BOE, Fuzhou에 6세대 flexible OLED 라인 투자 서명

2018년 12월 26일 BOE는 푸저우(Fuzhou) 주정부와 6세대 flexible OLED 라인 프로젝트에 서명하였다.

공장 건설 장소는 Fuqing시이며 월 48K의 6세대 flexible OLED 라인이다. 총 투자 금액은 465억 위안이다.

2018년 12월 26일 BOE는 푸저우(Fuzhou) 주정부와 6세대 flexible OLED 라인 프로젝트에 서명하였다.

공장 건설 장소는 Fuqing시이며 월 48K의 6세대 flexible OLED 라인이다. 총 투자 금액은 465억 위안이다.

BOE가 B7과 B11 플렉스블 OLED 공장에 이어 B12 공장 착공식에 들어갔다. 삼성디스플레이가 독점하고 있는 플렉스블 OLED 사업 흐름을 차단하기 위해 중국과 일본 패널 업체들의 추격이 시작된 가운데 BOE는 자국내 막대한 스마트폰 시장을 노리고 투자를 지속하고 있다.

일본에서는 유일하게 샤프가 플렉스블 OLED 양산을 시작하며 자사의 휴대폰에 패널을 탑재하기 시작했으며, BOE는 중국내 세트 업체를 겨냥하여 소량이지만 패널을 양산하고 있다. 여기에 비저녹스도 구안공장에서 플렉스블 OLED 양산을 위한 마지막 수율 조정 작업에 열을 올리고 있다. 내년에는 삼성디스플레이와 엘지디스플레이에 이어 중국과 일본에서도 플렉스블 OLED 생산량이 증가하며 시장 경쟁이 가속화될 전망이다.

이러한 각축속에서 BOE는 삼성디스플레이에 이어 최대 규모의 공장을 연이어 짓고 있다. B7 공장의 수율이 아직 충분히 확보되지 않은 상황이지만 시간이 가면 언젠가는 된다는 중국 특유의 뚝심으로 플렉스블 OLED 공장 건설을 지속하고 있다. 중국 정부의 지원은 수익이 나지 않는 플렉스블 OLED 투자를 가능하게 하고 있다.

중국 기업들중에서 BOE가 투자에 집중하고 있는 이유는 2가지로 볼 수 있다. 첫째는 LCD 패널가격이 지속적으로 하락하고 있는 상황에서 매출과 영업 이익을 동시에 확보할 수 있는 OLED는 BOE의 성장에 필수적이 요소이기 때문이다. 두번째는 중국내 다른 패널 기업들 보다 한발 앞선 투자로서 향후 다가올 경쟁 상황에서 주도권을 확보하기 위한 것이다. 중국 정부가 주도하는 2025 프로젝트가 끝나면 디스플레이 업체에 대한 투자가 줄어들 수 있다. 이러한 상황을 미리 대비하여 공장을 조기에 확보하면 추후 발생할 수 있는 중국내 업체간 경쟁에서 조기 감가상각을 통해 원가 경쟁력을 빠르게 확보할 수 있으며, 또한 중국내 스마트폰 고객 업체들을 미리 선점할 수 있다. 대량 생산 체제가 완성되면 다양한 중국내 고객들에게 안정적으로 제품을 공급할 수 있기 때문에 삼성디스플레이와 엘지디스플레이의 중국 시장을 뺏어 올 수 있다. 대량 생산 체제가 되면 부품소재 구매비를 낮출수 있기 때문에 공격적인 마케팅도 가능해진다.

BOE가 아직은 낮은 수율로 인해 대량 생산에는 시간이 걸릴 수 있지만 삼성디스플레이와 엘지디스플레이의 플렉스블 OLED 사업을 위협할 수 있는 경쟁업체로 부상하게 될 것이다.

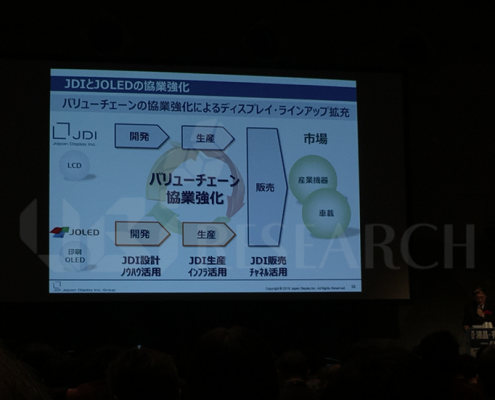

2018년 12월 5일부터 7일까지 일본 도쿄에서 열리고 있는 28TH FINETECH JAPAN에서 JDI와 JOLED는 중형 OLED 시장을 공략하기 위해 협력을 강화한다고 밝혔다.

JDI는 JDI만의 설계 노하우와 생산 인프라, 판매 채널을 통해 JOLED의 solution process OLED를 산업기기용 디스플레이 시장이나 자동차용 디스플레이 시장 등 중형 OLED 시장에 적극 공략할 것을 발표했다.

특히, JDI는 전자 미러나 A/B 필러용 디스플레이 등 안전을 위한 서포트와 새로운 인터페이스 기능, 4~8K 디스플레이를 활용한 영화 감상, 곡면과 대화면 등 인테리어와 조화를 이룬 디스플레이 등 JOLED와 함께 차세대 자동차 분야에 새로운 가치를 제공할 것을 밝혔다.

JDI와 JOLED는 전시장 부스도 공유하였다. JOLED는 e-sports용과 의료 분야용 전문 21.6인치 FHD OLED 모니터를 선보였으며, 자동차용 12.3인치 HD OLED와 12.2인치 FHD flexible OLED, 집 내부용 27인치 4K OLED, 원기둥 형태의 21.6 인치 4K flexible OLED 등 다수의 중형 OLED와 54.6인치 4K OLED 등 대형 OLED를 선보였다.

한편, JOLED는 지난 7월 solution process OLED 양산을 위한 노미 사업소를 개설한다고 밝힌 바 있다. 노미 사업장은 5.5세대 유리 기판 기준으로 월 생산 2만장의 생산 능력을 갖추고 2020년 양산을 목표로 하고 있다.

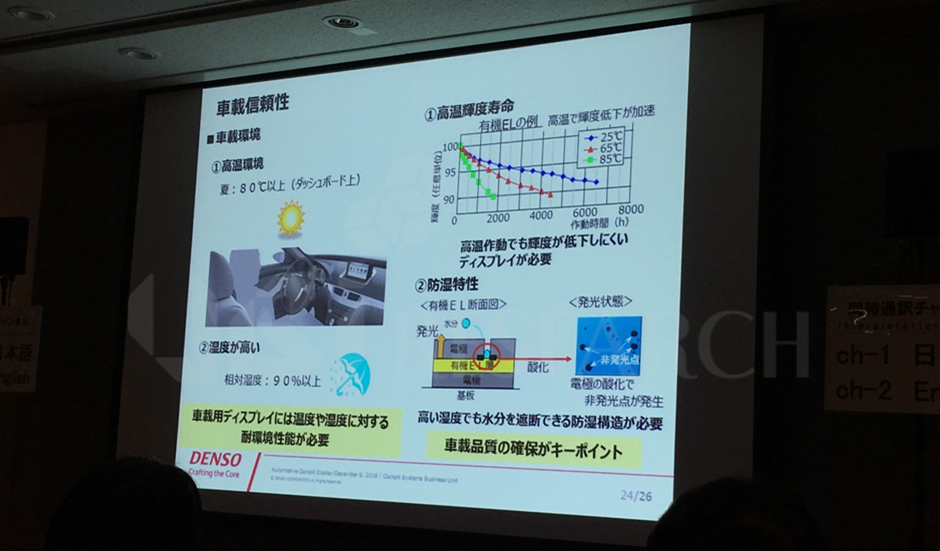

2018년 12월 5일부터 7일까지 일본 Makuhari Messe에서 열리는 28th FINETECH JAPAN에서 Denso의 Hiroyuki Hara manager는 OLED가 다양한 장점으로 인해 미래의 자동차용 디스플레이로 중용될 것이라고 의견을 밝혔다.

Hara manager는 자동차용 디스플레이의 최신 트렌드로 터치 패널을 포함한 대형 화면을 언급하며 현재는 LCD가 많이 쓰이고 있지만 전장 업체와 운전자들이 고화질의 디스플레이를 요구하는 만큼 OLED가 해를 거듭할수록 자동차 내부에서 쓰임새가 많아질 것으로 예상했다.

