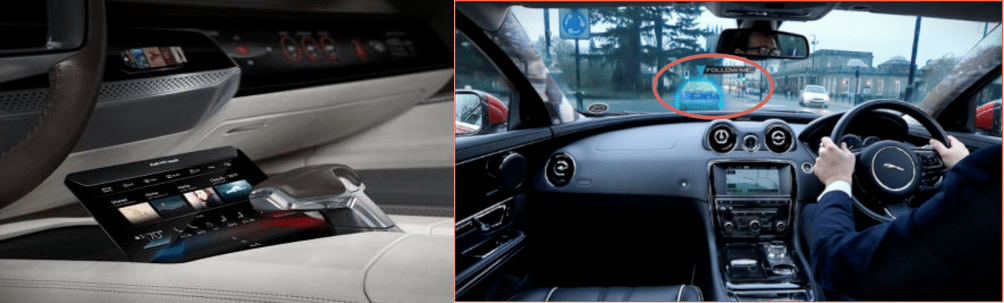

Kim discussed wall display, IoT, educational display, etc. as the new applications which will become important in future. Particularly, mentioning the automotive display area, Kim explained that for OLED to enter these new areas, plastic materials suitable for each applications and technology that can correctly process this are required. In order for this type of research development to be carried out smoothly, Kim added that cooperation between the academia and industry is necessary.

제 1회 OLED Frontier Forum의 제 3부 ‘OLED 미래’에서는 정부, 업계, 학계 전문가들이 참석한 가운데, 차세대 기술개발, 융복합 분야, 인력양성 등 OLED 산업 발전 전략과 미래 전망에 대한 패널 토론이 진행되었다. OLEDnet에서는 사회자(이창희 교수, 서울대)의 질문에 대한 각 분야별 전문가들의 답변 내용을 요약하였다.

석준형 교수 (성균관대)

SDC Mobile의 경우 OLED의 감가상각이 끝나가기 때문에 OLED의 원가는 LCD와 거의 같아지고 있다. OLED관련 전문 인력만 빼앗기지 않으면 4~5년은 한국이 주도해나갈 수 있다.(Black Box화 전략) 지속적인 주도권 확보를 위해 flexible R2R로 차별화를 해야하며, 이와 더불어 소재와 encapsulation쪽 기술개발 필요하다.

김성철 CTO (SDC CTO)

a-Si는 기술적 차별성이 없다. Sharp의 panel 사업이 어려움을 겪은 이유는 panel에 대한 기술연구를 하지 않았기 때문이다. 한가지 기술로는 7개월 밖에 못 가기 때문에 다양한 기술에 대한 개발이 필요하다.

강인병 CTO (LGD CTO)

빠른 조직이 이길수 밖에 없다. 따라서 LCD에서 OLED로의 빠른 전환이 필요하다. 기술이 어려운만큼 산학연의 협력이 필요하며, 차세대 기술개발에 대한 산학연의 협력이 더욱 필요한 시점이다. LGD는 OLED 흑자를 위해 열심히 노력하고 있다.

김성진 전무(도레이 첨단 소재)

소재 업체와 장비 업체의 협력이 용액공정 재료 개발 시 중요하며 특히 Dry process를 어떻게 control을 할 것이냐가 중요한 이슈이다. 또한 현재의 용액공정 재료 개발은 3 ~ 5년 정도면 가시적인 결과를 볼 수 있으리라 판단한다.

이준엽 교수 (성균괸대)

용액공정이 재료 최적화에 유리하다. 초기 고분자 위주에서 최근에는 저분자 위주의 soluble 재료 개발이 이루어지고 있으며 공통층을 어떻게 가져가느냐에 대한 이슈가 있다. 발광층은 현재 증착 재료로 사용되고 있는 저분자 재료를 그대로 사용하고 있으며 차이점은 용매를 사용하기 때문에 가격 측면에서 현재는 비싸다는 이슈가 있으며, 또한 대형화 시 문제점(formulation 문제)이 있어 이에 대한 해결이 필요하다.

김경수 부회장(디스플레이 산업 협회)

전문인력 확보가 관건이며, 산학연 or 기업간 협력을 upgrade 시켜 panel-장비-소재간의 협력이선순환관계로 발전되어야 한다. 또한 새로운 OLED 응용분야에 대한 open platform이 필요하다.

박영호 PD(한국 산업기술평가 관리원)

Flexible 디스플레이 경쟁력 확보에 대한 고민이 크다. 도전적 R&D를 위한 program과 고부가가치의 상품/기술 개발, R&D infra 구축(가성비 높은 R&D)에 대해 깊은 고민을 해야 한다.

제1회 OLED Frontier Forum에서 삼성디스플레이의 김성철 CTO는 ‘AMOLED Technical Issue and Future’라는 제목으로 OLED의 과거와 현재의 기술적인 이슈에 대해 점검하는 시간을 가졌다.

김성철 CTO는 OLED가 LCD에 비해 가장 차별화되는 점으로 꼭 glass 기판이 필요하지 않다는 것을 꼽으며, plastic 기판이 적용되는 flexible OLED에 대해 강조하였다. 김성철 CTO는 “플렉시블 OLED에 대한 이슈로 window의 내구성과 코팅, 터치패널의 전극 재료와 flexibility, encapsulation의 layer수 감소와 flexibility, backplane의 저stress 구조와 OTFT 적용이 있다.”고 발표하며 사용자가 관심있어 하는 부분을 확대하여 볼 수 있도록 구 형태의 stretchable 디스플레이를 개발하는 것까지 제품 로드맵이 되어 있다고 밝혔다.

김성철 CTO는 투명/거울 디스플레이와 관련해서는 앞으로 OLED가 발전해 나아가야 할 길이라고 밝히며 각 응용 분야에 알맞은 layout design 개발이 필요하다고 이야기하였다. 이에 대해 “구체적으로 투명 디스플레이는 투과부가 높아지고 TFT 면적이 낮아지는 방향으로, 거울 디스플레이는 전반사와 반반사 부분의 비율을 최적화하는 방향으로 개발되어야 한다.”고 발표했다.

또한 고해상도 OLED를 제작하기 위해서는 pixel 구동과 backplane 구조 측면에서 혁신이 필요하며, 특히 보상회로를 강조하며 ‘고해상도 디스플레이를 저렴하고 단순한 구조로 만들 수 있는가’가 핵심이라고 밝혔다.

미래에 중요하게 될 새로운 application으로 김성철 CTO는 wall 디스플레이, IoT, 교육용 디스플레이 등이 있다고 발표했다. 특히 차량용 디스플레이 분야를 언급하면서 OLED가 이런 신규 분야에 진출하기 위해서는 각 application에 알맞은 플라스틱 재료와 이를 제대로 가공할 수 있는 기술이 필요하며, 이러한 연구 개발이 원할히 진행되기 위해서는 산학연 연계가 필수적이라고 밝혔다.

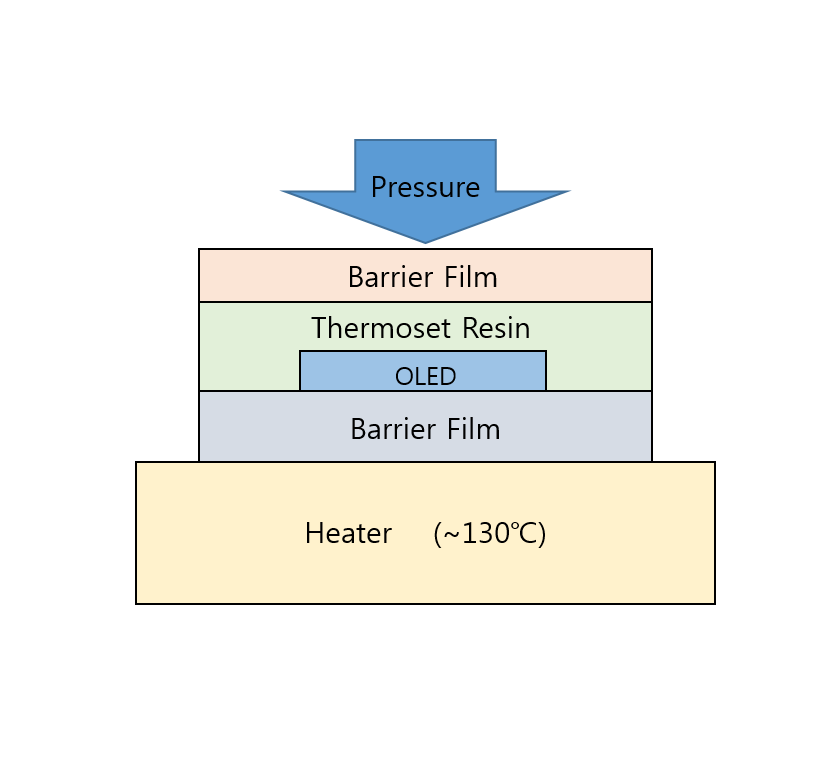

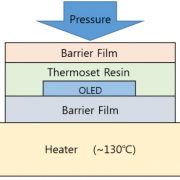

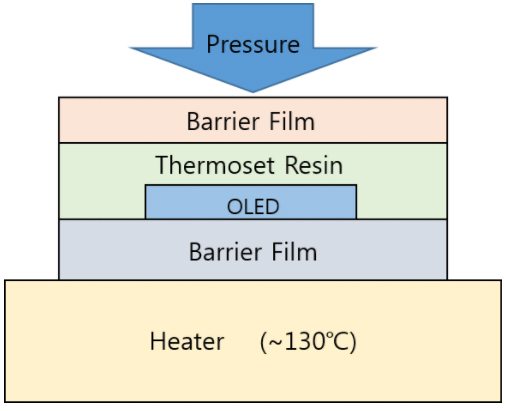

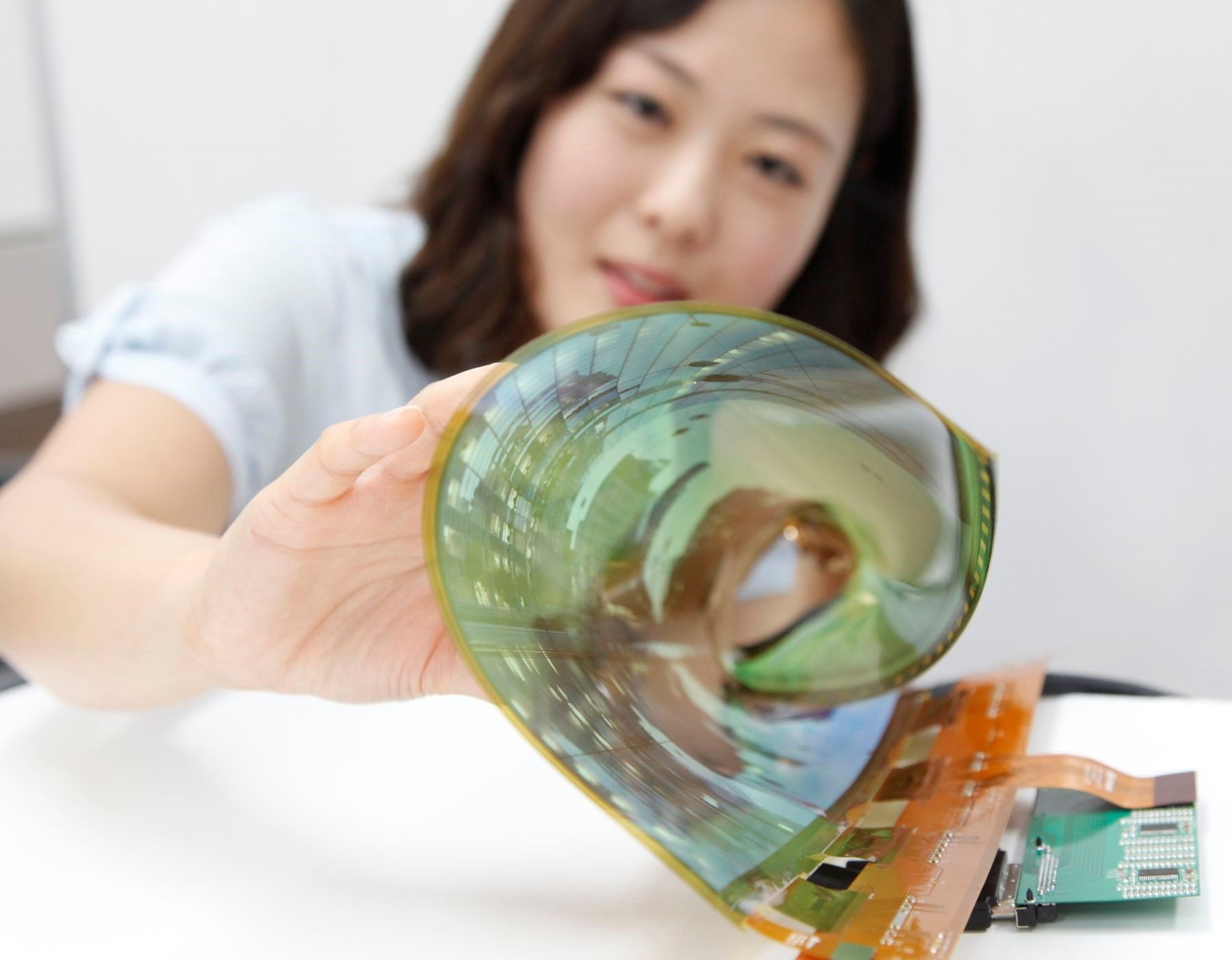

Innovation Center for Organic Electronics in Yamagata University in Japan discussed low cost flexible OLED encapsulation in Lighting Japan 2016 conference. Existing flexible OLED encapsulation mainly used hybrid encapsulation structure that forms multi-layer thin film passivation layers on top of OLED, and then applying adhesive organic material and laminating gas barrier film. The encapsulation structure presented by Yamagata University forms, of the hybrid encapsulation structure, thermoset resin and barrier film above OLED without multi-layer thin film passivation, and laminate at approximately 130 °C. Yamagata University announced that they were successful in transparent flexible OLED panel development on January 13 using encapsulation, and that this panel will be presented in Printable Electronics 2016 in Tokyo from January 27.

The OLED panel to be exhibited is a leaf shaped of 45 mm width, 110 mm length, weighs less than 1.2g, and 250 um thick transparent film substrate that can be folded.

According to Yamagata University, if the newly developed encapsulation is applied, the OLED lighting panel price can be reduced as passivation layer is not used. Also, Yamagata University revealed as it can satisfy both transparent and flexible categories simultaneously, it is estimated that it will become a key technology in future transparent flexible OLED lighting development.

Low Cost Flexible OLED Encapsulation, Yamagata University

일본 야마가타 대학에 있는 유기 전자 혁신 센터의 OLED 그룹은 Lighting Japan 2016의 conference에서 저비용 flexible OLED용 encapsulation에 대해 발표하였다. 기존 flexible OLED의 encapsulation은 OLED위에 한층 이상의 다층 박막 passivation layers를 형성한 후 adhesive organic material을 도포하고 gas barrier film을 laminating 하는 하이브리드 encapsulation 구조가 주로 사용되었었다. 이번에 야마가타 대학에서 발표한 encapsulation 구조는 하이브리드 encapsulation 구조에서 다층 박막 passivation 없이 thermoset resin과 barrier film을 OLED 위에 형성한 후 약 130도의 온도로 합착한다. 야마가타 대학은 encapsulation을 사용하여 지난 13일 ‘투명 플렉시블 OLED 패널’ 개발 및 프로토 타입에 성공했다고 발표 했으며, 이 패널은 27일부터 도쿄 빅사이트에서 열리는 ‘인쇄 전자 전시회 2016’에서 전시할 계획이라고 밝혔다.