이어서 Hara manager는 자동차용 디스플레이의 중요한 요소로 높은 명암비와 넓은 시야각, 디자인 자율성, 경량화, 저반사, 신뢰성 등을 언급하며 이 모두를 아우를 수 있는 디스플레이는 OLED라고 강조했다. 또한, 명암비나 시야각 등 화질에 관련 된 요소는 운전자에게 바로 안전과 직결되는 요소이기 때문에 OLED가 더욱 더 많이 사용될 수 밖에 없는 상황이라 밝혔다.

마지막으로, Hara manager는 자동차용 OLED의 요구 사항을 언급하며 온도 변화에 따른 휘도 저하 절감이나 높은 습도에 의한 OLED의 훼손 방지 등의 신뢰성 향상이 자동차용 디스플레이 시장 진입을 위한 OLED의 중요한 열쇠가 될 것이라 언급하며 발표를 마쳤다.

자동차용 디스플레이 시장은 모바일 기기와 TV에 이어 차세대 디스플레이 시장으로 주목받는 대표적인 시장으로써 LG 디스플레이와 삼성 디스플레이 뿐만 아니라 BOE나 Visionox 등 다양한 OLED 패널업체들이 국내외 전시회에서 자동차용 디스플레이를 선보이고 있다. Denso 또한 한국 패널 업체들과 경쟁을 위해 2018년 초 JOLED에 300억엔을 투자한 바 있다.

한편, UBI Research에서 최근 발간한 “자동차용 OLED 디스플레이 보고서”에 의하면 삼성 디스플레이와 LG 디스플레이가 이끄는 자동차용 OLED 디스플레이 시장은 2023년에는 5.4억달러 시장으로 성장할 전망이다.

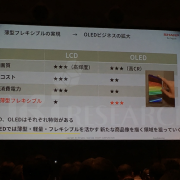

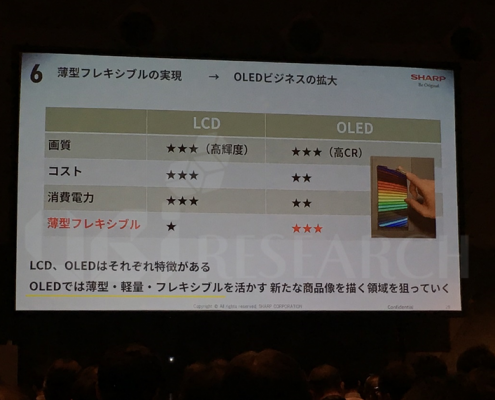

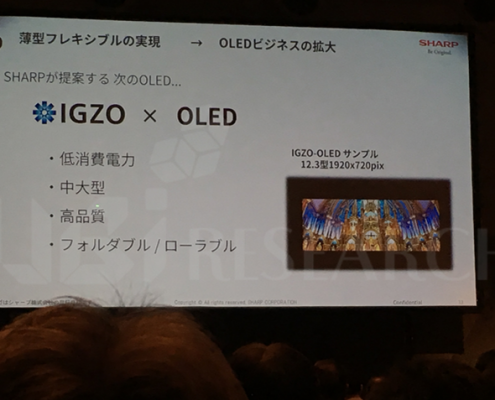

2018년 12월 5일부터 일본 Makuhari Messe에서 열리고 있는 28th FINETECH JAPAN에서 Sharp의Atsushi Ban 부사장은 keynote session을 통해 IGZO와 OLED를 결합한 미래 전략을 발표하였다.

Ban 부사장은 “전체 디스플레이 시장에서 OLED의 비중은 더욱 더 높아질 것으로 예상되며 OLED만의 새로운 가치는 다름아닌 flexibility”라고 강조하였다.

이어서 Ban 부사장은 “Sharp 또한 OLED만의 얇고 가벼우며 flexible의 특징을 이용하여 다양한 응용 제품을 계획하고 있다”고 밝히며 “2018년 3분기부터 Taki 공장에서 4.5세대 backplane을 생산하고 Sakai 공장에서 4.5세대 15K 분량의 OLED용 glass 투입과 모듈 공정을 진행하고 있다”고 발표하였다.

또한 Ban 부사장은 flexible OLED를 통해 OLED 산업의 확장 가능성을 언급하며 Sharp의 다음 목표는 IGZO를 결합한 foldable OLED 개발이라고 밝혔다. 특히 Ban 부사장은 IGZO가 저전력 소모가 가능하고 중형과 대형 사이즈에서 고화질을 지원할 수 있다고 장점들을 열거하며, 이러한 IGZO가 중대형 foldable OLED나 rollable OLED와 결합한다면 새로운 가치를 창출 할 수 있을 것으로 기대했다.

마지막으로 Ban 부사장은 Sharp의 IGZO 개발 로드맵을 소개하며 구동 능력이 더욱 향상 된 IGZO를 개발할 것이라 밝히며 발표를 마쳤다.

파인텍 재팬에서 JOED가 처음으로 부스를 열었다.

파나소닉의 잉크젯 OLED 기술을 전수 받아 OLED 패널 사업을 하고 있는 JOLED는 올해 초부터 의료용 모니터를 판매하고 있다. 내년에는 Asus에서 JOLED에서 만든 잉크젯 OLED TV도 판매할 예정이다.

전시 제품은 의료용 OLED 모니터와 게임용 OLED 모니터를 포함하여 차량용 OLED, OLED TV 3 종류이다.

JOLED의 잉크젯 OLED는 공통적으로 peak intensity가 350nit이며 full white는 140nit이지만 모니터용으로는 충분한 휘도를 보유한 것으로 판단된다.

JOLED는 내년에 양산라인을 구축하여 20인치대 모니터용과 TV용 OLED를 본격적으로 생산할 예정이며 2020년 이후에는 자동차용 OLED 사업을 계획하고 있다.

JOLED는 잉크젯 기술로서 제작한 OLED 패널을 생산하고 있는 유일한 기업이다. JOLED는 이 기술을 중국과 일본, 대만 패널에 제공하여 라인센스 사업도 동시에 추진중에 있다.

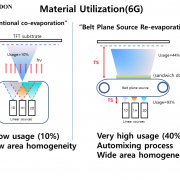

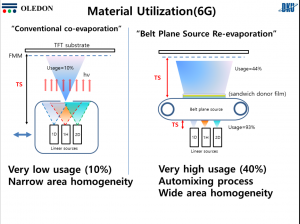

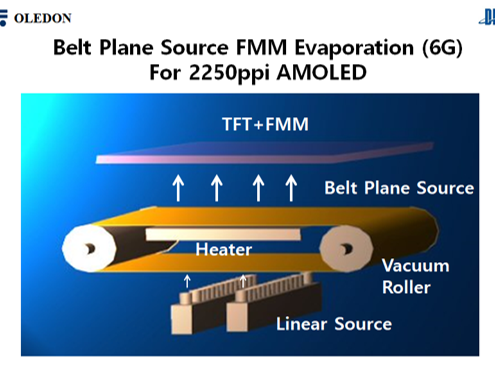

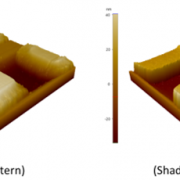

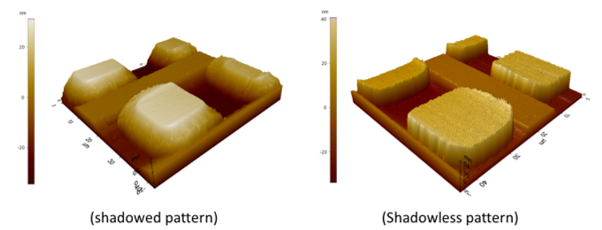

세계최초로 면소스증착 장비를 개발하는 단국대 벤처회사인 OLEDON사 (대표: 황창훈)는 11월30일 코엑스에서 열린 유비산업리서치 2018년 OLED 산업결산 세미나에서 양산용 “초격차” AMOLED 제조 기술인 벨트면소스 FMM 증착기술을 개발했다고 발표했다. 벨트면소스 FMM증착기술은 리니어소스로 호스트와 도판트 유기물을 벨트금속면에 차례로 증착하여 도너박막을 형성한다. 이후에는 연속으로 벨트금속을 이송하여 도너박막의 상향식 수직재증발을 유도한 후 초미세 패턴(800ppi~2250ppi)의 타겟박막을 형성하는 개념이다. 이 기술은 기존의 리니어소스 증착의 동시증발(co-evaporation)증착 기술과는 완전히 다르다. 황창훈박사의 설명에 따르면, 호스트와 도판트 박막을 적층하여 한번에 재증발하는 벨트면소스 증착공정은 완전히 새로운 방식의 “오토믹싱 재증발(automixing re-evaporation)” 공정이라고 하면서, 이 공정을 이용하면 발광물질 사용율을 4배까지 향상하는 효과가 있다. 현재 리니어소스의 co-evaporation공정의 물질사용효율은 불과 10퍼센트에 불과한 것으로 알려져 있다.(아래 사진참고) 이 밖에도, 벨트면소스 증착기술은 발광층의 도핑그래디언트(doping gradient)를 자유롭게 조절 가능하여, 특히 블루발광효율이 향상될 것으로 기대되기도 한다. (참고논문, SR forrest, “Tenfold increase in the lifetime of blue phosphorescent OLED, nature communication (2014))

(사진: Auto-mixing Re-evaporation 공정, source : OLEDON)

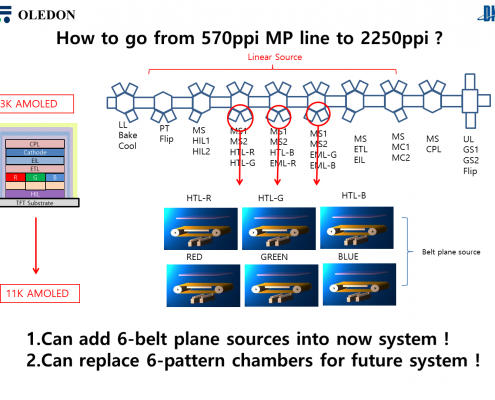

황창훈대표는 벨트면소스 FMM증착기술을 기존의 6세대 리니어소스 FMM 증착기에 바로 적용하여 초고해상도(800ppi~2250ppi)의 AMOLED 소자의 대량 생산 공정을 개발할 필요가 있다고 발표했다. 이론적으로 기존의 리니어 소스 FMM 증착기에 벨트면소스를 12개 설치하면 AMOLED의 해상도를 획기적으로 향상하게 된다는 아이디어이다.(아래 사진 참고)

(사진: 11K AMOLED제조용 벨트형 면소스FMM 증착, source : OLEDON)

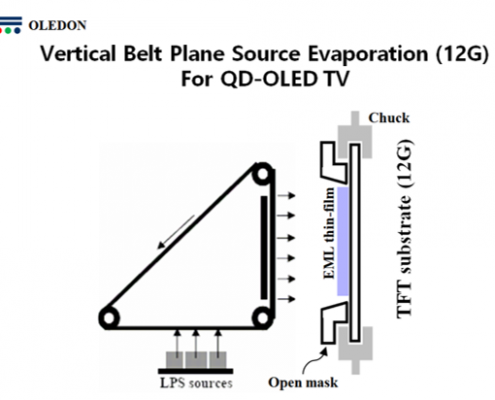

황창훈대표는 또한, 인라인 증착기에서 발생할 것으로 보이는 Footprint문제, 기판처짐문제, 생산성문제를 해결하여, 77인치 QD OLED TV의 대량 생산에 성공하려면, 12세대급의 대형 프레임드 기판척과 초대형 수직벨트면소스를 이용하는 클러스터형 증착기를 개발해야 한다고 발표하기도 하여 관심을 모았다. 한편 올레드온사는 면소스 및 벨트면소스 증착기에 대한 원천특허를 포함하여, 초대형 프레임드기판척과 초대형 수직벨트면소스 증착기에 관련한 34편의 특허를 보유하고 있다.

(사진: 면소스 및 벨트면소스 증착기 원천특허, source : OLEDON)

OLEDWorks는 최근 flexible OLED 조명을 이용한 LumiCurve 제품군의 플랫폼인 ‘Wave’의 출시를 발표하였다.

<OLEDWorks의 Wave 조명, source: oledworks.com>

Wave의 기판은 Corning의 ‘Willow glass’가 적용되었다. Willow glass는 0.1 mm 두께의 thin glass로 고유한 밀폐 차단 특성이 있어 조명 패널의 내구성과 수명을 손상시키지 않으면서 뛰어난 광 품질과 우수한 색 재현율을 제공할 수 있다고 OLEDWorks는 설명하였다.

Wave FL300C 제품은 warm white와 neutral white 등 두가지 제품으로 출시되었으며, warm white 제품의 최대 밝기는 300 루멘, 효율은 100 루멘 기준 62 lm/W, 온도는 3000 K, CRI는 90이다. Neutral white 제품의 최대 밝기는 250 루멘, 효율은 100 루멘 기준 47 lm/W, 색온도는 4000 K, CRI는 90이다. 두 제품의 수명은 모두 50,000 시간이며 최소 곡률 반경은 10 cm이다.

현재 디스플레이로 모바일 기기와 TV에 적극 적용되고 있는 OLED는 고유의 면발광 특징으로 조명 시장에서 실내 조명 뿐만 아니라 차량용 조명, 전시용 조명 등 다양한 분야에 걸쳐 적용되고 있다.

신제품을 출시하고 있는 OLEDWorks 뿐만 아니라 조명용 OLED 패널을 대규모로 양산할 수 있는 LG Display도 CES 2019에서 다양한 OLED 조명을 선보일 것으로 예측 되는 등 OLED 조명 시장이 본격적으로 확대될지 귀추가 주목되고 있다.

신개념의 OLED 증착장비 개발 벤처회사인 OLEDON사 (대표: 황창훈)는 11월30일 코엑스에서 열리는 유비산업리서치 2018년 OLED 산업결산 세미나에서 양산용 “초격차” AMOLED 제조 기술인 벨트면소스 FMM 증착기술과 “초대면적” QD-OLED TV 제조용 수직 벨트면소스 증착기술을 발표할 예정이다.

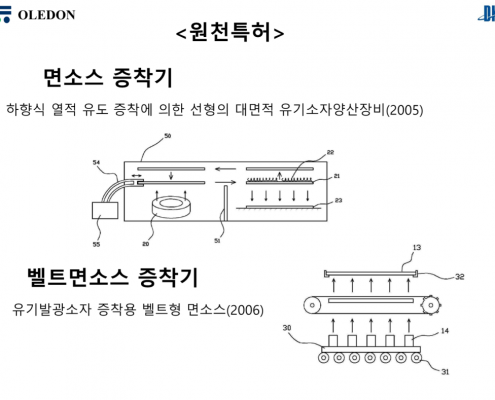

올레드온사에서 세계최초로 이미 개발에 성공한 면소스의 증착원리는 금속면에 1차 유기물을 증착하고 난뒤, 이를 상향식으로 재증발하여 유기물 기체의 수직증발을 유도하여 2250ppi의 초고해상도의 미세 패턴을 제작하는 신개념 증착기술이다. 이러한 면소스 공정에는 1차증착, 면소스 인버전, 2차 증발의 세가지 공정이 필수적이며, 양산에 적용 시 그에 따른 고진공챔버의 수도 증가한다. 이번에 올레드온에서 소개하는 벨트면소스 FMM 증착기술은 한 증착기내에서 위의 여러기능을 한번에 하는 개념으로서, 금속면을 벨트형태로 구성한 연속 면소스 공급형 증착기술이다.

(사진: 벨트형 면소스FMM 증착기, Source : OLEDON)

황창훈대표의 설명에 따르면, 벨트면소스를 이용하면, 증착챔버를 새로이 제작하지 않고도, 기존의 6세대 리니어소스 FMM 증착기에 바로 적용이 가능한 개념이라고 밝혔다. 이를 활용하면, 조만간, 스마트폰에 탑재하는 AMOLED 소자와 VR 디스플레이의 해상도가 획기적으로 향상될 것으로 보인다.

또한 황창훈대표는 수직벨트면소스를 사용하면, QD-OLED TV용 12세대급 초대면적 기판을 처짐 없이 원활한 증착공정이 가능하다고 밝혔다. 수직벨트면소스 증착기는 기판을 세워서 증착하는 개념으로, 프레임드기판척(framed glass chuck)과 오픈마스크의 하중부담이 매우 적어져 로봇이송이 용이하고, 정지상태에서 균일한 초대면적 박막의 증착공정이 가능하여, 8세대는 물론, 향후 10세대이상 기판크기의 클러스터형 양산용 증착기에 활용이 가능할 것으로 보인다.

(사진: QD-OLED제조용 수직벨트형 면소스 증착기. Source : OLEDON)

황창훈대표는 최근 블루물질의 물질변성시험과 블루도판트 증착시험을 성공적으로 마쳤다고 밝히며, 한국이 현재의 OLED 생산국 1위를 유지하려면, 창의적 핵심증착 기술개발 도전에 적극 투자하여야 한다고 하며, 미래형 중소형 및 대형 OLED 제조는 모두 면소스 증착기술을 사용하게 될것이라고 전망했다. 한편 올레드온사는 면소스 및 벨트면소스 증착기에 대한 원천특허를 포함하여 30여편의 관련 특허를 보유하고 있으며, 최근 양산용 수직벨트면소스증착기에 관련한 특허를 출원하기도 하였다.