전시될 OLED 패널은 폭 45mm, 길이 110mm의 나뭇잎 형태로 무게는 1.2g보다 가벼우며, 두께는 250um의 투명한 필름 기판으로 접을 수 있다.

야마가타 대학에 따르면, 새로 개발한 encapsulation을 적용하면 passivation layer를 사용하지 않아 OLED lighting panel의 가격을 낮출 수 있으며 투명과 플렉시블을 동시에 충족시킬 수 있기 떄문에 앞으로의 투명 플렉시블 OLED lighting 개발에 핵심 기술이 될 것으로 예상한다라고 밝혔다.

저비용 flexible OLED용 encapsulation, 야마가타 대학

On January 6 (local time), LG Display held a press conference with key board members in attendance including CEO Sang-Beom Han, CTO In-Byeong Kang, and head of marketing Young-Kwon Song.

At this conference, unlike previously, Han conveyed strong determination and announced LG Display will invest in future large area display with OLED. This was a conviction never seen before.

The evidence of the confidence could be read at the exclusive exhibition. OLED TV achieved 800 nit, 150% higher than UHD Alliance’s standard of 540 nit.

With transparent OLED, LG Display reached leading specs. The WRGB OLED structured transparent OLED has 40% transmittance and 600 nit of brightness through the application of the 800 nit OLED technology.

Flexible OLED also was significantly different from last year. In 2015, the comparison between LG’s OLED and LCD for automotive dashboard display showed OLED to be lacking in brightness. However, this year’s exhibition showed OLED panel to have similar level of brightness as LCD and exceeding LCD’s spec with deeper black.

The exhibition showed rapid development of LG Display’s OLED technology.

LG 디스플레이는 한상범 부회장과 CTO 강인병 전무, 전략마케팅 송영권 전무등 주요 경영진이 참석한 가운데 기자 간담회를 개최했다.

이번 기자 간담회는 이전과 달리 한 부회장은 매우 강한 의지를 표명했다. “LG디스플레이는 향후 대면적 디스플레이는 OLED로 투자합니다!” 이제까지 본적 없는 소신이었다.

한 부회장의 자신감은 특별 전시장에서 읽을 수 있었다. OLED TV는 800nit를 달성했다. UHD Alliance 규격의 540nit 보다 이미 150%를 초과 달성했다.

투명 OLED에서는 챔피언 스펙을 달성했다. WRGB OLED 구조를 적용한 투명 OLED는 40% 투과율에 휘도는 600nit 이다. 800nit OLED 기술을 적용했기 때문이다.

Flexible OLED도 작년과는 매우 달랐다. 작년에 LG가 전시한 자동차 dashboard용 OLED와 LCD를비교하면 휘도가 부족한 단점이 보였지만 이번 전시장의 OLED 패널은 LCD와 휘도가 동등 수준이며 깊은 black으로서 LCD의 spec을 능가했다.

LG디스플레이의 OLED 기술이 급 진전하고 있음을 보여주었다.

Choong Hoon Yi, Chief Analyst, UBI Research

BOE is intending to carry out a large amount of investment in order to operate Gen10.5 LCD line from 2018. Meanwhile, key set makers including Apple, Samsung Electronics, LG Electronics, and Panasonic are devising strategy to move from LCD to OLED for smartphone and premium TV displays. As such, it is becoming more likely for the LCD industry to be in slump from 2018.

At present, the area where LCD industry can create profit is LTPS-LCD for smartphone. The forecast smartphone market for this year is approximately 15 billion units. Of this, Samsung Electronics and Apple are occupying 20% and 15% of the market respectively. OLED equipped units are less than 2 billion.

However, from 2018 the conditions change greatly. Firstly, Apple, which has been using LCD panel only, is estimated to change approximately 40% of the display to OLED from 2017 earliest and 2018 latest. Apple is testing flexible OLED panels of JDI, LG Display, and Samsung Display, and recommending them to invest so flexible OLED can be applied to iPhone from 2017. The total capa. Is 60K at Gen6. As new investments for Gen6 line of Samsung Display and LG Display are expected to be carried out from 2016, supply is theoretically possible from 2017.

Source: UBI Research Database

If 5inch flexible OLED is produced from Gen6 line, under the assumption of 50% yield at 60K capa. 65 million units can be produced annually, and approximately 1 billion units if the yield is 80%. If Apple’s iPhone shipment in 2017 is estimated to be around 2.7 billion units, within the 50-60% yield range approximately 25% of the display is changed to OLED from LCD, and if yield reaches 80% around 40% will change. The companies that are supplying Apple with LCD for smartphone, LG Display, JDI, and Sharp, are expected to show considerable fall in sales and business. These 3 companies could be reduced to deficit financial structure just from Apple’s display change

Furthermore, as Apple is not producing low-priced phones, under the assumption that future iPhone could all have OLED display, Apple could cause the mobile device LCD industry to stumble after 3 years.

Samsung Electronics also is gradually changing Galaxy series display to OLED from LCD. Of the forecast 2015 shipment of 3 billion units, 50%, 1.5 billion units, has OLED display, but Samsung Electronics is expected to increase flexible OLED and rigid OLED equipped products in future. Particularly, as Apple is pushing for flexible OLED application from 2017, Samsung Electronics, whose utilizing OLED as the main force, is estimated to increase flexible OLED usage more than Apple. It is estimated that all Galaxy series product displays will be changed to OLED from 2019.

Under these assumptions, of the estimated smartphone market in 2020 of approximately 20 billion units, Samsung Electronics and Apple’s forecast markets’ 7 billion could be considered to use OLED.

Samsung Display is strengthening supply chain of set companies using their OLED panels. Samsung Display is supplying OLED panels to diverse companies such as Motorola and Huawei as well as Samsung Electronics, and also expected to supply rapidly rising Xiaomi from 2016. If smartphone display is swiftly changed to OLED from LCD from 2017, Chinese display companies that are currently expanding TFT-LCD lines are to be adversely affected.

Additionally, in the premium TV market, LG Electronics mentioned that they will focus on OLED TV industry at this year’s IFA2015. As a part of this, LG Display is planning to expand the current Gen8 34K to 60K by the end of next year. Furthermore, in order to respond to the 65inch market, Gen9.5 line investment is in consideration. In the early 2015, Panasonic commented that they were to withdraw from TV business but changed strategy with new plans of placing OLED TV on the market in Japan and Europe from next year.

As Samsung can no longer be disconnected from the OLED TV business, there are reports of investment for Gen8 OLED for TV line in 2016. Although OLED TV market is estimated to be approximately 350 thousand units this year, in 2016, when Panasonic joins in, it is expected to expand to 1.2 million units. The OLED TV’s market share in ≥55inch TV market is estimated to be only 4% but in premium TV market it is estimated to be significant value of ≥10%.

If Samsung Display invests in Gen8 OLED for TV line in 2016, from H2 2017 supply to Samsung Electronics is possible. As OLED Gen8 line’s minimum investment has to be over 60K to break even, it can be estimated that Samsung Display will invest at least 60K continuously in future.

Under these conditions, LCD industry can only be in crisis. Firstly, it becomes difficult for Sharp to last. Sharp, which is supplying TFT-LCD for Apple’s iPhones and LCD for Samsung Electronics’ TV, will lose key customers. Secondly, BOE, AUO, and JDI, the companies selling LCD panels to these companies, are not ready to produce OLED and therefore damage is inevitable.

BOE is carrying out aggressive investment with plans to lead the display industry in future with operation of Gen10.5 LCD line. Therefore, from 2018, as the main cash cow items disappear, administration pressure could increase.

이충훈, Chief Analyst, UBI Research

BOE가 2018년부터 Gen10.5 LCD 라인을 가동하기 위해 막대한 투자를 집행할 예정인 가운데 Apple과 삼성전자, LG전자, Panasonic 등 주요 세트 메이커들이 스마트폰용 디스플레이와 프리미엄 TV용 디스플레이를 LCD에서 OLED로 전환할 계획을 수립하고 있어 2018년 이후에는 LCD 업계에 불황이 닥칠 가능성이 높아지고 있다.

현재 LCD 업계에서 수익을 창출할 수 있는 부분은 스마트폰용 LTPS-LCD이다. 올해 스마트폰 예상 시장은 약 15억개이며 이중 삼성전자와 Apple이 각각 20%와 15%의 시장을 점유하고 있다. OLED가 사용되는 부분은 2억개 미만이다.

하지만 2018년 이후에는 양상이 많이 달라지게 된다. 우선 LCD 패널만 사용하던 Apple이 빠르면 2017년, 늦어도 2018년부터는 디스플레이 물량의 40% 정도를 OLED로 전환할 것으로 예상된다. Apple은 JDI와 LG디스플레이, 삼성디스플레이의 flexible OLED 패널을 테스트 중에 있으며, 이들 3개사에게 2017년부터 iPhone에 flexible OLED를 채택할 수 있도록 투자를 권유하고 있다. 총 Capa.는 Gen6 기준 60K이다. 삼성디스플레이와 LG디스플레이의 Gen6 라인 신규 투자가 모두 2016년부터 진행될 예정이기 때문에 이론적으로는 2017년부터 물량 공급이 가능하다.

출처) UBI Research database

Gen6 라인에서 5인치 flexible OLED를 생산할 경우 60K Capa.에서 수율을 50%로 가정하면 연 65백만개가 생산 가능하며 80%로 가정하면 약 1억개가 나올 수 있다. Apple의 2017년 iPhone 예상 출하량을 2.7억대로 추산하면 50~60% 수율 범위내에서는 약 25%의 디스플레이가 LCD에서 OLED로 바뀌게 되며, 수율이 80%에 도달하면 40% 정도의 교체가 발생한다. Apple에 스마트폰용 LCD를 공급하고 있는 LG디스플레이와 JDI, Sharp는 매출과 영업 이익에 큰 악영향을 받게 된다. Apple의 디스플레이 교체만으로도 이들 3개사의 사업은 적자 구조로 돌아 설 수도 있다.

더욱이 Apple은 저가폰은 생산하지 않고 있어 추후 iPhone의 모든 디스플레이가 OLED로 바뀔 수도 있음을 가정하면 Apple에 의해 모바일 기기용 LCD 업계는 3년후부터 사업이 휘청거릴 수 있다.

삼성전자 역시 갤럭시에 사용하는 LCD를 점차 OLED로 전환하고 있는 추세이다. 2015년은 예상 출하량 3억대 중 50%인 1.5억개에 OLED를 탑재하고 있으나 추후 flexible OLED와 rigid OLED 탑재 물량을 늘려 나갈 것으로 예상된다. 특히 Apple이 2017년부터 flexible OLED 탑재를 추진하고 있어 OLED를 주력으로 삼고 있는 삼성전자는 Apple 보다 flexible OLED 사용을 늘릴 것으로 전망되며 2019년부터는 갤럭시의 모든 디스플레이가 OLED로 전환될 것으로 예상되고 있다.

이러한 가정하에서는 2020년 예상 스마트폰 시장 약 20억개에서 삼성전자와 Apple의 예상 시장 7억개가 OLED를 사용할 수 있다고 볼 수 있다.

삼성디스플레이는 자사가 생산하고 있는 OLED를 사용할 세트 업체 진영을 강화하고 있다. 삼성전자 이외에 Motorola와 Huawei등 다양한 업체들에게 OLED 패널을 공급하고 있으며, 새로운 강자로 급부상하고 있는 Xiaomi에도 2016년부터 OLED 패널을 공급할 예정이다. 2017년부터 스마트폰용 디스플레이가 LCD에서 OLED로 급 전환되면 현재 TFT-LCD 라인을 증설하고 있는 중국 디스플레이 업체들은 막대한 악영향이 시작될 것으로 예상된다.

또한 프리미엄 TV 시장에서는 LG전자가 올해 IFA2015에서 향후 OLED TV 사업에 집중할 것을 언급하였고, 이 일환으로 LG디스플레이는 현재 보유하고 있는 Gen8 34K를 내년까지는 60K로 확대할 계획이다. 더불어서 65인치 시장에 대응하기 위해 Gen9.5 라인 투자도 검토 중에 있다. Panasonic은 올해 초 TV 사업에서 철수 할 것으로 언급하였지만 계획을 수정하여 내년부터는 OLED TV를 일본과 유럽에 판매할 계획이다.

삼성 진영에서도 더 이상 OLED TV 사업에 손을 놓고 있을 수 없기 때문에 2016년에 TV용 Gen8 OLED 라인 투자에 대한 이야기가 가시화되고 있다. OLED TV 시장은 올해 약 35만대 수준에 불과할 것으로 전망되지만 Panasonic이 가세하는 2016년은 120만대까지 확대될 것으로 추정된다. 55인치 이상 TV 시장에서 OLED TV 점유율은 4%에 불과할 것으로 예상되지만 프리미엄 TV 시장에서는 10% 이상의 의미 있는 수치가 될 전망이다.

삼성디스플레이가 2016년 TV용 Gen8 OLED 라인을 투자하게 되면 2017년 후반부터는 삼성전자에 물량 공급이 가능해진다. OLED용 Gen8 라인은 최소 투자가 60K를 넘어야 손익분기점에 도달 할 수 있기 때문에 추후 삼성디스플레이는 최소 60K는 연속 투자 할 것이라고 가늠할 수 있다.

이러한 상황에서는 LCD 업계는 비상이 걸릴 수 밖에 없다. 첫번째로는 Sharp가 더 이상 버티기 어려워진다. Apple에 iPhone용 TFT-LCD를 삼성전자에 TV용 LCD를 공급하고 있는 Sharp는 주요 고객을 잃게 되기 때문이다. 두번째로 이들 업체들에게 LCD 패널을 판매하고 있는 BOE와 AUO, JDI 역시 OLED 생산 준비가 되어 있지 않기 때문에 타격은 불가피하다.

BOE는 Gen10.5 라인 가동으로 향후 디스플레이 업계에서 선두 주자로 도약할 계획을 가지고 공격적인 투자를 진행하고 있어 2018년 이후에는 오히려 주요 cash cow가 사라져 경영 압박이 가중될 수 있다.

By Hyun Jun Jang

During the 2015 OLED Evaluation Seminar (December 4) hosted by UBI Research, Professor Hong Mun-Pyo of Korea University gave a talk titled Flexible AMOLED Gas Barrier Technology Development Status. Through this presentation, he discussed in detail flexible OLED’s outline, technological issues, and encapsulation among other key issues.

Flexible display signifies a display that was produced on top of flexible substrate, and not an existing glass substrate, which can bend, fold, or roll without breaking. Hong emphasized flexible display is the next generation display that can simultaneously satisfy consumers and panel makers, and an area that OLED can be more valuable compared to LCD.

There are 3 essential issues in flexible display, substrate, TFT array, and display processes, as well as ancillary issues such as application and cost. Hong reported key issues regarding substrate and display process.

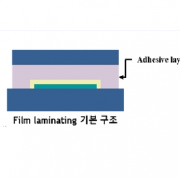

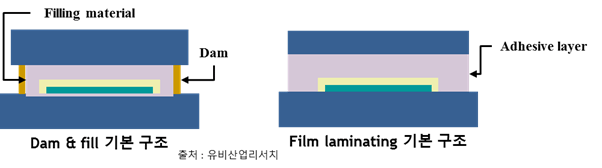

Flexible display uses plastic substrate, instead of glass, that is strong against shock and can bend. Therefore, handling technology that manages plastic substrate is considered a key technology in flexible display production. Hong revealed that for handling technology, a film lamination method and vanish coating method are mainly used. A film lamination method is where plastic substrate is attached to carrier glass using adhesive before being processed and a vanish coating method is where the PI substrate is coated to the carrier glass before processing. He emphasized that no matter which method is used, the debonding technology used to detach the plastic substrate from the glass plays a crucial role in deciding yield.

Hong followed the substrate discussion with encapsulation technology. Encapsulation technology prevents moisture and oxygen that affect OLED panel’s performance from infiltrating in order to increase the display’s lifetime. As it is a core process that decides OLED panel’s yield, OLED panel production companies are focusing on optimum encapsulation technology development.

Key issues of encapsulation technology that is currently being applied to flexible OLED, barrier coating related issues are considered the most important. Barrier coating is the coating applied to the plastic substrate to overcome the limitations that occur as existing glass substrate is replaced by plastic. For flexible encapsulation, as can type or frit seal technologies that were used for glass encapsulation cannot be used, face seal or TFE technologies that can be applied to flexible are used. Also, as the permeability of oxygen and moisture has to be 10-6g/m2day or less, high performing barrier coating technology is needed.

When barrier coating is used to flexible OLED, generally 3 problems occur. Firstly, physically cracks or particles can develop. Regarding this, Hong explained that this issue can be solved if process is properly maintained. The second problem is micro defects that can arise on the surface of plastic film, which can be solved through optimized process, according to Hong. Lastly, nano-sized pin holes can come up. Hong revealed that multi-layers of barrier coating can solve this problem.

Generally, when OLED panel is produced the thickness of encapsulation layer is not a big issue. However, Hong emphasized that the thickness becomes a core issue when producing flexible OLED panel. He reported that hybrid structure of encapsulation where gas barrier cover plate is attached to passivation layer placed via PECVD can be the solution.

Although the most suitable process technology for hybrid encapsulation production is R2R, as appropriate results are not obtained when CVD is applied to R2R, Hong reported that research is being carried out toward the sputtering using direction. He revealed that if reflection plate is added to the sputtering equipment and neutron beam release is induced, defects that occur during the sputtering process can be reduced as the target thin film stabilizes.

4일 유비산업리서치가 개최한 ‘2015 OLED 결산 세미나’에서 고려대학교 홍문표 교수는 ‘Flexible AMOLED용 Gas Barrier 기술개발 현황’이라는 제목의 강연을 통해 플렉시블 OLED의 개요와 기술적인 이슈, 플렉시블 OLED에 적용되는 encapsulation들에 대하여 심층적으로 이해하는 시간을 가졌다.

플렉시블 디스플레이는 기존의 평판 디스플레이의 특성을 그대로 유지하면서 기존 유기기판이 아닌 깨지지 않으며, 휘거나 구부리거나 말 수 있는 유연한 기판 위에 제작된 디스플레이를 의미한다. 홍 교수는 플렉시블 디스플레이는 소비자와 패널 maker를 동시에 만족시킬 수 있는 차세대 디스플레이라고 강조하며 OLED가 LCD보다 더 유용하게 적용할 수 있는 분야라고 밝혔다.

플렉시블 디스플레이에는 크게 기판과 TFT array 공정, 디스플레이 공정 이라는 3가지의 기술적인 이슈가 있으며 application과 cost 등 부수적인 이슈들이 있다. 이 날 홍 교수는 기판, 디스플레이 공정에 대한 핵심 기술에 대한 내용을 발표했다.

플렉시블 디스플레이에는 유리기판이 아닌 휘어질 수 있고 충격에 강한 플라스틱 기판을 사용한다. 그래서 플라스틱 기판을 다루는 handling 기술은 플렉시블 디스플레이 제작에 핵심적인 기술로 꼽힌다. 홍 교수는 “Handling 기술에는 adhesive를 사용해서 플라스틱 기판을 carrier glass에 붙이고 공정을 진행하는 film lamination 방식과 PI기판을 carrier glass에 코팅한 후 공정을 진행하는 vanish coating 방식이 주요하게 쓰인다.”고 밝히며 어떤 방식을 사용하던지 플라스틱 기판을 glass에서 떼내는 debonding 기술이 수율에 결정적인 역할을 한다고 강조했다.

홍 교수는 이어서 디스플레이 공정 중 encapsulation 기술에 관해 논했다. Encapsulation 기술은 디스플레이의 수명을 증가시키기 위해 OLED panel의 성능에 영향을 주는 수분과 산소의 투습을 방지하는 기술을 말하며 OLED panel의 수율을 결정짓는 핵심 공정이기 때문에 각 OLED panel 제조 업체는 최적의 encapsulation 기술을 찾는데 집중하고 있다.

현재 플렉시블 OLED에 적용되는 encapsulation의 핵심 이슈로는 barrier coating에 대한 것이 가장 중요하게 꼽힌다. Barrier coating은 기존 유리기판을 플라스틱으로 대체하면서 발생하는 한계를 극복하기 위해 플라스틱 기판에 부착하는 코팅을 말한다. 플렉시블 encapsulation에는 기존 glass encapsulation에 쓰이는 can type나 frit seal과 같은 기술이 사용될 수 없기 때문에 플렉시블에 적용 가능한 face seal이나 TFE과 같은 기술이 사용된다. 또한 투습되는 산소와 수분의 양은 10-6g/m2day이하가 되어야 하기 때문에 고성능의 barrier coating 기술이 필요하다.

플렉시블 OLED에 barrier coating이 사용될 때 일반적으로 3가지 문제가 발생한다. 먼저 물리적으로 크랙이나 파티클이 발생할 수 있다. 이와 관련하여 홍 교수는 공정 관리를 잘해주면 해결 가능하다고 밝혔다. 두번째로는 플라스틱 필름의 표면에 마이크로 단위 크기의 defect가 발생할 수 있다. 이에 대해서는 공정을 최적화해서 해결 가능하다고 밝혔다. 마지막으로 나노사이즈의 pin hole이 생기는 문제가 발생할 수 있는데 이에 대해서는 barrier coating을 다층박막으로 형성해 해결할 수 있다고 밝혔다.

홍 교수는 보통의 OLED 패널을 제작할 때는 encapsulation 층의 두께가 크게 이슈가 되지 않지만 플렉시블 OLED 패널을 제작할 때는 두께가 핵심적인 이슈가 된다고 강조하며 PECVD로 passivation 층을 올리고 그 위에 gas barrier cover plate를 합착하는 hybrid 구조의 encapsulation이 이에 대한 솔루션이 될 수 있다고 발표했다.

또한 Hybrid encapsulation 제조 시 가장 적합한 공정 기술은 R2R이지만 CVD를 R2R에 적용할 경우 적절한 특성이 나오지 않기 때문에 sputtering을 사용하는 방향으로 연구되고 있다고 하며, sputtering 장비에 반사판을 설치하여 중성화 빔이 방출하도록 유도하면 target 박막을 안정화시켜 기존 sputtering 공정 중에 발생되는 defect를 줄일 수 있다고 밝혔다.

By Choong Hoon Yi

At 2015 OLED Evaluation Seminar (December 4) hosted by UBI Research, Sung-Kee Kang, DS Hi-Metal’s CSO, reported that OLED display market has to expand through OLED TV and new applications in order for OLED emitting materials companies to grow.

Presenting under the title of ‘OLED Organic Material Technology, Industry Trend’, Kang introduced the current OLED emitting material value chain. He explained that within OLED emitting materials market, there are too many players considering the current volume and overall OLED display market expansion is a necessity. However, he added that for OLED display to compete against LCD display, OLED TV market has to expand successfully, and new application that utilizes OLED’s characteristics is needed.

In order to expand the market, development of OLED emitting materials and other materials is urgently in demand that meet the required conditions. Kang emphasized that at present new technology seeds promotion for the next OLED is needed as well as development of OLED emitting materials, and other flexible/transparent related materials with new functions.

Considering LG’s active OLED TV marketing, Apple’s interest in OLED panel application, and possibility for Samsung to apply AMOLED to all models among others, OLED market is anticipated to rapidly grow. Together with this, the industries of OLED emitting material and component/other materials with new functions are also expected to considerably grow.

유비산업리서치가 개최한 ‘2015 OLED 결산 세미나’에서 덕산 네오룩스 CSO 강성기 전무는 OLED용 발광 재료 업체들이 성장하기 위해서는 OLED TV와 새로운 어플리케이션을 통한 OLED 디스플레이 시장 확대가 되어야 한다고 발표했다.

강성기 전무는 ‘OLED용 유기소재 기술, 산업 동향’이라는 주제로 발표하면서 현재 OLED 발광 재료 value chain을 소개했다. 이에 강 전무는 ‘OLED 발광 재료 시장은 현재 규모에 비해 player가 많아서 전반적인 OLED 디스플레이 시장 확대가 필수적’이라고 강조했다. 하지만 OLED 디스플레이가 LCD 디스플레이에 경쟁력을 갖추기 위해서는 OLED TV시장이 성공적으로 확대되어야 하며, OLED의 특징을 활용한 새로운 어플리케이션 시장 창출이 필요하다고 덧붙였다.

OLED 시장을 확대하기 위해서는 OLED TV와 flexible, transparent등에 필요한 요구 조건을 갖추고 있는 OLED용 발광 재료와 부품 소재의 개발이 시급하다. 강성기 전무는 ‘지금은 OLED용 발광 재료, flexible/transparent관련 신 기능 소재 개발과 함께 Next OLED를 위한 신기술 seeds 육성이 필요한 상황’이라고 강조하였다.

LG의 본격적인 OLED TV 마케팅과 Apple의 OLED panel 적용에 대한 관심, Samsung 스마트폰의 전모델 AMOLED 적용 가능성 등 앞으로 OLED 시장이 급격히 성장할 것으로 기대되는 가운데 OLED 발광재료와 신기능 부품/소재 산업 또한 크게 성장할 것으로 기대된다.

10월 27일부터 29일까지 미국 버클리에서 개최되는 OLEDs World Summit의 첫째 날, 삼성디스플레이와 LG디스플레이는 연이어 발표에 나섰다. 삼성디스플레이의 이창훈 상무와 LG디스플레이의 임주수 OLED 기술전략팀장은 각각 ‘The Future of OLEDs’와 A Future Game Changer’라는 주제로 OLED에 대해 발표했다.

삼성디스플레이의 이 상무는 먼저 발표에 나서며 모바일 시장 내에서 삼성디스플레이의 선도적인 역할과 삼성전자의 모바일 디스플레이가 이것을 어떻게 반영하였는지를 강조하였다. 이 상무는 사람의 눈의 구조와 다이아몬드 픽셀 구조 사이의 관계를 통해 일반 RGB픽셀 구조와 다른 삼성디스플레이의 다이아몬드 픽셀 구조를 설명하였다. 사람의 눈은 다른 색상보다 green에 더 민감하다. 다이아몬드 픽셀은 이런 특성을 반영해서 green 서브픽셀을 blue와 red 서브픽셀보다 2배 많도록 배치하여 형성한 픽셀구조다. 다이아몬드 픽셀 구조는 서브픽셀 packing을 최대화하고 PPI를 증가시키는 장점이 있다.

OLED 디스플레이의 이점에 대하여 이 상무는 삼성전자의 최신 스마트폰의 2가지 기능을 예시로 들었다. 먼저 AMOLED 디스플레이는 각 픽셀의 선택적 제어가 가능하다는 점을 말하며 삼성이 색약자를 돕기 위해 제공하는 Vision Aid라는 기술을 예로 들었다. 또한 OLED의 완벽한 블랙을 낼 수 있는 능력은 Super Dimming이라는 기술에 쓰여 어두운 환경에서 화면의 밝기를 2nit까지 줄일 수 있게 한다고 발표하였다.

LG디스플레이의 임 팀장은 미국의 성인들이 하루에 평균적으로 9시간 40분을 디스플레이를 보는데 쓴다고 밝혔다. 고품질 디스플레이의 중요성과 필요성을 강조하며 임 팀장은 삼성의 발표와 마찬가지로 완전한 블랙, 3D효과, 높은 색재현률 등 LCD보다 나은 OLED 디스플레이의 이점들을 발표하였다.

이 부사장과 임 팀장 모두 미래 OLED 디스플레이로 투명이나 거울디스플레이보다 플렉시블(플라스틱)OLED를 좀 더 중점에 두었다. 삼성디스플레이는 플렉시블 디스플레이를 위한 커버윈도우와 flexible backplane, touch sensor, encapsulation등 핵심 요소들에 대해 발표하였다.

LG디스플레이는 플렉시블 디스플레이의 디자인 자유도와 이것이 웨어러블과 모바일, 차량 시장에 미치는 영향에 대해 논했다. 임팀장은 또한 얼마나 OLED가 유연해질 수 있느냐가 가상현실(VR) 디스플레이 시장에 적용되는데 핵심적인 요소가 될 것이라고 전망했다. 두 명의 발표자들은 OLED 기술과 새로운 어플리케이션이 새로운 디스플레이 시장과 혁신에 필요하게 될 것이라고 단언하여 발표를 마쳤다.

삼성디스플레이는 TV에는 LCD 패널을 계속 넣는 대신 투명·미러·플렉서블과 같은 차세대 제품에는 OLED 패널을 적용하는 투 트랙 전략을 고수하고 있으며, LG디스플레이는 중소형 OLED 시장과 OLED TV 패널 시장을 동시에 노리고 있다. 이번 발표를 통해 두 업체 모두 미래 성장동력인 OLED의 기술수준 향상에 집중할 것으로 보이며 특히 단기적으로는 플렉시블 OLED 개발에 중점을 둘 것으로 전망된다.

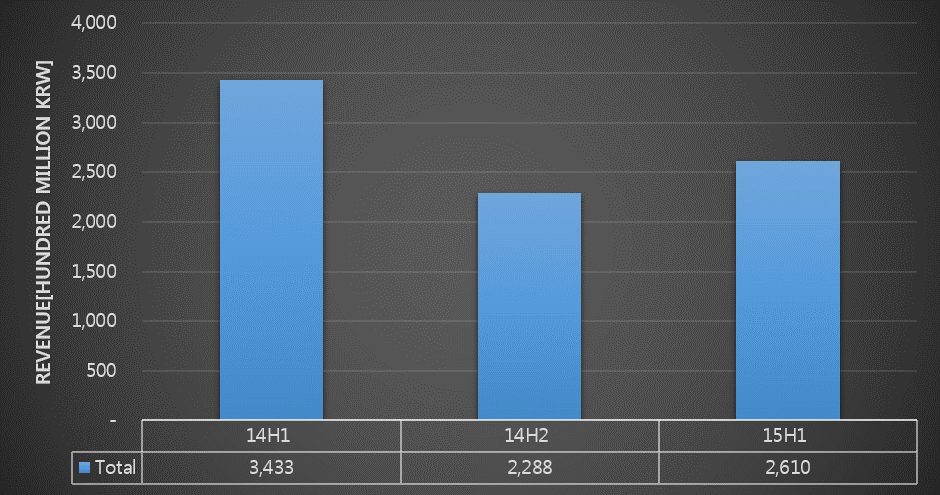

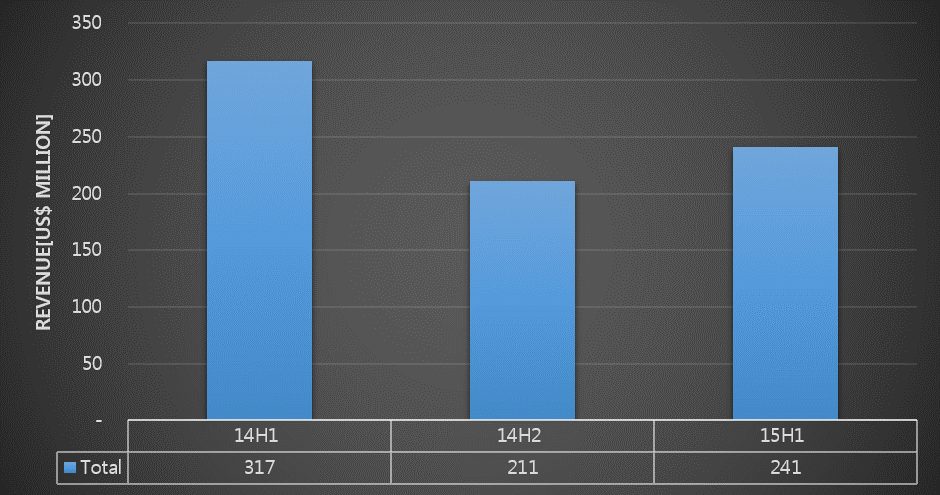

According to UBI Research, the 2015 H1 OLED material market recorded approximately US$ 564 million; this is a 14% increase compared to 2014 H2, but a 24% decrease against 2014 H1.