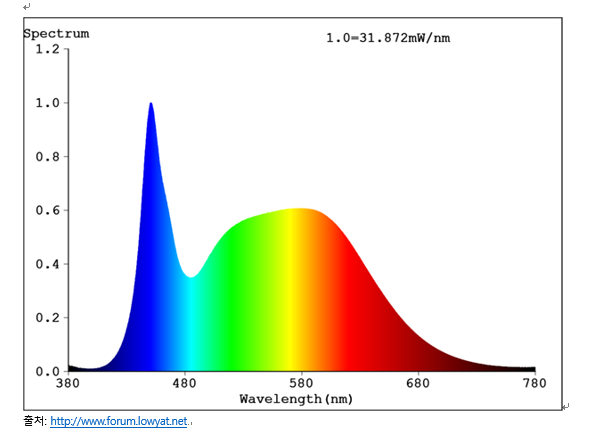

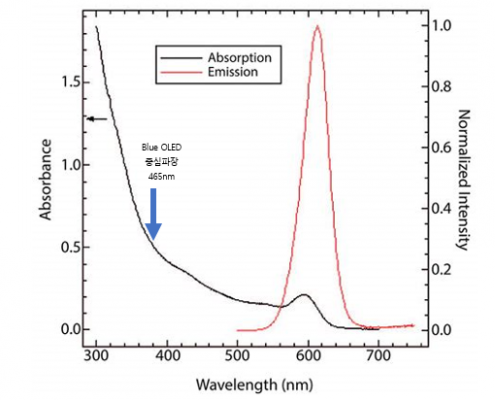

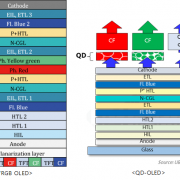

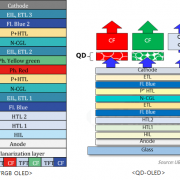

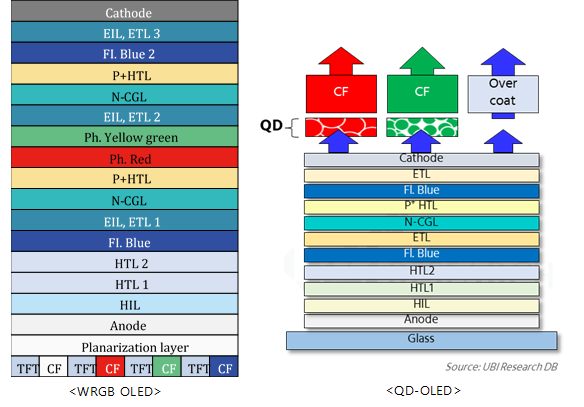

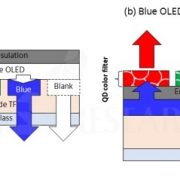

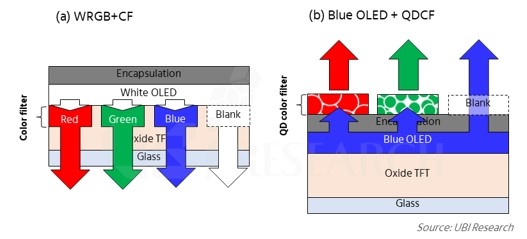

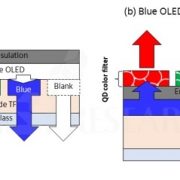

최근 삼성디스플레이의 프리미엄 TV 패널용 QD-OLED 개발이 디스플레이 산업의 화두가 되고 있다. 현재 TV 용 OLED 패널을 단독 공급하고 있는 LG 디스플레이는 White OLED(WOLED) 방식을 사용하고 있으며 RGB 효율을 지속적으로 개선시켜 나가야 하는 것을 목표로 하고 있다.

위 그림은 LG디스플레이의 WOLED의 Spectrum이다.

일반적으로 Blue OLED는 낮은 수명과 효율과 휘도의 문제를 가지고 있다고 알려져 있다. Blue는 휘도에 기여도는 낮지만 에너지로서 강하다. 마치 우리 눈에 보이지 않지만 강한 에너지를 가지는 UV와 같다고 할 수 있다. Blue광원에 적절한 형광체를 사용한다면 충분히 휘도를 얻을 수 있다.

위의 Graph를 기준으로 단순한 Simulation을 해 볼 수 있다.

만약 Blue의 에너지가 100%일 경우 Blue와 Green의 파장 차이는 13%를 반영할 경우 Blue Quantum의 개수는 Green의 약105% 이다. 여기에 이론적인 QD의EQE 85%를 계산하면 약 89% 휘도를 얻을 수 있다. 그러나 실제는 여러가지 변수가 있기 때문에 실제의 휘도는 약 70% 수준으로 예상된다.

결론적으로 400nit를 구현하기 필요한 Blue의 에너지로 약 300nit의 빛을 낼 수 있을 것으로 예상된다. 물론 이 수치는 만족할 수준의 수치가 아니다. 다시 말하면 색 재현성 혹은 색온도를 높이기 위해 WOLED는 QD-OLED 보다 더 많은 에너지가 필요하다.

OLED의 재료와 Device관점에서 보면 Blue의 성능은 Red와 Green에 비해 뒤떨어져 있다. RG는 이미 인광재료를 채용해 효율의 한계치에 근접해 있는 반면 Blue는 아직도 형광재료에 묶여 있고 휘도 문제로 여전히 효율과 수명 제약이 있다.

몇 년전부터 Blue 재료의 개선을 위한 방법 중 하나로 삼성과 엘지에서 TADF 기술에 관심을 보이고 투자를 해왔다. TADF는 지금 당장은 아직 완벽한 기술은 아니다. 그러나 인광재료처럼 산업적 요구가 강해지고 투자되는 Infra가 커지면 산업화는 앞당겨 질 수 있다. 그러나 현실적으로 Blue의 기여도가 낮으면 그 속도는 더디겠지만 그 요구가 명확하고 그에 따는 투자가 강화된다면 Blue 재료 개선을 위해 한가지 해결책이 될 수 있을 것이라는 것이 업계 종사자들의 예상이다.

그렇다면, Blue 재료의 개선만 있으면 QD-OLED는 현재 WOLED TV보다 월등한 제품을 만들 수 있는 기술인가?

먼저 QD와 CF를 같이 만드는 경우라면EQE는 예상보다 나쁘다.

PL 현상과 CF는 원리상 양립한다는 것은 모순이 되기 때문에 결과적으로 CF와 QD층은 분층이 되어야 한다

QD는 가능한 많은Blue 광원이 입사하거나 입사된 광원이 가능한 많은 QD particle과 만나야 EQE는 증가할 것인데, CF는 반대로 Blue광원을 차단하는 성질이 있기 때문에 두께는 올리는데 한계가 있을 수 있다. 실제로 QD+CF(6㎛ 두께 기준) 에서PL의 EQE는 약 25% 전후이다.

QD입장에서 적절한 QD을 통과해서 충분히 광변환을 한 후 잉여의 Blue 광원을 CF를 통해서 차단하는 것이 가장 효율이 높을 것으로 예상된다

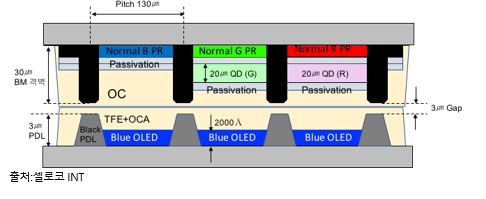

현재 사용하는 QD film에서 QD 층의 두께는 대략 100㎛이고 QD의 Volume Density는 약 1%이다. 이 상태에서 EQE는 85% 정도라고 알려져 있습니다. 그래서 실제로는 아래와 같은 구조가 되는 것이 더 효율적이다.

이 구조의 핵심적인 아이디어는 3가지이다. 첫번째는QD와 CF를 분리한다는 것, 두번째는 QD재료는 R,G를 분리한다는 것, 마지막은 1%의 Volume Density를 5%로 높인다는 것이다. 이렇게 되면 아마도 EQE는 80%수준에 근접해서 휘도 저하는 크지 않을 것이다.

위 구조를 실현하기 위해서 몇 가지 공정이 추가적으로 개발되어야 한다.

BM격벽을 높게 형성하여 되는데 이것은 PDP에서 이미 개발된 공정이 있어서 차용이 가능할 것이다. 두번째는 20㎛ 두께의 QD의 선택적 증착인데 이는 장Nozzle Printing을 통해 극복이 가능할 것으로 보인다.