Despite reports that Samsung Electronics and LG Electronics are selling much larger volumes of flexible OLED applied Galaxy S6 Edge and OLED TV respectively compared to last year, the OLED material market is gradually stagnating.

The main reason for this OLED material market’s downward turn is Samsung Display’s operation level which remained stationary at 50% in H1. This led to stationary material usage compared to the year before. LG Display is producing flexible OLED and large size OLED panel for TV. However, approximately only 100,000 units of OLED panels were sold in H1 and material usage was also lowl. The current capa. is 34K but as the OLED material cost spent in H1 is approximately US$ 36 million, the operation rate is analyzed to be only 30% of the total capa.

The OLED material market is decreasing because the supply price is rapidly falling without increase in production volume. OLED material companies are frustrated at the 10-15% price decrease per quarter. At present, as the only clients are Samsung Display and LG Display, material companies are compelled to reduce the price as the failure to do so could lead toward the termination of business. OLED material companies spend several thousands of millions of dollars annually on development to meet constant improvement demanded by clients. There is much difficulty for OLED material companies as display companies continue with one-sided demands without compensation regarding development cost.

For OLED industry to maintain its continued growth, it requires more than success of panel companies. Material companies that play a pivotal part within the industry have to continue development and production of quality materials in order to create a healthy growth cycle. However, display companies are destroying the ecosystem.

What OLED material companies currently crave is for Chinese display companies to mass produce OLED panels as soon as possible.

* 1 USD = 1,100 KRW

OLED Material Market Revenue 2014 H1 – 2015 H1

Samsung Electronics, the current global leader of smartphone market share, challenged Apple to dominate smartwatch market with Galaxy Gear 2 armed with latest functions.

The exterior of Gear 2 changed to round type. Previous Gear copied rectangular fashion watch, but Gear 2 returned to the classic design.

Galaxy Gear 2, IFA 2015

Gear 2 has the most basic circular shape, but the rotating bezel within the simple design boasts the perfect blend of digital and analog. The rotating bezel design used in stop watch in quality sports watch was applied to add a touch of analog. At the same time, the smartwatch has the digital side from the jog dial used in quality vehicles, merging the analog with digital.

Smartwatches until now had to be touched to change screen. However, Gear 2’s rotating bezel allows the screens to be changed easily through dial rotation.

Galaxy Gear 2, IFA 2015

Gear 2 applied flexible OLED produced by Samsung Display same as Gear with its 1.2inch size and 360×360 resolution. Compared to competitors’ 1.3inch, it might feel smaller but has the highest resolution; Samsung Electronics used a smaller display with better expressiveness. Particularly, absolute black, one of the advantages of OLED, is actualized with this product. The quality of black in previous Gear fell short and the screen wallpaper showed hints of blue. The new display shows that it is of OLED leader, Samsung family, with its brilliant colors using latest OLED materials.

Gear 2 also uses Tizen OS and firmly differentiated itself from other products. In fact, other products employed Google OS and had a problem of basically being the same under the different exterior leading to no particular differentiation factors for the consumers.

However, deserving the title of the leader of the smart device, Samsung Electronics utilized independently developed Tizen and boasted totally different interior.

Galaxy Gear 2, IFA 2015

Samsung Electronics is investing much effort in Gear 2 promotion; with the exclusive booth, visitors can examine diverse forms of Gear 2.

Galaxy Gear2 Booth, IFA 2015

유비산업리서치에 따르면 올해 상반기 OLED 발광재료 시장 규모는 약 2600억원으로 전 반기대비 14% 상승했지만 전년 동기 대비 24% 감소했다.

올해에는 삼성전자가 flexible OLED를 탑재한 Galaxy S6 Edge를, LG전자에서는 OLED TV를 작년 보다 수십배 이상 판매하고 있다고 하지만 OLED 재료 시장은 점차 얼어 붙고 있는 실정이다.

OLED 재료 시장이 마이너스 성장으로 돌아 선 것은 무엇보다도 OLED 대표 기업인 삼성디스플레이의 상반기 가동율이 50% 수준에 머물러 재료 사용량이 전년 동 반기 대비 늘지 않았기 때문이다. LG디스플레이는 flexible OLED와 TV용 대형 OLED 패널을 생산하고 있지만 상반기 OLED 패널 판매는 약 10만대에 불과하여 재료 소모량 역시 얼마 되지 않는다. 전체 capa는 34K이지만 상반기 구매한 OLED 재료비는 약 400억원 정도에 불과하여 가동율이 전체 capa의 30%에 불과한 것으로 추정된다.

OLED 재료 시장이 줄어든 이유는 생산량 증가 없이 공급 가격만 심하게 깍이고 있기 때문이다. OLED 재료 업체들은 분기당 10~15% 가격이 인하되고 있다고 불만을 토로하고 있다. 현재로서는 수요 기업이 삼성디스플레이와 LG디스플레이 밖에 없는 실정이기 때문에 가격 인하에 불응하면 거래 자체가 단절될 수 있어 울며 겨자 먹기로 가격을 낮추고 있다. OLED 재료 업체들은 수요 기업들이 성능이 향상된 재료 개발을 끊임없이 요구하고 있어 연간 개발비가 수십억원 이상 소요되고 있지만 디스플레이 업체에서는 개발비에 대한 가격 보전 없이 일방적인 요구만 지속되고 있어 사업에 어려움이 심각하다.

OLED 산업이 지속 성장하기 위해서는 패널 업체만 살아서는 유지될 수 없다. 산업을 지탱하고 있는 한 축인 재료 업체들이 좋은 재료를 끊임없이 개발하고 생산해야지만 선순환 구조로 산업이 성장할 수 있다. 하지만 디스플레이 업체들은 생태계를 완전히 망가뜨리고 있다.

OLED 재료 업체들이 현재 가장 바라고 있는 것은 중국 디스플레이 업체들이 하루 속히 OLED를 대량으로 생산하는 것이다.

반기별 OLED 발광재료 시장 실적 2014H1~2015H1

스마트폰 시장 세계 점유율 1위를 차지하고 있는 삼성전자가 스마트 워치 시장을 장악하기 위해 최신 기능으로 무장한 Galaxy Gear2로서 Apple에 도전장을 던졌다.

Gear2의 외관은 라운드 타입으로 바뀌었다. 전작인 Gear에서는 사각의 패션 시계를 모방했으나 이번에는 전통적인 시계 모양으로 돌아왔다.

Galaxy Gear2, IFA 2015

Gear2가 가장 기본적인 둥근 형태로 제작되었지만 심플한 디자인 속에 숨어 있는 rotating bezel은 디지털과 아날로그 느낌을 기막히게 조화 시켰다. 고급 스포츠 시계에서 사용되는 스톱워치용 회전 베젤 디자인을 사용하여 아날로그 감각을 부여했으며, 동시에 고급 자동차에 장착되는 조그 다이얼의 디지털 감각을 부가해서 아날로그와 디지털 감각을 일체화 시킨 스마트 워치이다.

현재까지 출시되고 있는 스마트워치는 화면을 바꾸기 위해서는 화면을 터치하며 넘겨야 하는 불편함이 있었으나 Gear2의 rotating bezel은 다이얼 회전에 의해 쉽게 화면을 변경할 수 있도록 만들어졌다.

Galaxy Gear2, IFA 2015

Gear2는 Gear와 마찬가지로 삼성디스플레이에서 생산하는 flexible OLED를 사용했다. 디스플레이는 사이즈는 1.2인치이며 해상도는 360×360이다. 경쟁업체들은 1.3인치를 사용하고 있어 조금 작은 느낌이 있지만 해상도는 오히려 최고 수준이다. 크기는 작아도 표현력이 더 훌륭한 강력한 디스플레이를 사용했다. 특히 이번 제품은 OLED의 최고 특성인 black가 완벽하게 표현되고 있다. 전작인 Gear에서는 black 특성이 나빠 바탕 화면이 청색 빛깔을 띠었으나 이번에는 OLED를 사용한 것임을 알 수 있게 하였다. 최근에 개발된 OLED 재료들을 사용하여 색상이 매우 화려하여 OLED 종주 기업인 삼성가(家)의 혙통을 물려 받은 최고의 제품임을 알 수 있다,

삼성전자가 다시 도전장을 내민 Gear2는 타이젠 기반의 OS를 사용하고 있어 타 제품과의 차별화도 분명히 했다. 실제로 타 제품들은 Google의 OS를 사용하고 있어 외양은 다르나 속은 모두 동일하여 고객 입장에서는 차별성이 보이지 않는 문제점이 있었다.

하지만 삼성전자는 스마트 기기 최고 기업답게 독자적으로 개발한 타이젠을 사용하여 내부도 완벽히 새로 디자인하여 차별화하였다.

Galaxy Gear2 Booth, IFA 2015

IFA2015에서 삼성전자는 Gear2 홍보에도 많은 심혈을 기울이고 있다. 전용 부스를 마련하여 다양한 Gear2를 참관자들이 관람할 수 있도록 배려하고 있다.

Galaxy Gear2 Booth, IFA 2015

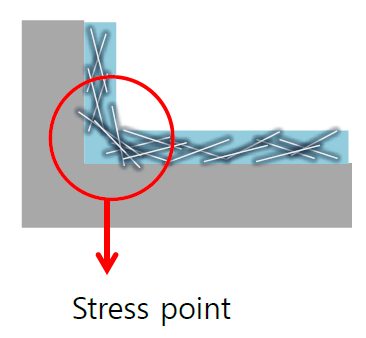

At IPEC 2015 (International Printed Electronic Conference), held on September 1, Professor Sang-Ho Kim of Kongju National University announced that silver nanowire technology is in initial stages of commercialization and will become display market’s key material.

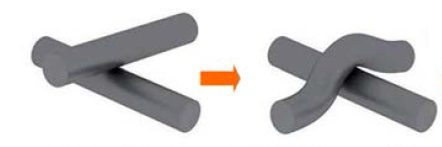

Kim reported that when the bending radius of flexible display is reduced, 2 key issues occur with silver nanowire used as TSP (touch screen panel) material. First, the wiring that are crossed when bending is loosened as can be seen in figure 1. Due to this effect the bending stability decreases.

Fig. 1, Source: Professor Sang-Ho Kim, IPEC 2015

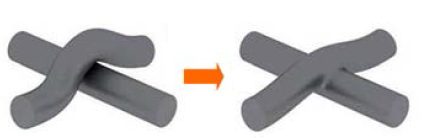

Kim explained that this effect can be solved by welding the two wires as shown in figure 2 using thermal annealing technology, laser process, and IPL photo-sintering technology.

Fig 2, Source: Professor Sang-Ho Kim, IPEC 2015

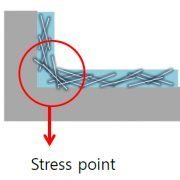

Another issue is a decrease in contact stability between nanowires at stress points when bending radius is reduced as shown in figure 3.

Fig 3, Source: Professor Sang-Ho Kim, IPEC 2015

During the presentation, Kim explained that this can be solved through undercoating process. This process involves mixing 2 polymers with different Tg (glass-transition temperature) and layering it as in figure 4, and placing TSP on top.

Fig 4, Source: Professor Sang-Ho Kim, IPEC 2015

Silver nanowire has benefit of being more flexible and less resistant compared to transparent electrode material, ITO. As such, it was spotlighted as TSP material most suitable for flexible OLED. Nonetheless, silver nanowire has been considered to fall behind ITO in panel mass production unit cost in display market.

However, haze effect which happens when sunlight is reflected off the silver nanowire TSP has been solved recently, and new touch technology that requires improved TSP functions, such as post-touch technology, has been developed. Accordingly, products that use silver nanowire are increasing despite the unit cost difference.

Kim reported that as TSP sheet resistance can be reduced through undercoating and welding technology and greatly increase bending stability, it is estimated that silver nanowire’s marketability will grow for flexible display.

공주대학교 김상호 교수는 9월 1일 서울 코엑스에서 개최된 IPEC(International Printed Electronic Conference) 2015에서 “Silver nanowire 기술은 현재 상업화 초기 과정에 있으며, 앞으로 디스플레이 시장의 핵심 소재가 될 것이다.”라고 말했다.

김교수는 flexible display의 bending radius가 감소할 때 TSP(Touch Screen Panel)소재로 쓰이는 silver nanowire에 2가지 주요 이슈가 생긴다고 발표하였다. 먼저 bending시 겹쳐져 있는 배선이 그림 1과 같이 느슨해지는 현상이 발생하며, 이 현상으로 인해 bending stability가 낮아진다고 밝혔다.

그림 1, Source : 김상호 교수, IPEC 2015

김교수는 이 현상을 그림 2와 같이 두 배선을 thermal annealing 기술과 레이저 공정, IPL 광소결 기술을 활용한 welding (용접)하는 공법으로 해결이 가능하다고 발표하였다.

그림 2, Source : 김상호 교수, IPEC 2015

다른 이슈로는 bending radius가 감소할 때 그림3과 같이 stress point에서 nanowire 사이의 contact stability가 낮아지는 현상이 나타난다고 밝혔다.

그림 3, Source : 김상호 교수, IPEC 2015

김교수는 이 문제는 Tg값이 서로 다른 2개의 polymer를 섞어 그림 4와 같이 층을 깔고 경화시킨 후 그 위에 TSP를 올라는 undercoating 공정을 통해 해결할 수 있다고 발표하였다.

그림 4, Source : 김상호 교수, IPEC 2015

Silver nanowire는 기존에 쓰이던 투명전극 소재인 ITO보다 flexibility가 높고 저항이 적은 장점이 있어 flexible OLED에 최적화된 TSP(Touch Screen Panel)소재로 각광받았지만 디스플레이 시장에서 패널 양산 시 단가경쟁에서 ITO에 밀린다는 평가를 받아왔다.

하지만 최근 silver nanowire TSP에 햇빛이 반사되어 전체 스크린이 뿌옇게 보이는 haze 현상이 해결되고 포스터치 기술 등 향상된 TSP 성능이 요구되는 새로운 터치 기술이 등장하면서 단가의 차이에도 불구하고 silver nanowire를 차용하는 제품이 점점 증가하는 추세이다.

김상호 교수는 “Undercoating 기술과 welding 기술을 함께 사용하여 TSP의 면저항을 낮추고 bending stability를 크게 높일 수 있기 때문에 차후 flexible 디스플레이에서 silver nanowire의 시장성이 커질 것으로 전망된다.” 라고 발표하였다.

During the keynote session of IMID 2015 (August 18 – 21), LG Display’s Sang Deog Yeo, the head of OLED division revealed LG Display’s intention to change the world with OLED together with everyone and strength in OLED industry expansion. Yeo explained that the most important factor in the success of large area OLED is strong conviction in OLED’s success and courage; he also announced further investment for OLED as future growth stimulus.

Yeo reported that TV’s first revolution was a change from black and white TV to color. The second revolution was the appearance of flat panel display and that the third revolution will be OLED. He explained that the key factors in TV panels are design and picture quality. He evaluated that these factors are advancing separately in other display while OLED is improving these issues together.

Explaining in more detail, Yeo reported that OLED has high design freedom as OLED structure is simple, a self-emitting light without BLU. Additionally, each pixel of OLED can operate independently and actualize true black, leading to differentiated picture quality.

In the beginning, LG Display struggled in applying WRGB technology and oxide TFT to OLED TV, which resulted in almost 0% of yield. Even within the company, there were opinions that oxide TFT application to Gen8 panel or larger will be almost impossible. However, the effort including introduction of external compensation circuit and coplanar structure, and compensation algorithm application to brightness and color brought LG Display’s current success of OLED TV mass production.

Yeo announced that much like how LG Display solved OLED TV’s technological problems of the past, they will improve the oxide TFT mobility to 50. He also revealed that LG Display is searching for a method of applying top-emission technology to mass production in order to improve transparent and flexible OLED technology, and researching light shutter technology and improved plastic substrate application technology.

LG Display recently announced their decision to invest approximately US$ 9,300 million centering around OLED. During the keynote session, Yeo reported that LG Display will increase the large area OLED panel’s production rate through investment, specifically from current 600 thousand units to 2 million units in 2017. He also announced that they will expand Gumi Gen6 line which will be used to increase production rate of small to medium-sized OLED panels and plastic OLED panels.

Although there has been speculation regarding this investment, through this keynote speech, it can be forecast the investment will be used in specific roadmap of large and small to medium-sized OLED. For the progress of OLED industry, which is growth stimulus of the future, Yeo emphasized the need for closer cooperation between materials, components, manufacturing equipment, and set companies, and laboratories and universities.

LG Display’s Sang Deog Yeo, IMID 2015

대구 엑스코에서 8월 18일 개막한 IMID 2015의 keynote session에서 LG 디스플레이의 여상덕 사장은 “여러분과 함께 OLED로 세상을 바꾸고자 한다.”고 밝히며 OLED 산업 확장에 대한 의지를 내비쳤다. 여사장은 대형 OLED 성공의 가장 중요한 요소는 OLED 성공에 대한 강한 확신과 용기라며 미래 성장동력인 OLED에 대한 투자를 더욱 강화할 예정이라고 밝혔다.

여사장은 TV 시장의 첫번째 혁명은 흑백에서 컬러로 바뀐 것이며 두 번째 혁명은 flat panel display의 등장이며 3번째 혁명은 OLED가 될 것이라고 발표하였다. TV용 패널의 중요 요건으로 디자인과 화질을 꼽으며 다른 디스플레이는 이런 요건이 각각 발전하고 있지만 OLED는 중요 요건이 함께 발전하고 있다고 평가하였다.

구체적으로 OLED는 구조가 단순하며 특히 BLU 없이 자체 발광하기 때문에 디자인 자유도가 높다고 하였다. 또한 OLED는 픽셀 개별 구동이 가능하며 완전한 black을 구현할 수 있기 때문에 화질적인 측면에서 다른 디스플레이와 수준이 다르다고 말했다.

LG디스플레이는 WRGB기술과 oxide TFT를 OLED TV에 적용하는 과정에서 수율이 0%에 가까울 정도로 초반에 고전하였다. 특히 회사 내부에서도 8세대 이상 패널에 oxide TFT를 적용하기는 불가능에 가깝다고 평가될 정도였다. 하지만 외부 보상회로의 도입과 coplanar구조 도입, 밝기와 color에서 보상 알고리즘 적용 등의 노력으로 현재의 OLED TV 양산에 성공하게 되었다.

여사장은 “LG디스플레이는 과거 OLED TV의 기술적 문제를 해결한 것처럼 oxide TFT의 mobility를 50까지 올릴 것이며 transparent와 flexible OLED 기술 향상을 위해 양산에 top-emission 기술을 적용하는 방안을 찾고 있으며 light shutter 기술과 향상된 plastic기판 적용기술을 연구하고 있다.”고 발표하였다.

최근 LG디스플레이는 OLED를 중심으로 10조원을 투자할 것이라고 밝혔다. 이 날 발표에서 여사장은 투자를 통해 대형 OLED 패널의 생산량을 늘릴 것이며 구체적으로 현재 60만장에서 2017년까지 200만장으로 생산량을 늘릴 예정이라고 밝혔다. 또한 구미 6세대 라인을 확장할 것이며 이를 통해 중소형 OLED패널과 plastic OLED 패널 생산량을 늘릴 계획에 있다고 발표하였다.

10조원의 LG디스플레이 투자에 대해 지금까지 대략적인 추측만 있었지만 이 날 발표를 통해 이번 투자가 대형과 중소형 OLED 각각의 구체적인 로드맵에 투입될 것으로 전망된다. 여사장은 소재, 부품, 장비, set 업체와 연구소, 학교가 미래성장동력인 OLED 산업 발전을 위해 더 긴밀한 협력이 필요하다고 강조하였다.

LG Display 여상덕 사장, IMID 2015

With the great increase of interest in flexible OLED from China and Taiwan’s small and medium-sized panel companies, diverse issues related to this are emerging.

Recent smartphone trend is moving from high resolution and specs toward diverse designs such as curved or bendable/foldable and flexible display that can differentiate applications. AMOLED flexible display is currently being applied to smartphone and smartwatch. However, only 2 companies, Samsung Display and LG Display, are supplying these high spec flexible AMOLED panel.

Small and medium-sized panel companies do not have the technology to mass produce high performance flexible AMOLED panel and cannot invest in mass production. For these reasons, Chinese and Taiwanese small and medium-sized companies are aiming for finding new applications where flexible PMOLED or low resolution flexible AMOLED can be applied and make mass production investment. Accordingly, set companies’ interest in flexible OLED applied application is also increasing.

Additionally, companies are in agreement that yield of flexible PMOLED that is applied to some smartbands does not meet demand. Taiwan’s wisechip and RiTdisplay, key PMOLED companies, are concentrating on developing flexible PMOLED and flexible OLED lighting. Taiwan’s AUO and Innolux, and China’s Visionox and EDO are also among those that are developing wearable flexible AMOLED.

Diverse application development where lower resolution flexible AMOLED, flexible PMOLED, or flexible OLED lighting, instead of expensive high-end smartphone and smartwatch, can be applied is essential. The outcome of this is forecast to greatly affect the growth of small and medium-sized OLED panel companies.

중국과 대만의 중소형 panel 업체들의 flexible OLED에 대한 관심이 증폭됨에 따라 이와 관련된 다양한 이슈들이 나오고 있다.

최근 스마트폰의 트렌드는 고성능 고해상도의 높은 스펙의 high-end panel에서 curved나 bendable/foldable 등의 디자인과 application을 차별화 시킬 수 있는 flexible display 적용에 업체들의 관심이 쏠리고 있는 추세이다.

현재 flexible display로서 AMOLED가 smart phone과 smart watch에 적용이 되어 출시되고 있지만 이러한 고스펙의 flexible AMOLED panel을 공급하고 있는 업체는 삼성디스플레이와 LG디스플레이 두 업체에 불과하다.

중소형 패널업체 입장에서는 이러한 고성능의 flexible AMOLED panel 양산할 기술이 없을뿐더러 양산에 투자할 여력이 없기에 중국과 대만의 중소형 업체들은 flexible PMOLED나 저해상도의 flexible AMOLED이 적용될 수 있는 신규 application을 발굴하고 양산 투자를 하는 것을 목표로 하고 있다. 이에 따라 세트업체들의 flexible OLED를 적용한 어플리케이션에 관한 관심 또한 높아지고 있는 것으로 보여진다.

또한, 현재 smart band 일부에 적용되는 flexible PMOLED는 생산이 수요에 못 미치고 있다는 것이 업체들의 공통된 의견이다.

대표적인 PMOLED 업체인 대만의 wisechip과 RiTdisplay는 flexible PMOLED와 flexible OLED lighting에 대한 개발에 집중하고 있으며, AUO와 Innolux, 중국의 Visionox와 EDO등도 wearable용 flexible AMOLED에 대한 개발을 진행 중이다.

고가의 high-end smart phone과 smart watch가 아닌 저해상도의 flexible AMOLED나 flexible PMOLED, flexible OLED lighting등이 적용될 수 있는 다양한 application 발굴이 앞으로 중소형 OLED panel업체들의 성장에 큰 영향을 미칠 전망이다.

Dr Choong Hoon Yi, UBI Research Chief Analyst, ubiyi@ubiresearch.co.kr

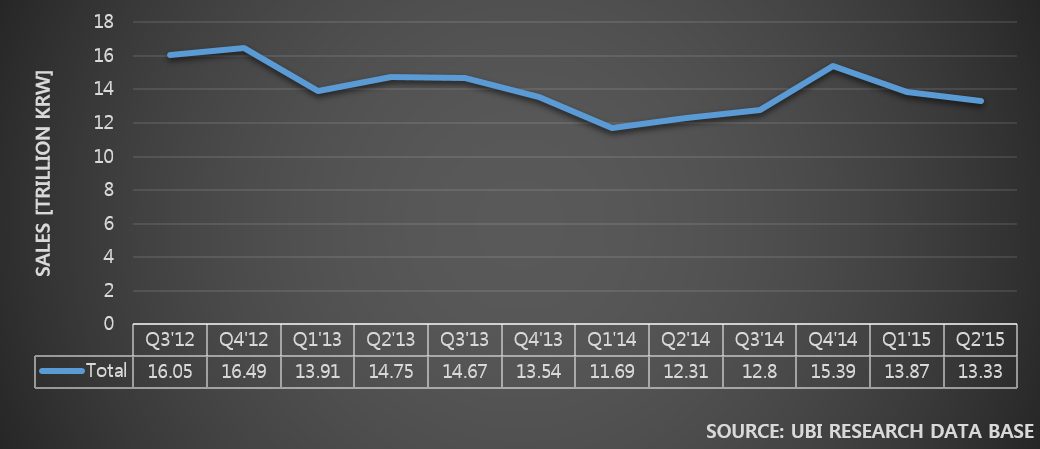

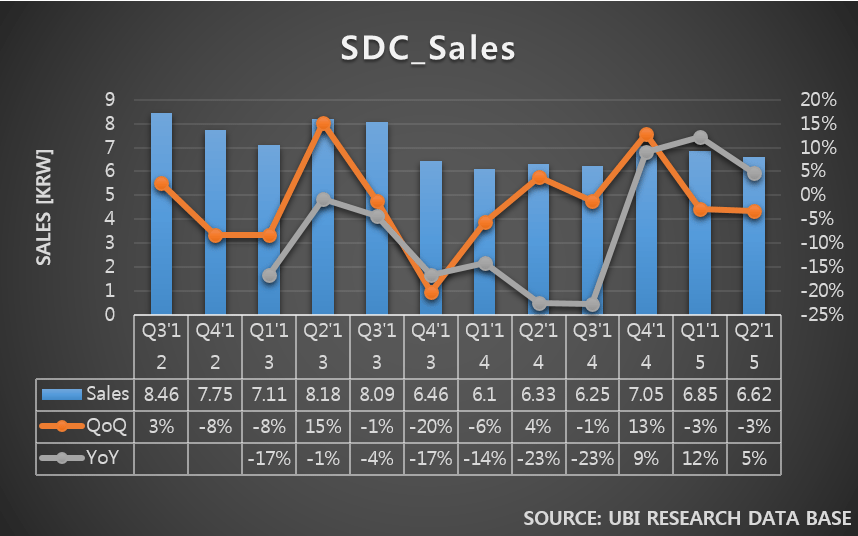

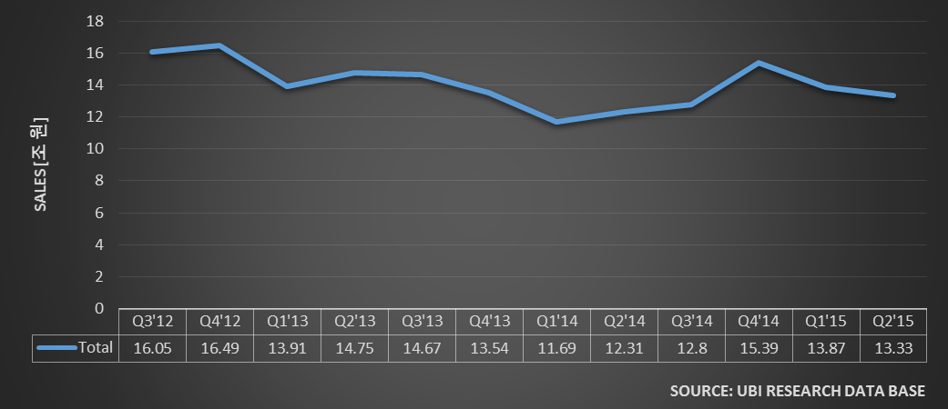

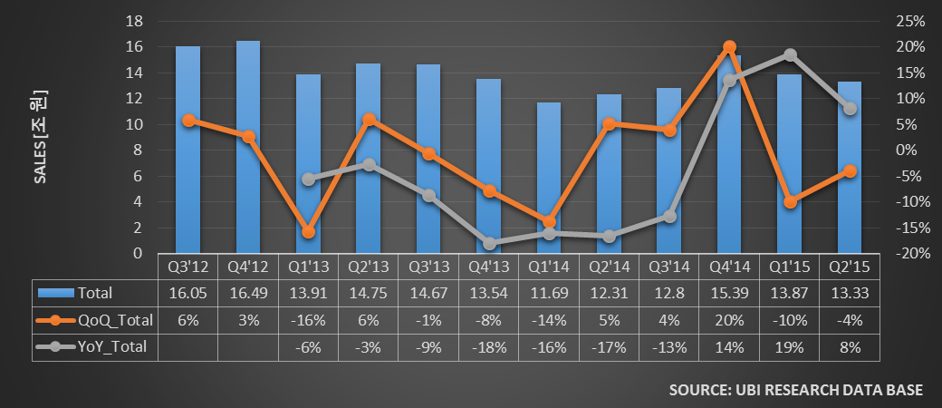

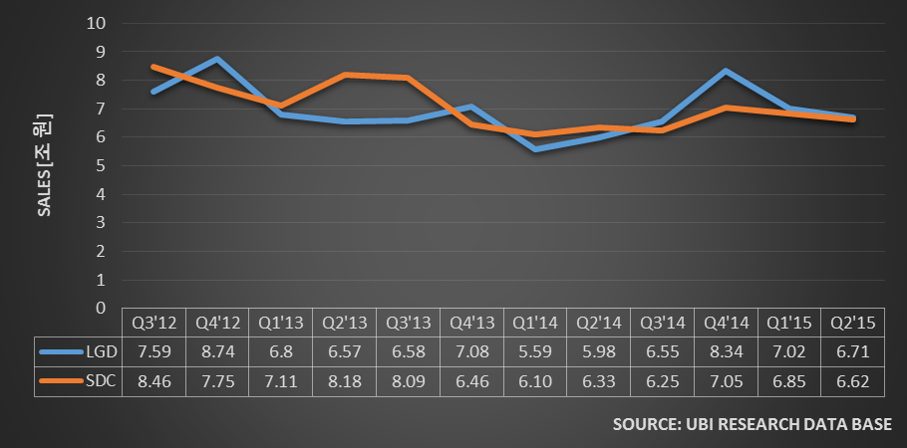

The analysis of 2015 2Q results of Samsung Display and LG Display shows clear indication that Korean display industry is on descent.