현재 가장 큰 개발 이슈는 QD의 PL의 파장과 Blue OLED의 발광 파장이 차이가 있다는 것이다.

QD의 경우는 UV로 갈수록 PL을 일으키는 흡수율이 증가한다.

반면에 Blue OLED는 발광의 중심이 465nm 이상에 있기 때문에 실제로 PL을 통한 System전체의 발광 효율은 낮게 나온다. QD CF의 흡수파장을 좀 더 높이는 구조나 혹은 OLED의 발광파장을 낮추는 개선이 필요하다.

OLED와 QD를 광학적으로 하나의 System으로 구현하려는 시도는 이미 여러 특허에서 제안되었다. 가장 대표적인 방법은 현재의 White OLED 구조에 QD 변환층을 추가하는 구조가 있다. 관련 특허는 이미 여러 기업과 개인에 의해 제안되었다. 하지만 이경우 광효율의 증가는 일부 있을 수 있지만 색재현성에 대한 개선은 크지 않을 것이다. 대신 고가의 QD 재료를 추가로 사용하고 또한 추가적인 공정이 필요하기 때문에 현재까지 실제 제품에 적용된 사례는 없었다. 더구나 현재 양산중인 배면발광 구조에서는 더더욱 구현이 기술적으로 아주 어렵다.

가장 중요한 목표로 논의되는 부분은 효율을 개선하면서 동시에 소비자가 느끼는 화질측면에서 개선이 동시에 있어야 한다는 점이다. 이를 위해 또 다른 방식으로 R,G,B로 독자적인 Cavity 구조를 적용해 반치폭(FWHM)을 줄이는 방법이 개발중에 있다. 이 구조는 독일의 프라운호퍼 연구소에서 올 해 처음 소개한 구조인데 이 역시 공정의 복잡성 때문에 적용이 용이하지는 않다. 다만 큰 방향에서 FMM을 사용하지 않고 R,G,B각의 광학특성을 최대한 개선한다는 측면에서 의미가 있다.

만약 WOLED+QD_CF 구조에서R,G,B 개별 색깔의 광학적 특성을 개선하는 동시에 공정도 간단하고 또한 효율도 개선하는 기술이 가능하다면 지금의 Blue OLED + QD_CF의 Plan B로서 충분히 의미가 있다고 판단되며, 이 기술은 짧은 시기에 가시화 될 수 있을 것으로 예상된다.

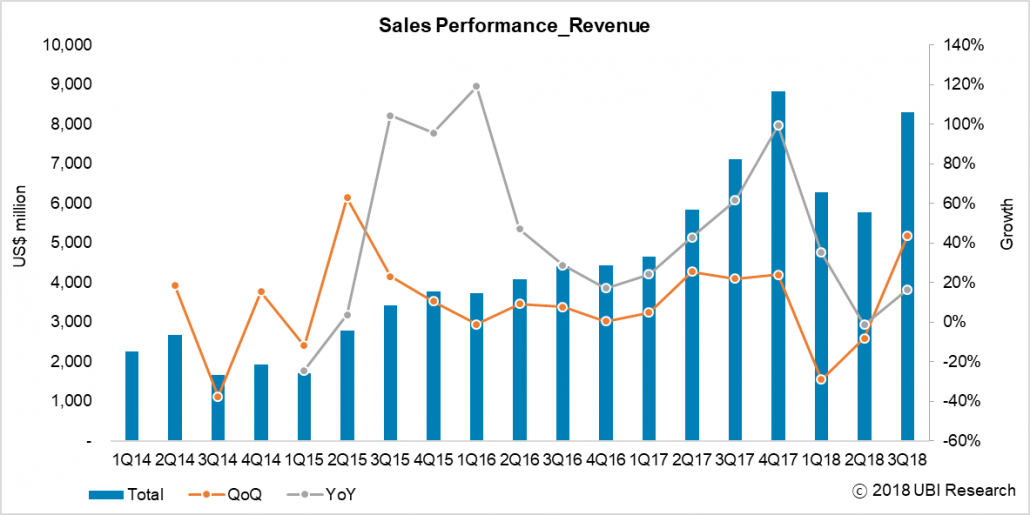

2사분기에는 삼성디스플레이의 가동율이 매우 낮아 OLED 시장 실적이 1사분기 보다 나쁘게 나타나며 업계를 긴장시켰다. 가동율 저하는 재료 업체들의 매출에 직접적인 영향을 주며, 추후 발주가 있을 것으로 예상했던 A5 공장 투자 지연으로 이어질 수 있기 때문이다. 하지만 3사분기부터는 삼성디스플레이가 갤럭시9과 iPhone XS용 플렉시블 OLED 생산을 시작함에 따라 매출이 급증하였다. 작년 3사분기 실적 71.3억달러 보다 11.7달러가 많은 83억달러로서 역대 3분기 최대 매출을 기록하였다.

<3사분기 AMOLED 마켓 트랙, 유비리서치>

3사분기 출하량은 1.3억개로서 분기 최대 매출을 달성하였다. 출하량 증대에 가장 기여한 응용제품은 역시 스마트폰용 OLED이다. 삼성디스플레이가 지난 분기 보다 15백만대 많이 판매하였다. 그 다음 출하량이 증가한 응용 분야는 워치이다. 애플 워치와 갤럭시 기어가 모두 새로운 모델이 나와 출하량이 대폭 증가하였다.

LG디스플레이는 OLED TV 시장 활황에 의해 공장을 풀가동해도 물량이 부족하다. 수율은 이미 85%에 도달해 있다. 3사분기에는 E4-1 라인의 감가상각이 끝나 4사분기부터는 흑자 전환이 기대되고 있다.

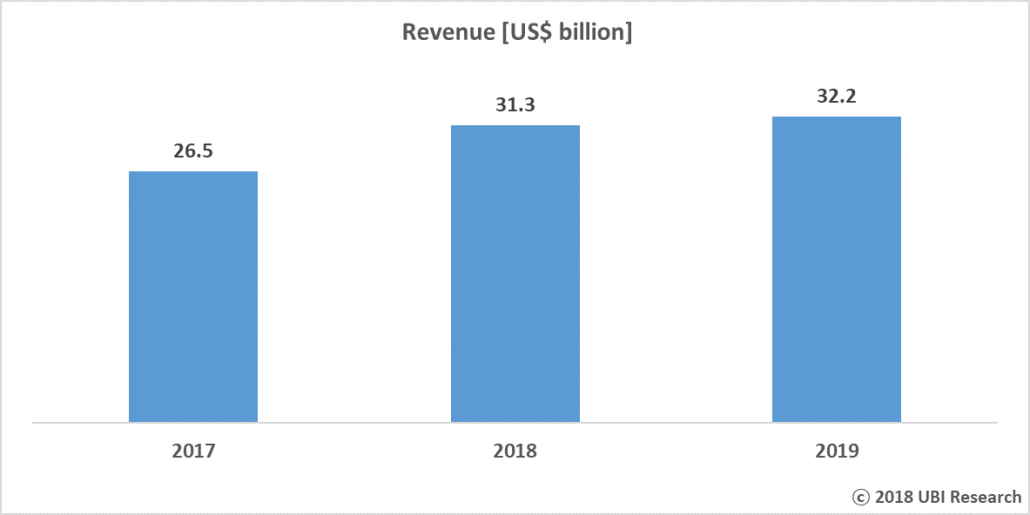

2018년이 1개월 정도 남은 현재 시점에서 2018년 매출을 예상하면 313억달러이다. 2017년 실적 265억달에 비하면 48억달러가 증가할 것으로 전망된다. 18%가 증가한 수치이다. 3사분기까지의 실적을 바탕으로 예상되는 2019년 매출은 322억달러 수준이다. 올해 대비 2.9% 정도 증가한 수치이다. 삼성전자의 주력 제품인 갤럭시S 판매가 이전과 달리 저조하며 저가형 갤럭시J 모델에는 OLED 대신 값싼 LCD가 사용되기 때문이다. 애플은 OLED를 대폭 채용하며 1,000달러 이상의 하이엔드 스마트폰용 시장에 집중하는 반면 삼성전자는 OLED를 LCD로 바꾸며 250달러 이하의 저가형 스마트폰 시장에 관심을 두고 있다.

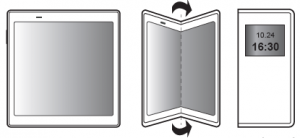

삼성 개발자 컨퍼런스에서 세계 최초의 인폴딩 폴더블 갤럭시F가 공개되었다. 폴더블 OLED의 이름은 인피니티 플렉스 디스플레이다.