[2015 Q2 Korean Display Total Sales Analysis]

According to the results announcement of the 2 companies, the total of 2015 Q2 sales is approximately US$ 11,000,000,000. Compared to the total sales in 2013 Q2 which was US$ 13,000,000,000, Korean display industry trend is exhibiting clear downward tendency.

2015 Q2 Korean display sales records -4% QoQ, and 8% YoY.

The main reason for the decrease in sales is Samsung Display’s deterioration of earnings results. While LG Display’s sales of the past 3 years remain fairly consistent but Samsung Display’s sales is gradually decreasing.

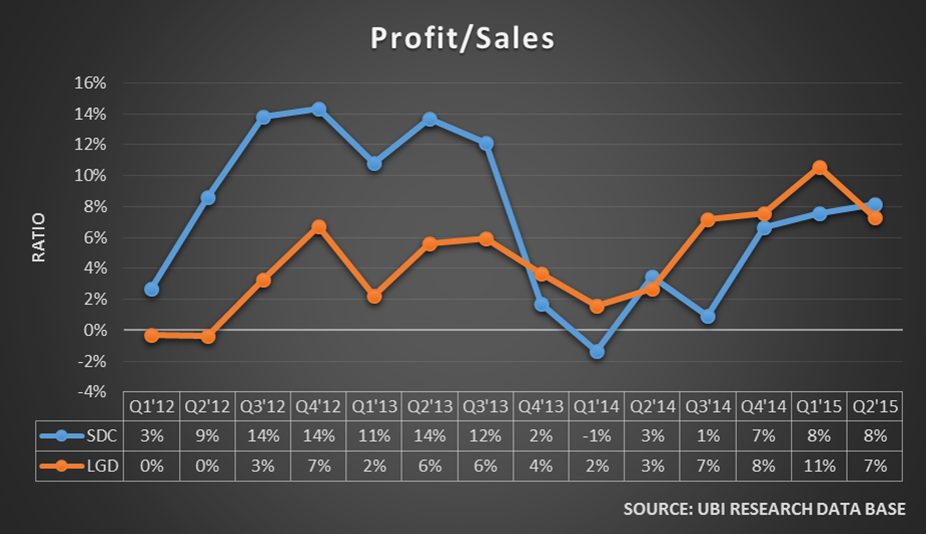

[2015 Q2 Korean Display Total Business Profit Analysis]

Connecting the high points of the total of 2 companies’ business profit reveal that the business value is worsening as the trend moves downward. This also is much contributed to Samsung Display’s business profit decrease.

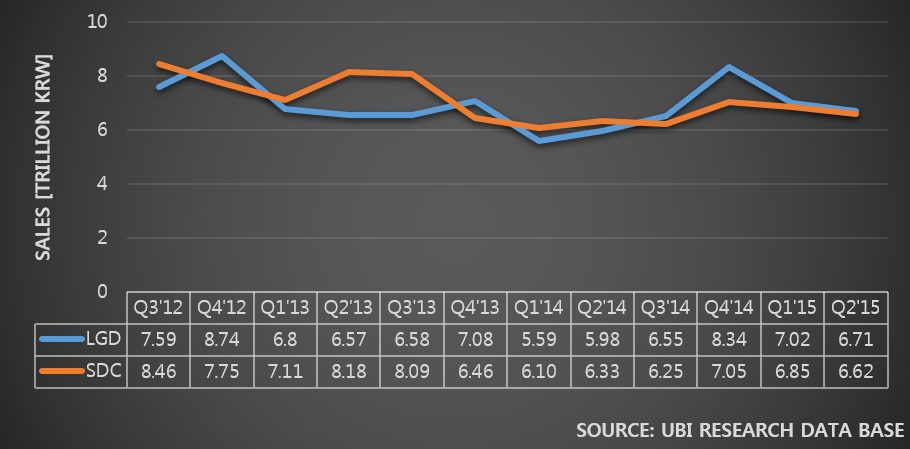

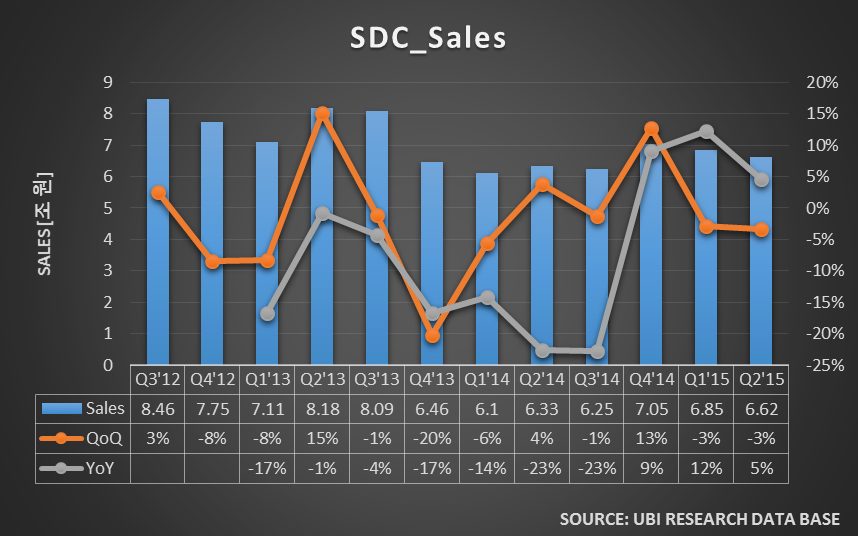

[Samsung Display and LG Display Sales Analysis]

According to the earnings announcement of both companies, Samsung Display and LG Display recorded sales of approximately US$ 5,500,000,000 and US$ 5,600,000,000 respectively. LG Display is maintaining higher sales results compared to Samsung Display for the past 5 quarters. Each company’s QoQ showed to be -4% (LGD) and -3% (SDC) and YoY to be 12% (LGD) and 5% (SDC). The simultaneous decrease of QoQ sales of both companies demonstrates that the Q3 sales could also fall.

[Samsung Display and LG Display’s Competitiveness Analysis]

Looking at the profit/sales graph of Samsung Display and LG Display, it is apparent that Samsung Display showed superior competitiveness until 2013 Q3, but since then LG Display averaged higher.

[Conclusion]

The reason for the downward trend of Korean display industry is analyzed to be the fall of display panel price due to the Chinse display companies’ mass production through aggressive investment. Particularly, in or after 2017 when China’s BOE is estimated to begin Gen10.5 LCD line, LCD panel price will fall even more rapidly. This is forecast to lead Korean LCD industry to suddenly lose competitiveness. For Korean display companies that have immense LCD sales to show positive growth, it is time to expand OLED business that can be differentiated from Chinse display companies.

The only solutions for Korean display industry are OLED investment in large scale and conversion of LCD line to OLED line. At the time of BOE’s Gen10.5 line operation, Korean display companies also should respond with Gen6 flexible OLED investment and early establishment of Gen8 OLED line.

이충훈/Chief Analyst

2015년 2사분기 삼성디스플레이와 LG디스플레이의 실적을 분석한 결과 한국 디스플레이 사업이 내리막을 걷고 있는 것이 명확하게 드러났다.

[2015년 2사분기 한국 디스플레이 전체 매출 분석]

양사의 실적 발표에 의하면 2015년 2사분기 합계는 13.33조원이다. 한국 디스플레이 전체 매출은 2013년 2사분기가 16.05조원이었나 현재는 13.33조원으로 나타나며 전반적인 흐름이 하락세를 나타내고 있다.

2015년 2사분기 한국의 디스플레이 매출은 전 분기 대비 QoQ -4% 성장을 나타내었으며, 작년 동 분기에 비해서는 YoY 8% 상승을 보이고 있다.

한국 디스플레이 매출이 하락하고 있는 것은 삼성디스플레이의 실적 악화가 주된 요인이다. LG디스플레이는 최근 3년간 매출 변동이 적으나 삼성디스플레이의 매출은 점차적으로 줄어 들고 있기 때문이다.

[2015년 2사분기 한국 디스플레이 전체 영업 이익 분석]

양사의 영업 이익 합계에서 고점을 연결해 보면 하락세에 접어들어 사업성이 악화되고 있음을 알 수 있다.

이 결과 역시 삼성디스플레이의 영업 이익 감소가 크게 작용하고 있는 것으로 분석된다.

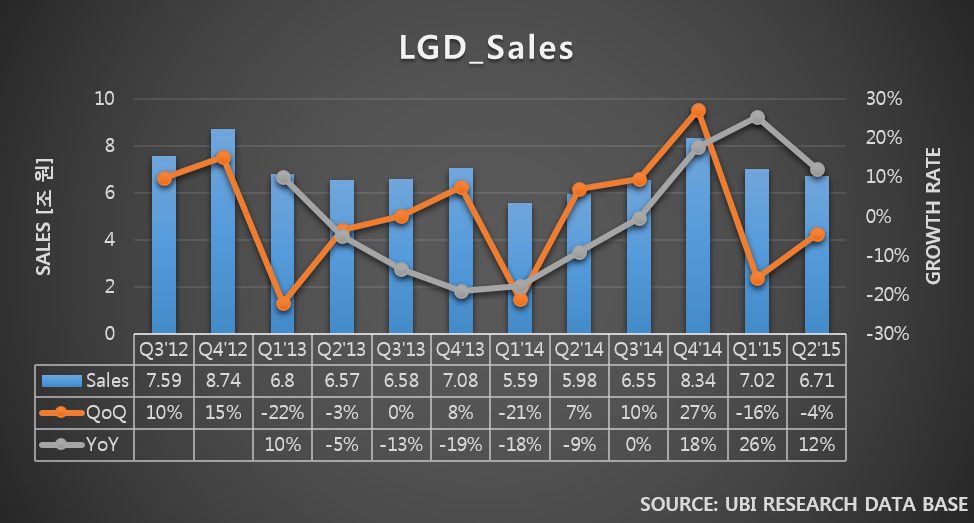

[삼성디스플레이와 LG디스플레이 매출 분석]

양사의 실적 발표에 의하면 삼성디스플레이(SDC)와 LG디스플레이(LGD)는 각각 매출 6.62조원와 6.71조원을 나타냈다. LG디스플레이는 5분기 연속 삼성디스플레이 보다 매출 우위를 점유하고 있다. 양사의 QoQ 각각 -4%(LGD)와 -3%(SDC)를, YoY는 각각 12%(LGD)와 5%(SDC)를 나타내었다. 양사의 2사분기 매출이 1사분기 대비 동시에 하락한 것은 3사분기 매출 역시 하락할 수 있음을 보여주고 있다.

[삼성디스플레이와 LG디스플레이의 경쟁력 분석]

삼성디스플레이와 LG디스플레이의 사업성을 나타내는 영업이익(profit)을 매출(sales)로 나눈 profit/sales에서 보면 2013년 3사분기까지는 삼성디스플레이가 월등한 경쟁력을 보여주었으나, 그 이후에는 평균적으로 LG디스플레이가 높게 나타나고 있다.

[마무리]

한국 디스플레이 사업이 하락세로 들어선 것은 중국 디스플레이 기업들의 공격적인 투자에 의한 대량 생산이 디스플레이 패널 가격 하락을 유도하고 있기 때문으로 분석된다. 특히 중국 BOE의 Gen10.5 LCD 라인 가동이 예상되는 2017년 이후에는 LCD 패널 가격 인하가 더욱 빨라져 한국의 LCD 사업은 경쟁력을 급격히 상실할 것으로 전망된다. LCD 매출이 압도적으로 많은 한국 디스플레이 기업들이 성장세로 돌아서기 위해서는 중국 디스플레이 기업들과 차별화 할 수 있는 OLED 사업 확대가 필요한 시점이다.

대규모 OLED 투자와 LCD 라인을 빨리 OLED 라인으로 전환해야만 한국 디스플레이 사업이 살 수 있는 유일한 대안이다. BOE의 Gen10.5 라인이 가동되는 시점에는 한국 디스플레이 기업들 역시 Gen6 flexible OLED 투자와 Gen8 OLED 라인 조기 구축으로 대응해야 한다.

Dr Choong Hoon Yi, UBI Research Chief Analyst, ubiyi@ubiresearch.co.kr

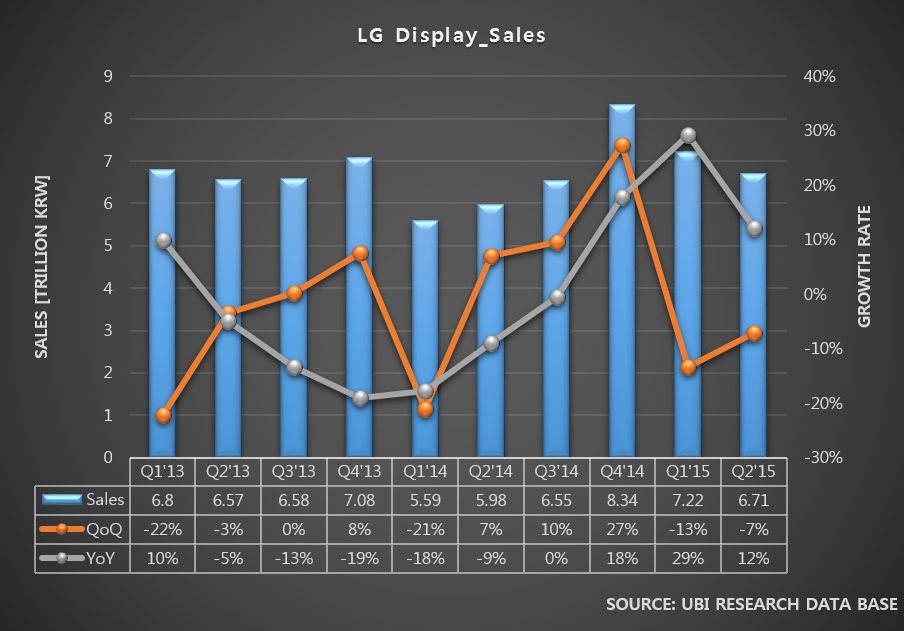

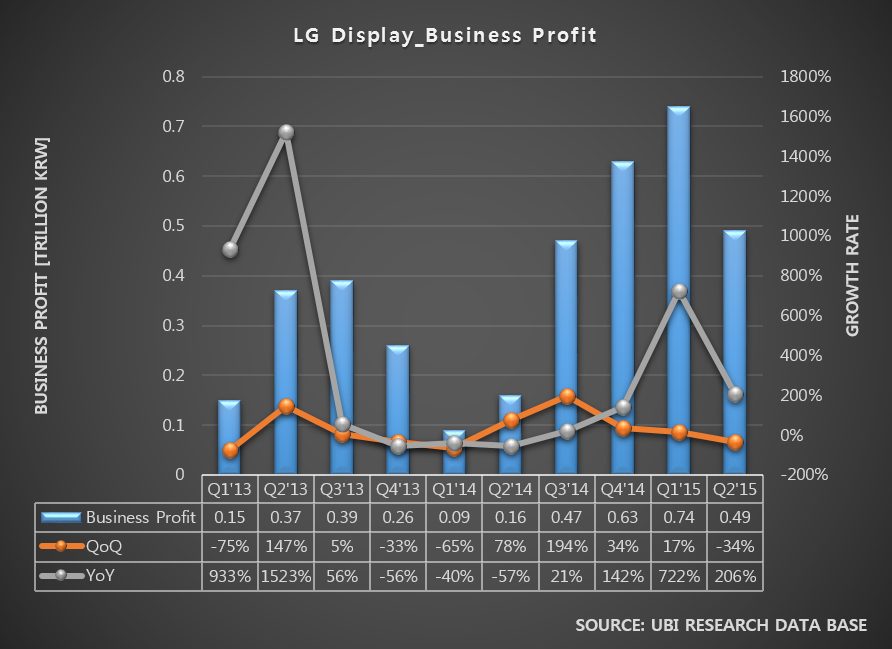

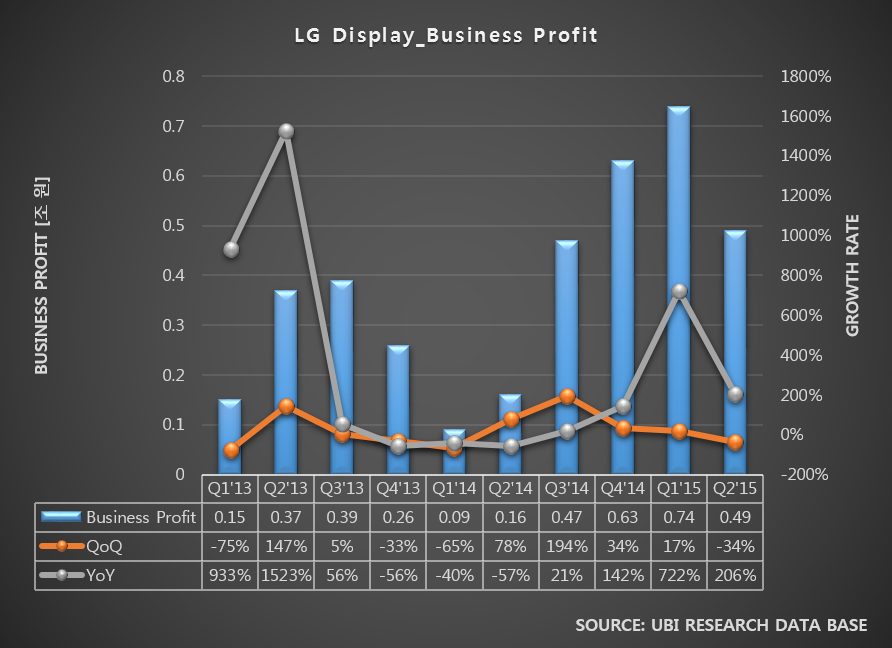

On July 23, LG Display announced its earnings results at LG Twin Towers in Yeouido, South Korea. LG Display reported that their Q2 sales recorded approximately US$ 5,700,000,000 with business profit of approximately US$ 420,000,000.

Although sales fell by approximately US$ 260,000,000 (-5%) compared to the previous quarter, it was an increase of US$ 620,000,000 (12%) compared to the year before. Business profit showed approximately US$ 210,000,000 decrease (-34%) QoQ, and YoY US$ 280,000,000 increase (206%).

LG Display’s sales and business profit of Y/Yo (green line) showed U shape of trend of growth in previous 5 quarters but this quarter recorded a fall. It is analyzed that the growth could slow down from 2H 2015.

The drop of the LG display’s Y/Yo growth in this 2Q is much attributed to smartphone market’s slow down and TV market reduction. It is also estimated the panel price reduction due to Chinese display companies’ aggressive investment is reflected.

For LG Display to stop the degrowth, mass production of products that are differentiated from competition, is urgently needed, away from LCD panel that is LGD’s current major business.

On the day, LG Display’s management announced approx. US$ 900,000,000 investment for Gen6 flexible OLED line in order to lead flexible OLED market. The investment location is Gumi factory. Investment location is Gumi factory with the initial investment of 7.5K. It is expected world’s second flexible OLED exclusive line will established following Samsung Display. It is anticipated that up to 15K will be established for this line.

Considering last year’s LG Display’s business profit was approx. US$ 1,100,000,000, the US$ 900,000,000 flexible OLED investment is very large. The investment decision must have been very difficult. However, the reasons for LG Display’s drastic flexible OLED exclusive line investment are because companies that produce LTPS-TFT LCD (LGD’s existing main market) is increasing, and because Samsung Display is already monopolizing rigid OLED market and therefore difficult to secure market share.

LG Display’s CFO Kim Sang-don explained that flexible OLED Gen6 line investment was decided at the board of directors meeting on July 22, and was made official on the morning of July 23. Kim added that the decision was reached so that LG Display can lead the OLED business in terms of technology and to occupy initial market in foldable and rollable technologies. He also commented the monthly capa. of the flexible OLED line will be 7.5K.

Regarding large area OLED panel, it was emphasized that this year’s panel production target remains to be 600,000 units and 1,500,000 units next year, same as the ones announced during the Q1 earnings results presentation. It was also revealed that 34K, approximately 9K higher than current capa., will be in operation in 2016. Addressing the concern of oversupply of next year’s 1,500,000 units while the OLD TV market is still small, LG Display suggested the solution of increasing the demand by active promotion from the second half of this year.

Despite the fall of mid to large size panels’ sales price, from the enlargement of sets and AIT technology applied sales performance, the business profit of approximately US$ 4,000 million was recorded. This is a 34% decrease compared to the previous quarter but a 199% increase from the same period in 2014. LG Display estimates that the sales will increase in the third quarter due to seasonal factors and panel’s enlargement trend.

이충훈 / Chief Analyst

7월 23일, 여의도 LG 트윈타워에서 LG Display의 실적 발표회를 개최하였다. LG Display의 지난 2사분기 매출은 6.71조원이며 영업이익은 0.49조원을 달성했다고 보고했다.

매출은 지난 분기 보다 0.31조원 감소(-5%)하였으나 지난 해 동분기 보다는 0.73조원 증가(12%)한 실적을 달성하였다. 영업 이익에서는 지난 분기 대비 0.25조원 감소(-34%), 지난 해 동 분기 대비 0.33조원 증가(206%)한 수치이다.

LG Display는 매출과 영업이익에서 지난 5분기 동안 Y/Yo(초록색 선)가 U자 커브의 성장세를 나타내었으나 이번 분기에서는 하락세를 나타내고 있다. 2015년에는 LG 디스플레이의 성장세가 둔화될 조짐이 있는 것으로 분석된다.

LG Display의 2사분기 Y/Yo 성장세 꺾임은 성장세를 유지하던 smart phone 시장 성장 둔화와 TV 시장 감소에 의한 요인이 가장 크게 작용한 것으로 분석되며 더불어 중국 디스플레이 기업들의 공격적인 투자에 의한 패널 가격 하락이 반영된 결과로 예상 된다.

LG Display가 하락 성장을 멈추기 위해서는 현재 주력 사업인 LCD 패널 위주에서 경쟁 업체들과 차별화할 수 있는 제품의 대량 생산이 시급할 것으로 분석된다.

이날 LG Display의 경영진은 플렉서블 OLED 시장 선도를 위해 1조 500억원 규모의 Gen6 플렉서블 OLED 라인 투자 결정을 공시했다. 투자 위치는 구미 공장이다. 초기 투자는 7.5K로서 삼성디스플레이에 이어 세계 2번째로 flexible OLED 전용 라인이 만들어질 예정이다. 이 라인은 추후 15K까지 증설될 것으로 예상 된다.

LG Display의 지난 해 영업 이익이 약 1.35조원이었던 점을 고려하면 flexible OLED에 1조원을 투자하는 것은 매우 큰 금액이다. 투자 결정에 매우 어려움이 컸을 것이다. 하지만 LG Display가 flexible OLED 전용 라인 투자를 과감하게 결정한 것은 기존 주력 시장인 LTPS-TFT LCD를 생산하는 기업들이 증가하고 있으며, 이미 rigid OLED에서는 삼성디스플레이가 독점 시장을 확보하고 있어 시장 확보가 쉽지 않기 때문이다.

LG Display의 CFO 김상돈 전무는 “Flexible OLED Gen6 line 투자가 어제 이사회에서 결정되었고, 오늘 아침에 공시되었다”라고 말하며 “OLED 사업에서 기술적인 우위를 가져가기 위한 결정이었고 foldable이나 rollable 기술에서도 시장 선점을 할 것이다”라고 투자 결정의 이유를 설명했다. Flexible OLED line은 월 7.5K가 가동될 것이라고 덧붙였다.

대면적 OLED panel 관련해서는 지난 1분기 실적 설명회 때 밝힌 것과 같이 올해 패널 생산 목표는 60만대, 내년 150만대임을 다시 한 번 강조하였다. 또한 2016년에는 현재 가동되는 capa.보다 약 9K 이상인 34K가 운영될 것이라고 밝혔다. 이어 아직 OLED TV의 성장이 크지 않아 내년 150만대에 대한 공급 과잉의 우려에 대해서는 올해 하반기부터 적극적인 프로모션 활동을 통해 수요를 늘리겠다는 방안을 제시했다.

한편 LG Display는 중대형 패널의 판가 하락에도 불구하고 세트의 대면적화와 AIT 기술을 이용한 실적 덕분에 영업이익은 4조 8,800억원을 기록하였다. 이는 전분기 대비 34% 하락한 수치이지만 작년 동분기 대비 199% 오른 수치이다. 3분기 실적에 대해서는 계절적 요인과 패널 대형화 트렌드가 매출 상승에 기인할 것으로 보여진다고 발표했다.

A seminar where latest technology of next generation display, OLED (Organic Light Emitting Diode), can be easily understood will take place. UBI Research, a research company specializing in OLED (http://www.ubiresearch.co.kr, president: Dr. Choong Hoon Yii), revealed that it will hold 2015 OLED Key Technology Seminar in COEX (Samseong-dong, Gangnam-gu, Seoul, South Korea) on 27 Aug.

This seminar will discuss latest issues in OLED industry such as processes in flexible OLED, encapsulation, oxide-TFT, blue phosphorous emitting material, and solution process, and focus on technology development and its future.

Encapsulation, which decides OLED panel’s final yield and lifetime, is an important process that determines exterior design in flexible OLED and large size OLED panel. It is also sensitive to light characteristics in surface light structure. At the 2015 OLED Key Technology Seminar, Dr. Choong Hoon Yi (president of UBI Research) is scheduled to introduce, through process and material analysis, essential technology needed for OLED panel to continue its growth and encapsulation technology trends.

At this seminar, Dr. Nam Sung Cho of ETRI (Electronics and Telecommunications Research Institute) will give a presentation on display technology that utilizes white OLED technology that is receiving much interest by Korean display market. He will detail white OLED technology’s present and future from lighting to large size TV.

Professor Sung Kyu Park of Chung-Ang University, will introduce oxide material that is in spotlight as display and next generation wearable device. He will also talk about internationally much discussed related technology trends and future progress.

Further presentation topics by OLED top experts include:

– AMOLED panel technology trends analysis (Hyun Jun Jang, senior researcher of UBI Research)

– Oxide-TFT technology status (Professor Ga-Won Lee, Chungnam National University)

– Solution process and vacuum evaporation OLED material’s status and forecast (Professor Sung-Ho Jin, Pusan National University)

– High efficiency blue phosphorous emitting material development trend (Professor Jun Yeob Lee, Sungkyunkwan University)

– Flexible OLED technology trend

UBI Research holds OLED Key Technology Seminars every year from 2011 and provides place for networking and sharing of information. Seminar registration can be completed through UBI Research website (www.ubiresearch.co.kr).

차세대 디스플레이로 자리매김한 유기발광다이오드(OLED)의 최신 기술 동향을 파악할수 있는 세미나 장이 마련된다.

‘OLED 전문 기업’ 유비산업리서치(http://www.ubiresearch.co.kr, 대표 이충훈)는 8월 27일(목) 서울 강남구 삼성동에 소재한 COEX에서 ‘2015 OLED 핵심 기술 세미나’를 개최한다고 밝혔다.

이번 세미나는 최신 OLED 산업에서 이슈 되고 있는 flexible OLED와 encapsulation(봉지기술), Oxide-TFT, 청색인광재료, solution process 공정 등에 대한 주제로 OLED 산업에서 주목할 만한 기술의 개발 현황과 전망에 대해 집중 소개한다.

OLED 패널에 있어서 최종 수율과 패널 수명을 결정하는 encapsulation은 Flexible OLED와 대면적 OLED 패널에서 외곽 디자인을 좌우하는 중요한 공정이며, 또한 전면 발광 구조에서는 광 특성에도 민감하게 작용한다. ‘2015 OLED 핵심 기술 세미나’에서는 유비산업리서치 이충훈 대표가 최근 OLED 주요 업체들이 사용하는 공정과 주요 재료들을 분석하여 향후 OLED 패널이 시장에서 지속 성장하기 위해 필수적으로 확보해야 할 기술과 encapsulation 기술 동향을 소개할 예정이다.

이 자리에서 한국전자통신연구원 조남성 박사는 최신 한국 디스플레이 시장에서 주목받고 있는 White OLED 기술을 기반으로 하는 디스플레이 기술에 대해 조명부터 대형 TV까지, 차세대 디스플레이의 핵심기술인 백색 OLED 기술의 현황과 미래에 대하여 설명한다.

아울러 중앙대학교 박성규 교수는 현재, 디스플레이 및 차세대 웨어러블 디바이스 소자로서 각광 받고 있는 산화물 전자소재의 특성 및 용액공정 기반으로 발전하고 있는 새로운 기술 및 응용에 대한 소개와 더불어 최근 국내외적으로 각광 받고 있는 관련 기술 동향 및 향후 발전 전망을 발표할 예정이다.

이 밖에도 ▲ AMOLED 패널 기술 동향 분석 (유비산업리서치, 장현준 선임연구원), ▲ 산화물박막트랜지스터 기술 현황 (충남대학교, 이가원 교수), ▲ 용액공정과 진공증착용 OLED 재료의 현황과 전망 (부산대학교, 진성호 교수), ▲ 고효율 청색 인광재료 개발 동향 (성균관대학교, 이준엽 교수), ▲ Flexible OLED 기술 동향, 이 OLED 최고 전문가들에 의해 다뤄진다.

유비산업리서치는 2011년부터 매년 OLED 핵심 기술 세미나를 개최 하며, OLED 전문기업으로서 OLED를 위한 가치 있는 공유의 장을 마련하고 있다. 세미나 참가신청은 유비산업리서치 홈페이지(www.ubiresearch.co.kr)를 통해 할 수 있다.

On July 23, LG Display announced its earnings results at LG Twin Towers in Yeouido, South Korea. During this event, LG Display revealed its decision to invest approximately US$ 900 million in Gen6 flexible OLED line in order to lead the flexible OLED market.

LG Display’s CFO, Kim Sang-don, explained that flexible OLED Gen6 line investment was decided at the board of directors meeting on July 22, and was made official on the morning of July 23. Kim added that the decision was reached so that LG Display can lead the OLED business in terms of technology and to occupy initial market in foldable and rollable technologies. He also commented the monthly capa. of the flexible OLED line will be 7.5K.

Regarding large area OLED panel, it was emphasized that this year’s panel production target remains to be 600,000 units and 1,500,000 units next year, same as the ones announced during the Q1 earnings results presentation. It was also revealed that 34K, approximately 9K higher than current capa., will be in operation in 2016. Addressing the concern of oversupply of next year’s 1,500,000 units while the OLD TV market is still small, LG Display suggested the solution of increasing the demand by active promotion from the second half of this year.