갤럭시F의 주요 특징은 하드웨어와 소프트웨어 관점으로 나눌 수 있다. 우선 하드웨어면에서 7.3인치 폰이 접으면 4.6인치로 변한다. 소형 태블릿PC와 그립감이 좋은 스마트폰을 동시에 경험할 수 있다. 휴대성과 정보 확장성을 동시에 만족시킨 제품이다.

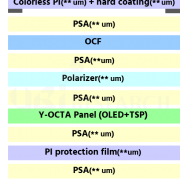

디스플레이의 해상도는 1536 x 2152이며 420ppi이며 4.2:3 비율의 제품이다. 외부 창은 840×1960이며 21:9의 비율을 가지고 있다. 접었을 때 반경이 1.5mm의 디스플레이는 기존 플렉시블 OLED 제조 기술과 소재들로서는 만들 수 없다. 접고 폈을 때 필름들이 손상을 입어 화면에 줄이가는 불량 현상이 발생한다.

<출처: 폴더블 OLED 보고서, 유비리서치>

삼성디스플레이는 접고 폈을 때의 신뢰성 확보를 위해 폴더블 OLED를 구성하는 각종 필름류의 두께와 물성 최적화 과정을 5년간 거쳤다. 기존 펄렉스블 OLED 보다 두께를 대폭 낮추었다. 이런 과정을 통해서 만들어진 폴더블 OLED는 12월부터 양산이 시작된다.

소프트웨어 관점에서 보면 펄더블 폰을 열면 외부 디스플레이에서 보던 화면이 내부 화면에서 같이 커지는 기능이 있으며, 3개의 애플리케이션을 동시에 사용할 수 있는 멀티 태스킹이 가능한 점이다.

가격은 150만원에서 200만원 정도가 될 것으로 추정되고 있다. 삼성이 이제까지 판매하던 스마트폰보다는 가격이 비싸지만 스마트폰과 태블릿 PC 두대를 한 대 가격에 구입한다고 생각하면 합리적인 가격이다. 편리 휴대성까지 고려한 부가가치까지 고려하면 매우 적절한 가격이라고 판단된다.

5G 통신 시대에 가장 필요한 스마트폰은 4K 해상도가 지원되는 7인치 이상의 디스플레이가 있는 제품이다. 휴대폰 사이즈가 7인치 이상이 되면 소형 table PC와 유사한 크기이기 때문에 휴대성이 떨어진다. 7인치 이상의 대형 디스플레이를 유지하며 휴대성을 극대화시킬 수 있는 스마트폰은 접을 수 있는 foldable OLED를 사용한 폴더블폰(foldable phone)이다.

따라서 폴더블 OLED를 생산할 수 있는 패널 업체와 폴더블폰을 팔 수 있는 세트업체, 폴더블 OLED와 폰에 들어 가는 재료와 부품을 공급할 수 있는 기업들이 2020년 이후 기업을 유지할 수 있을 것이다.

본 보고서는 foldable phone의 성공 요소 분석과 foldable OLED 개발 동향, 특히 OLED 시장에서 95% 이상의 시장을 점유하고 있는 독보적인 존재인 삼성디스플레이의 개발 방향 분석과 서플라인 체인 분석, 시장 전망을 통해 향후 foldable OLED의 미래를 예측하였다.

내년부터 도입되는 5G 통신 기술은 실시간 스트리밍 서비스 외에도 VR 등 더 높은 화질과 대용량 컨텐츠들을 더욱 더 빠른 속도로 처리할 수 있다. 통신 속도가 빨라지는 만큼 그래픽이 정밀한 고해상도와 대화면을 요구하는 컨텐츠가 출시될 전망이다.

현재의 스마트폰은 6인치까지 커지고 있으나 5G 통신시대의 4K 해상도를 담기에는 역부족이다. 7인치 이상의 디스플레이는 4K 해상도가 가능하기 때문에 5G 통신 시대의 가장 적합한 제품이 될 것이다. 폴더블 스마트폰은 7인치 이상의 디스플레이를 사용하지만 휴대성을 극대화시킨 차세대 모바일 기기로서 스마트폰과 태블릿 PC의 기능을 함께 할 수 있는 디지털 융합제품이다.

폴더블 스마트폰이 가능해진 것은 폴더블 OLED가 있기 때문이다. 삼성디스플레이를 포함하여 전세계 OLED 디스플레이 업체는 차세대 제품 시장을 선점하기 위해 막대한 개발비를 투입하여 왔고 이제 폴더블 OLED가 나오기 시작하고 있다.

OLED 스마트폰 시장을 이끌고 있는 삼성전자는 인폴딩 방식의 폴더블 폰을 세계 최초로 내년부터 출시한다. 이에 맞추어 삼성디스플레이는 1.5R가지 접을 수 있는 폴더블 OLED를 준비하고 있다. 갤럭시 S 시리즈의 판매가 정체되어 있는 삼성전자에 있어서는 폴더블 폰은 반드시 성공시켜야하는 수퍼프리미엄 제품이다.

<삼성전자 인폴딩 폴더블 OLED폰 예상 구조>

촐처: 폴더블 OLED 보고서, 유비리서치

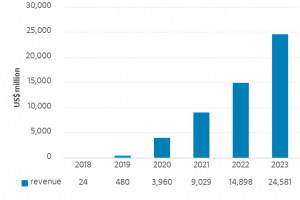

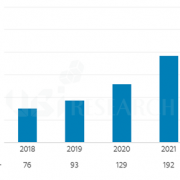

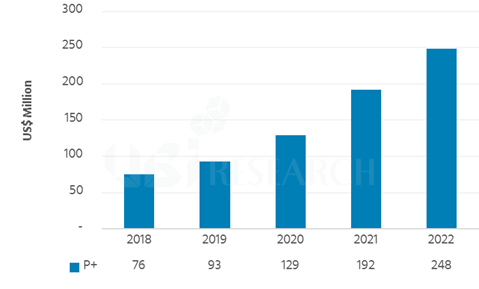

OLED 전문 리서치 기관인 유비리서치(대표 이충훈)가 폴더블 OLED 보고서를 출간했다. 이 보고서에 따르면 2019년 폴더블 OLED 시장은 4.8억달러 규모에 불과하지만 2023년에는 246억달러까지 성장할 것으로 예상하고 있다.

이충훈대표는 “폴더블 OLED 시장의 빠른 성장은 5G 통신 시대는 4K 해상도를 지원할 수 있는 7인치 이상의 스마트폰이 필수품”이 될 것으로 판단하고 있으며, OLED 패널 업체는 폴더블 OLED 생산 성공 여부에 따라 기업의 가치가 결정될 것이라고 언급했다.

<폴더블 OLED 시장 전망>

출처: 폴더블 OLED 보고서, 유비리서치

하지만 폴더블 OLED를 누구나 생산할 수 있는 제품은 아니다. 기존 플렉시블 OLED 보다 더 복잡한 모듈 구조를 가지고 있기 때문에 접었을 때 발생하는 다양한 패널 특성 변화를 극복할 수 있는 기술이 필요하다. 특히 인폴딩 폴더블 OLED는 TFT 저항 변화를 극복할 수 있는 보상 회로 기술과 화면을 접고 폇을 때 요구되는 복원력등이 대표적인 기술 난제들이다. 20만회 이상 접고 폇을 때도 디스플레이 화질과 표면에 이상이 없는 신뢰성도 요구된다.

유비리서치가 발간한 “폴더블 OLED 보고서”는 폴더블 OLED의 신뢰성을 결정하는 주요 필름의 개발 이슈와 패널 업체들의 개발 동향을 분석하여 수록하고 있다.

심천에 Gen5.5 7.5K 라인을 보유한 로욜은 디스플레이 기업 보다는 HMD(head mount display) 기업으로 알려져 있다. 올해 2사분기에 장비 설치를 완료하고 시생산에 들어간 로욜은 7.8인치 태블릿 PC를 타킷으로 패널을 개발해 왔다.

로욜은 OLED 분야에서 2가지 특이점이 있다. 폴더블 OLED 세계 최초 양산과 더불어 모바일 디스플레이에서 처음으로 oxide TFT 사용이다

모바일 기기들은 대부분 고해상도를 지향하고 있지만 로욜의 7.8인치 flexible OLED 패널은 1440×1920 FHD 보다 조금 높은 해상도로서 300ppi 정도 되는 제품이다. 폴딩 방향은 아웃폴딩이다. 비율은 4:3이다. 본격적인 판매와 생산은 12월부터 시작할 예정이다. 128G는 1,588달러이며 256G는 1759달러이다.

촐처: 로욜 홈페이지

중국 패널 업체들은 아직 패널을 안으로 접는 인폴딩 기술은 확보하지 못하고 있다. 화웨이용 폴더블 패널을 준비하고 있는 BOE와 GVO, Tianma도 아웃폴딩 패널을 주로 개발하고 있다.

폴더블 폰은 커버윈도가 플라스틱 필름을 사용하고 있기 때문에 아웃폴딩 폴더블 폰은 디스플레이가 외부 환경에 따라 손상을 입을 가능성이 매우 높다.

실제로 삼성디스플레이는 이미 수년전에 곡률반경이 5mm인 QHD 해상도 아웃폴딩 폴더블 OLED를 개발하였지만 화면에 손상을 최소화할 수 있는 인폴딩 폴더블 OLED를 12월부터 양산할 계획이다.

로욜은 oxide TFT로서 제품을 생산한적이 없기 때문에 아직 완벽한 TFT 신뢰도는 확보하지 못한상황이다. 수율이 아직 매우 낮기 때문에 판매가 시작되어도 연간 공급할 수 있는 물량은 한정적이 될 것으로 예상된다.

OLED는 rigid 타입에서 flexible 타입으로 진화하였고, 이제는 foldable OLED로 진화하기 위한 마지막 단계에 도달해 있다. 4G의 스마트폰 시장이 5G로 변경되면 더 빠른 통신 속도를 바탕으로 더 복잡하고 정교한 소프트웨어들이 출현할 전망이다. 스마트폰에서 5G 시대를 맞이하기 위해서는 8인치 정도의 디스플레이가 필수적이다. 이번 세미나에서는 foldable OLED 시장 전망과 더불어 foldable OLED 핵심 제조 기술인 최신 encapsulation과 기술과 평가 기술, 제조 경비를 줄일 수 있는 새로운 레이저 리프트오프 기술이 소개된다.

프리미엄 TV 시장은 이제 WRGB OLED로 대체되고 있다. 삼성디스플레이는 WRGB OLED를 능가할 수 있는 새로운 개념의 QD-OLED 사업화에 박차를 가하고 있다. 2021년부터 양산이 기대되는 QD-OLED의 핵심 재료인 청색 발광 재료와 QD 재료의 개발 상황을 파악하여 OLED TV 시장을 전망하고자 한다.

증착 기술로 만들어지는 WRGB OLED와 QD-OLED 기술에 대응하기 위해 일본과 중국 기업들은 중가의 OLED TV를 생산할 수 있는 soluble process (inkjet) OLED에 집중하고 있다. 이번 세미나에서는 soluble OLED 발광재료 개발 수준을 파악하여 언제부터 패널 양산이 가능할 것인지를 점검해보고자 한다.

지난 10월 24일부터 26일까지 서울 COEX에서 열린 IMID 2018 전시회에서 Samsung Display는 ‘5G 시대에 최적화된 OLED’를 주제로 다양한 OLED 제품을 선보였다.

먼저, Samsung Display는 ‘realistic multimedia’를 주제로 full screen OLED의 변천 과정과 HDR & true black을 소개하며 OLED의 장점을 강조하였다. 현재 스마트폰 시장은 OLED를 적용한 full screen 스마트폰이 주도하고 있으며, OLED는 LCD 대비 완벽한 블랙 표현이 가능하여 더욱 더 선명한 화질을 보여준다.

이어서, 화면을 터치하면 손으로 물리적 진동을 느낄 수 있어 실감 나게 콘텐츠를 즐길 수 있는 HoD(Haptic on Display) 기술과 디스플레이 내장형 지문 센서기술(FoD:Fingerprint on Display), 사운드 내장 디스플레이(SoD:Sound on Display)등 차세대 터치 기술과 full screen 기술을 선보였다.

뿐만 아니라, 부스 앞쪽에는 플라스틱 커버 윈도우를 부착한 flexible OLED의 내구성을 직접 체험해볼 수 있는 공간이 마련되어 관람객들이 직접 망치로 패널을 두드려보거나 볼을 떨어뜨리는 테스트를 진행하며 flexible OLED만이 보여줄 수 있는 다양한 장점들을 보여주었다.

이 밖에, 1200ppi 초고해상도를 구현한 VR용 OLED와 차량용 롤러블 디스플레이(CID), 5.9형 투명HUD 등이 전시되어 앞으로의 디스플레이 기술 발전에 대한 기대감을 불러일으켰다.

LG Display는 올해 초 미국 라스베이거스 CES 2018에서 공개한 8K OLED TV를 국내에서 처음으로 공개하며 관람객들의 이목을 사로잡았다. 이 제품은 현존하는 OLED TV 중 가장 큰 크기로써, UHD 해상도보다 4배 더 선명한 화질을 구현한다.

또한, LG Display는 사운드 시스템을 패널에 내재화해 화면에서 사운드가 직접 나오게 만든 65인치 CSO(Crystal Sound OLED)와 벽과 완전히 밀착시켜 거실의 인테리어 효과를 높일 수 있는 77인치 UHD 월페이퍼 OLED 제품을 선보이며 OLED의 다양한 활용 가능성을 제시했다.

이 밖에 자동차 부문에서 full dashboard 구현하기 위해 flexible OLED를 활용한 12.3인치 Cluster를 전시하였으며, 조명 부문에서 디자인 요소를 가미한 다수의 OLED 조명과 OLED를 활용한 자동차용 후미등도 선보였다.

10월 24일부터 26일까지 서울 COEX에서 개최된 IMID 2018에서 LG Display는 OLED의 다양한 활용 방안을 제시하며 큰 관심을 이끌었다.

LG Display는 올해 초 미국 라스베이거스 CES 2018에서 공개한 8K OLED TV를 국내에서 처음으로 공개하며 관람객들의 이목을 사로잡았다. 이 제품은 현존하는 OLED TV 중 가장 큰 크기로써, UHD 해상도보다 4배 더 선명한 화질을 구현한다.

또한, LG Display는 사운드 시스템을 패널에 내재화해 화면에서 사운드가 직접 나오게 만든 65인치 CSO(Crystal Sound OLED)와 벽과 완전히 밀착시켜 거실의 인테리어 효과를 높일 수 있는 77인치 UHD 월페이퍼 OLED 제품을 선보이며 OLED의 다양한 활용 가능성을 제시했다.

이 밖에 자동차 부문에서 full dashboard 구현하기 위해 flexible OLED를 활용한 12.3인치 Cluster를 전시하였으며, 조명 부문에서 디자인 요소를 가미한 다수의 OLED 조명과 OLED를 활용한 자동차용 후미등도 선보였다.

한편, LG Display의 한상범 부회장은 “이번 IMID 2018 전시회에서 차세대 디스플레이인 OLED 기술력을 선보여 시장과 고객에게 차별화된 가치를 제공하고, 이를 통해 디스플레이 시장을 지속적으로 선도해 나갈 것”이라고 언급했다.

2018년 10월 24일부터 서울 코엑스에서 열리고 있는 IMID2018에서 OLED 증착장비 개발 벤처회사인 OLEDON이 ‘경쟁 국가들과의 초격차를 유지하기 위한’ OLED 제조 기술인 면소스 증착기술을 공개하여 이목을 집중시키고 있다.

OLEDON의 황창훈대표는 “한국이 현재의 OLED 생산국 1위를 앞으로도 유지하려면 창의적인 증착 기술개발 도전에 적극 투자하여야 한다”며, “미래의 중소형 및 대형 OLED 제조는 모두 면소스 증착기술이 사용될 것”이라 전망했다.

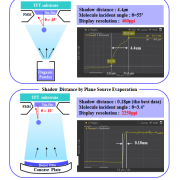

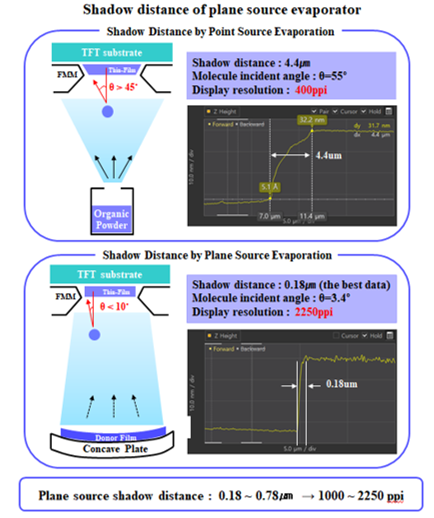

OLEDON이 세계최초로 개발 중인 곡면소스 FMM 증착기술은 2250ppi의 AMOLED 제조가 가능한 초고해상도 OLED 증착기술로서, 미세 패턴의 섀도우거리가 0.18um까지 가능하여 11K급 초고해상도의 AMOLED 패턴공정이 가능하다.