Despite the fall of mid to large size panels’ sales price, from the enlargement of sets and AIT technology applied sales performance, the business profit of approximately US$ 4,000 million was recorded. This is a 34% decrease compared to the previous quarter but a 199% increase from the same period in 2014. LG Display estimates that the sales will increase in the third quarter due to seasonal factors and panel’s enlargement trend.

7월 23일, 여의도 LG 트윈타워에서 LG Display의 실적 발표회를 개최하였다. 이날 LG Display의 경영진은 플렉서블 OLED 시장 선도를 위해 1조 500억원 규모의 Gen6 플렉서블 OLED 라인 투자 결정을 공시했다.

LG Display의 CFO 김상돈 전무는 “Flexible OLED Gen6 line 투자가 어제 이사회에서 결정되었고, 오늘 아침에 공시되었다”라고 말하며 “OLED 사업에서 기술적인 우위를 가져가기 위한 결정이었고 foldable이나 rollable 기술에서도 시장 선점을 할 것이다”라고 투자 결정의 이유를 설명했다. Flexible OLED line은 월 7.5K가 가동될 것이라고 덧붙였다.

대면적 OLED 패널 관련해서는 지난 1분기 실적 설명회 때 밝힌 것과 같이 올해 패널 생산 목표는 60만대, 내년 150만대 임을 다시 한 번 강조하였다. 또한 2016년에는 현재 가동되는 capa.보다 약 9K 이상인 34K가 운영될 것이라고 밝혔다. 이어 아직 OLED TV의 성장이 크지 않아 내년 150만대에 대한 공급 과잉의 우려에 대해서는 올해 하반기부터 적극적인 프로모션 활동을 통해 수요를 늘리겠다는 방안을 제시했다.

한편 LG Display는 중대형 패널의 판가 하락에도 불구하고 세트의 대면적화와 AIT 기술을 이용한 실적 덕분에 영업이익은 4조 8,800억원을 기록하였다. 이는 전분기 대비 34% 하락한 수치이지만 작년 동분기 대비 199% 오른 수치이다. 3분기 실적에 대해서는 계절적 요인과 패널 대형화 트렌드가 매출 상승에 기인할 것으로 보여진다고 발표했다.

With the active release of Apple’s smartwatch within Korean market, the interest in LG Display’s plastic OLED business is suddenly increasing.

LG Display began OLED development at the similar time as Samsung Display, but misjudgments on OLED potential and marketability led to the late market entrance and folding of the rigid OLED business. With the plastic OLED business, LG Display is matching the progress of the competitor, Samsung Display, and speeding up the development and commercialization.

Already, LG Display supplied plastic OLED for LG Elec.’s G Flex that went on sale in November 2013. Although the panel was 6inch, as the resolution was only at HD level, there was criticism that compared to Samsung Elec.’s FHD OLED which was released in the same period, the resolution fell short.

This year, LG Display supplemented the resolution and succeeded in FHD plastic OLED production. The panel is applied to G Flex 2, and it is also supplied to LG Elec.’s G Watch and Urbane.

For Samsung Elec., they intensively applied flexible OLED to the flagship smartphone model Galaxy S6 and intensified marketing; in comparison to Samsung’s smartphone market control, smartwatch’s is weaker. Accordingly, Samsung Display is mainly producing 55inch flexible OLED.

However, in contrast to the competitor, LG Display is using different business strategy for plastic OLED business. Rather than plastic OLED for smartphone, which has weak market control, they are focusing on small plastic OLED for smartwatch that is already receiving positive response.

Following the uproar within the smartwatch market, created by Samsung Elec.’s greatest rival Apple, LG Display, Apple’s supplier of plastic panel, is making all effort in panel production. Additionally, as LG Display has already secured a position as Apple’s next smartwatch plastic OLED supplier, although the capa. is lower than Samsung Display’s, the line is actively operational.

It is also estimated that LG Display will decide soon on Gen6 plastic OLED line investment to promote closer relationship with Apple. Apple is already seriously considering flexible (plastic) OLED for next iPhone series, and it is analyzed that they requested LG Display for Gen6 line investment for stable product supply.

Although LG Display does not have as high volume of clientele as Samsung Display, it is anticipated that they will establish a bridgehead in OLED panel industry through forming mutually beneficial relationship with a giant company called Apple.

LG Display’s Flexible Automotive Display, SID 2015

LG Urbane, WIS 2015

Apple이 smart watch를 한국 시장에서도 본격적으로 출시함에 따라 LG디스플레이의 plastic OLED 사업에 대한 관심이 폭증하고 있다.

OLED 개발은 삼성디스플레이와 유사한 시기에 시작하였으나 OLED 잠재력과 시장성에 대한 오판으로 시장 진입이 늦어 rigid OLED 사업을 접어야만 했던 LG디스플레이는 plastic OLED 사업에서는 경쟁업체인 삼성디스플레이와 같은 보조를 취하며 개발과 사업화를 가속하고 있다.

이미 LG디스플레이는 2013년 11월에 LG전자가 판매한 G Flex에 plastic OLED를 공급했다. 패널 크기는 6인치였지만 해상도가 HD급에 불과해 같은 시기에 판매되기 시작한 삼성전자의 FHD OLED에 비해서는 해상도가 부족하다는 지적이 있었다.

올해에는 해상도 단점을 보완하여 FHD plastic OLED 생산에 성공하여 무사히 G Flex2에 사용되었으며, 동시에 LG전자가 판매하고 있는 G Watch와 Urbane에도 패널을 공급하고 있다.

삼성전자는 플레그쉽 모델인 Galaxy S6에 flexible OLED를 전격적으로 탑재하고 마케팅을 강화함에 따라 상대적으로 smart watch는 시장 지배력이 약하다. 이에 따라 삼성디스플레이 역시 현재 생산중인 flexible OLED는 5.5인치 제품을 주로 생산하고 있다.

하지만 LG디스플레이는 경쟁 업체와는 다른 사업 전략으로 plastic OLED 사업을 진행하고 있다. 시장 지배력이 약한 smart phone용 plastic OLED 보다는 이미 시장에서 호응을 받고 있는 smart watch용의 소형 plastic OLED 생산에 집중하고 있다.

더욱이 삼성전자의 최대 라이벌인 Apple이 smart watch 시장에서 돌풍을 일으킴에 따라 Apple에 plastic watch를 공급하고 있는 LG디스플레이는 눈 코 뜰 시간 없이 바쁘게 패널 생산에 주력하고 있다. 더불어 Apple의 차기 smart watch용 plastic OLED 공급도 이미 확보하고 있어 비록 capa는 삼성디스플레이에 비해 열세지만 라인은 활발히 가동 중에 있다.

LG디스플레이는 Apple사와의 관계를 더욱 돈독히 하기 위해 조만간 Gen6 plastic OLED 라인 투자도 결정할 예정이다. 이미 Apple은 차기 iPhone 시리즈에 flexible(plastic) OLED 탑재를 신중히 검토하고 있으며, 제품 공급선을 원할히 하기 위해 LG디스플레이에 Gen6 라인 투자를 요청한 것으로 분석되고 있다.

삼성디스플레이에 비해 고객사 역량이 낮은 LG디스플레이는 Apple이라는 거대 공룡 기업과 공생 관계를 구축함에 의해 OLED 패널 사업에서 확실한 교두보를 확보할 것으로 기대된다.

LG Display’s Flexible Automotive Display, SID 2015

LG Urbane, WIS 2015

Smartphone’s hardware performance has improved as much as possible and can no longer be the differential point within the market. Following this, Samsung’s Galaxy Note 4 Edge and S6 Edge, and LG’s G-flex series are differentiating themselves from existing products through flexible (plastic) AMOLED panel applied new designs and functions. Particularly, Galaxy S6 Edge’s higher than anticipated demand means that the ratio between total Galaxy S6 and S6 Edge demand was expected to be approximately between 8:2 and 7:3, but at present it is estimated to be 5:5. To meet this demand, Samsung Display began actively operating A3 line, and carried out investment to convert A2 rigid line to flexible line.

As interest in flexible OLED is rising within the next generation smartphone market, there is much talk that Apple will also apply flexible OLED to the next product. UBI Research’s Flexible OLED Annual Report, published on 18 June, analyzed Apple’s flexible OLED application potential and forecast scenario.

According to the Flexible OLED Annual Report, other than Samsung Display, LG Display is the only company with the technology to mass produce flexible AMOLED. Japan Display and AUO also possess flexible AMOLED production technology and with investment, mass production is analyzed to be possible. Therefore, for the Apple to apply flexible OLED to the iPhone series to be released in 2017, the Gen 6 flexible AMOLED line investment of LG Display, Japan Display, or AUO has to be carried out within 2015. However, as Japan Display and AUO’s mass production technology has not been verified, depending on the currently mass producing LG Display’s Gen 6 line investment timing the flexible OLED applied iPhone release date will be decided.

As the results of analyzing future model’s shipment based on the analysis of iPhone series’ sales progress so far, to meet the demand for Apple’s flexible AMOLED applied model’s shipment in 2020, approximately 170K monthly capa. by Gen 6 (considering operation and yield rate) is needed. Considering the recent trend of 20K capa. per 1 line, 8 or 9 flexible AMOLED line are required, and Apple’s future flexible AMOLED line investment is estimated to be actively carried out.

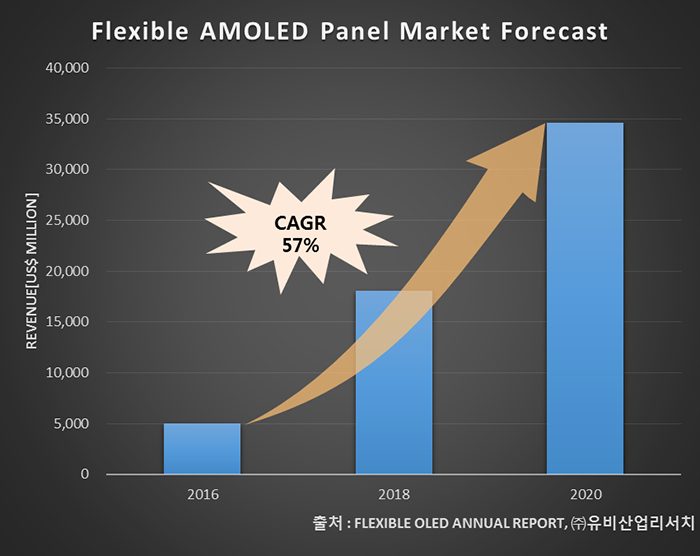

On the other hand, flexible AMOLED market is forecast to grow at 57% CAGR from 2016, and show approximately US$ 35,000 million revenue in 2020.

스마트폰 시장에서 하드웨어성능은 높아질 만큼 높아져 더 이상 차별화 포인트가 될 수 없어졌다. 이에 따라 Samsung의 Galaxy Note4 Edge와 S6 Edge, LG의 G-flex 시리즈는 기존의 flexible(plastic) AMOLED panel을 적용하여 새로운 디자인과 기능으로 기존 제품과 차별화 하고 있다. 특히 Galaxy S6 Edge는 기대보다 높은 수요를 보이고 있어 전체 Galaxy S6와 S6 Edge의 비율을 약 8:2 에서 7:3정도로 예상했었지만 현재는 약 5:5 정도가 될 것으로 예상되고 있다. 이에 따라 Samsung Display에서도 물량을 맞추기 위해 A3 line의 본격 가동하고 A2 line의 rigid line을 flexible line으로 전환투자를 진행하였다.

이처럼 차세대 스마트폰 시장에서 flexible OLED에 대한 관심이 높아지면서 Apple도 차기 제품에 flexible OLED를 적용할 것이라는 소문이 무성하다. 유비산업리서치에서 18일에 발간한 “Flexible OLED Annual Report”에서는 Apple의 flexible OLED 적용 가능성과 예상 시나리오를 분석하였다.

Flexible OLED Annual Report에 따르면, Samsung Display 이외에 flexible AMOLED를 양산할 수 있는 기술을 가진 업체는 LG Display가 유일하며, Japan Display와 AUO도 flexible AMOLED 제조 기술을 보유하여 투자가 이루어진다면 양산은 가능할 것으로 분석된다. 따라서, Apple이 2017년에 출시될 iPhone series에 flexible OLED를 적용하기 위해서는 LG Display와 Japan Display 또는 AUO의 Gen6 flexible AMOLED line 투자가 2015년 안에 이루어져야 할 것으로 보았다. 하지만 Japan Display와 AUO의 양산 기술은 검증되지 않았기 때문에 현재 양산을 진행하고 있는 LG Display의 Gen6 line 투자 시점에 따라 flexible OLED가 적용된 iPhone을 볼 시점이 정해질 것으로 내다봤다.

또한 iPhone series의 그 동안의 판매 추이를 분석하여 앞으로 출시될 신 모델의 출하량을 분석한 결과, 2020년 Apple의 flexible AMOLED가 적용된 모델들의 출하량을 소화하기 위해서는 Gen6 기준 월 약 170K(가동률과 수율 고려)가 필요한 것으로 나타났다. 이는 최근 추세가 1 line당 20K인 것을 감안하면 약 8~9개의 flexible AMOLED line이 필요한 것으로, Apple 향(向)의 flexible AMOLED line 투자가 본격적으로 이루어질 것으로 예상된다.

한편 flexible AMOLED 시장은 2016년부터 연평균 57%로 성장하여 2020년에 약 US$ 35,000 million의 시장을 형성할 것으로 내다봤다.

Japan Display (JDI) revealed product level of flexible OLED exceeding the demonstration standard of OLED panel exhibition. JDI has been carrying out white OLED panel development for several years, and had shown 5.2 inch flexible AMOLED panel in Display Innovation 2014.

5.2 inch flexible OLED panel revealed in SID 2015 is similar to last year’s flexible panel. It is 5 inch FHD (423ppi) with 0.05mm thickness and pixel structure formed by combining white OLED and color filter. LTPS TFT was used for backplane.

Flexible OLED produced by Samsung Display and LG Display has RGB structure. While the resolution is FHD, as it uses pentile type drive the actual resolution is about 320ppi. However, flexible OLED revealed by JDI has white OLED structure, which is structurally similar to WRGB OLED for OLED TV currently being produced by LG Display.

Japan Display (JDI)가 단순한 데모 수준의 OLED 패널 전시를 넘어 제품 수준 단계의 flexible OLED를 SID2015에서 공개했다. JDI는 이미 white OLED 패널 개발을 수년 전부터 진행해 왔으며, Display Innovation 2014에서도 5.2inch flexible AMOLED panel을 공개한 바 있다.

이번 SID 2015에 공개된 5.2inch flexible OLED panel도 작년에 공개한 flexible panel과 같은 panel 이며, 0.05mm의 5.2인치 FHD(423ppi), 화소 구조는 white OLED와 color filter를 혼합하여 만들었다. Backplane은 LTPS TFT를 사용했다.

삼성디스플레이와 LG디스플레이가 생산하는 flexible OLED는 RGB 구조로서 해상도는 FHD급이나 pentile 방식의 구동을 사용하고 있어 실제 해상도는 320ppi 정도이다. 하지만 JDI가 공개한 flexile OLED는 white OLED 구조로서 현재 LG디스플레이가 생산하고 있는 OLED TV용 WRGB OLED와 구조가 유사한 구조이다.

Supported by the success of WOLED production for OLED TVs, LG Display is ambitiously formulating the next project with the plastic OLED. The development of dual-edge plastic OLED was completed as an extension of the plastic OLED product already used in LG’s G Flex and G Watch, and the product for automobile dash board is under preparation.