기존의 FMM 증착 패턴(좌)와 면소스 FMM 증착 패턴(우), Source: OLEDON

황 대표는 이러한 공정을 800ppi 섀도우 마스크로 확인한 결과, 면소스로 증착한 패턴의 발광면적이 기존의 증착 방법보다 1.7배 향상되었다고 발표하였다.

한편, OLEDON은 면소스 FMM증착기술의 원천특허를 보유하고 있으며 최근에는 대면적 OLED TV 제조용 수직형 면소스증착 특허를 출원하기도 하였다.

OLED TV 제조용 수직형 면소스 증착, Source: OLEDON

2018년 10월 24일 진행한 3분기 컨퍼런스 콜에서 LG 디스플레이는 대형 OLED의 흑자전환을 발표하였다. 최근 OLED TV의 판매 호조에 힘입어 유일한 TV 패널 공급사인 LG 디스플레이는 지속적인 매출 상승을 보여왔으나 감가상각 등으로 적자를 기록하다 올 3분기 흑자 전환하였다. 이는 LG디스플레이를 비롯한 디스플레이 산업에 긍정적인 시그널로 인식되고 있으며 앞으로 계속적인 추가투자를 진행하는 LG디스플레이에게 우호적인 분위기를 실어줄 것으로 기대하고 있다.

3분기는 LCD도 전반적인 패널 판가 상승 등 우호적인 상황 계속되어 전분기 대비 매출은 9% 증가한 6조1천억, 영업이익 1401억을 기록했다. 하지만 여전히 디스플레이 산업의 사이클이 변화하고 있다는 것을 언급하며 LG디스플레이는 지속적으로 보수적인 시각에서 향후 전략을 이어 나갈 것임을 강조했으며 고부가가치 제품과 OLED 수익성 개선에 집중할 것을 언급했다.

3분기 출하 면적은 전분기 대비 5% 증가했으나, 소형 패널의 출하가 미뤄지면서 면적당 판가에는 긍정적인 영향을 미치지 못한 것으로 나타났으며 중장기 투자 진행과 LCD 팹의 OLED 전환계획 등으로 순차입금은 소폭 상승하고 현금흐름은 감소하였다.

향후 패널 판가는 현제의 상승세는 유지하기 어려울 것이며 사이즈별로 상이하게 움직일 것으로 예상하였다. 또한 최근 산업의 이슈 중 하나였던 iPhone 패널 공급과 관련하여 “모바일 제품 수급 이슈가 해결되어 출하가 정상화될 것”으로 언급, 2018년 말에는 iPhone 패널 공급이 이루어 질 것을 짐작해 볼 수 있다.

LCD팹의 OLED 전환과 관련해서는 아직 규모와 시기 확인에 대해 언급하지 않았으나 현재 최근 전시/컨퍼런스 등을 통한 공급 계획 규모 등을 볼 때 연내 순차적인 규모와 시기 확정을 통해 계획 수립을 할 것으로 기대 된다. 또한 E6-1와 E6-2팹의 감가상각 언급을 통해 2019년 E6-2의 양산 목표를 밝혔다.

과거 디스플레이 산업에서 최강국이었던 일본은 브라운관과 PDP, LCD 시대를 거치며 점차 쇠락하여 OLED 산업에서는 중국에 이어 3위의 생산국으로 전락했다.

현재 AMOLED를 생산하는 일본 기업으로서는 소니와 JOLED가 있다. 양사 모두 특수 모니터용 OLED를 월 500~1,000대 수준으로 생산하고 있다. JDI는 flexile OLED를 개발하고 있지만 아직 사업화를 하지 못하고 있다.

제품 생산에 소극적이던 현 일본 제조 환경에서 샤프가 과감히 스마트폰용 OLED 시장에 도전장을 던졌다. 사카이 공장 4.5세대 시생산 장비에서 flexible OLED 생산을 시작한다. 소프트뱅크용 AQUOS zero 모델에 채택된다.

CEATEC2018의 샤프부스에서 이 제품이 전시되었다. QHD+ 6.2인치 듀얼 엣지 타입이다. 관계자는 아직 판매는 시작하지 않았다고 언급하였다.

샤프는 이 이외에 개발중인 flexible OLED 2종을 같이 전시하였다.

일본전자전 CEATEC2018이 지난주 마쿠하리메세에서 개최되었다. IoT와 첨단 센스 기술을 중심으로 다양한 일본 기업들이 제품을 전시하였다. 일본의 전자 산업이 대형 하드웨어에서 점점 소형 첨단 부품 산업과 소프트웨어 산업으로 변화하고 있는 것이 감지되었다.

이번 전시회에는 자율주행이 가능한 스마트카의 핵심 기술도 소개되었다. 쿄세라는 자동차의 안전을 강화하기 위해 첨단 센싱 기술과 화상 처리 기술로서 사각 지대에서 발생할 수 있는 각종 사고를 미리 예상하고 방지할 수 있는 cockpit 기술을 소개하였다.

또한 자동차용 디스플레이 사업에서는 클러스터와 CID, 룸미러 디스플레이, 사이드뷰 디스플레이가 탑재된 첨단 컨셉카를 전시하였다.

쿄세라 관계자에 의하면 이 컨셉카의 디스플레이는 모두 LCD를 사용하고 있지만 외부 환경을 보여주는 룸미러 디스플레이와 사이드뷰 디스플레이는 LCD는 한계가 있어 OLED로 전환되어야 할 것이라고 언급하였다.

고속주행중에 빠르게 바뀌는 외부를 보여주는 룸미러 디스플레이와 사이드뷰 디스플레이에 LCD가 사용되면 응답속도가 늦어 주위 차들의 위치가 실제 위치 보다 뒤에 있는 것으로 표현할 수 있어 운전자가 차선을 변경할 때 사고가 발생할 수 있다. 특히 야간에는 명암비가 낮은 LCD는 외부 사물을 정확히 나타낼 수 없음을 인정하였다.

OLED는 고속 응답과 높은 명암비를 가지고 있어 미래 자동차의 룸미러와 사이드뷰 미러 시장을완전히 장악하게 될 것으로 예상된다.

모니터와 가상현실 기기에 이어 자동차에 사이드미러용 OLED의 적용 등, OLED가 스마트폰과 TV에서 벗어나 점점 그 영역을 확대해 나가고 있다. 다양한 환경에서 새로운 OLED application이 증가할수록 사용자들을 만족시키기 위한 기술 개발도 필수적이다.

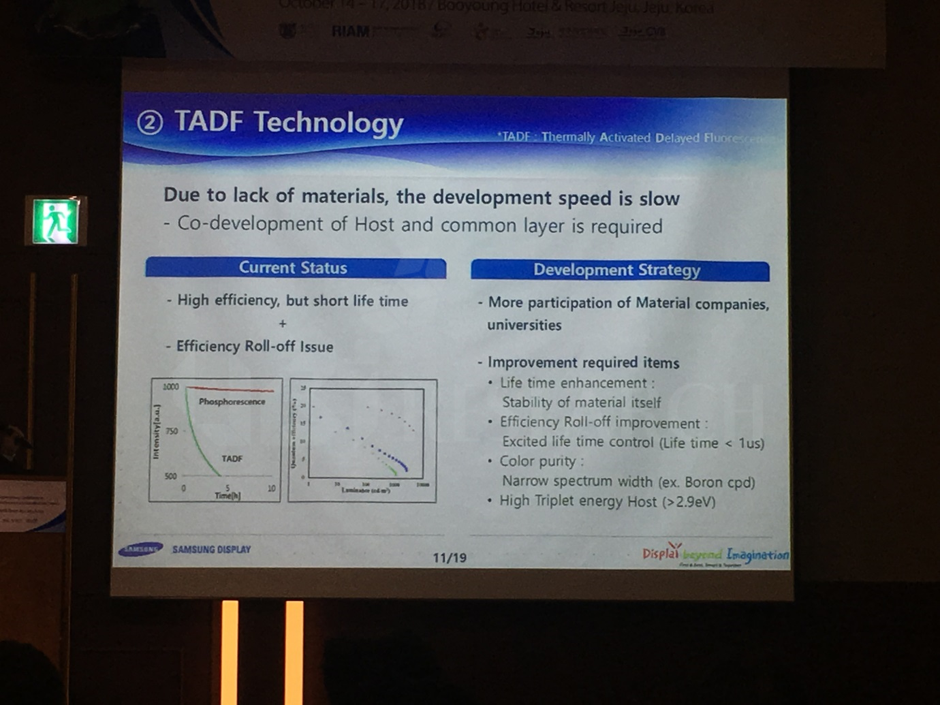

제주국제컨벤션센터에서 10월 15일부터 진행되고 있는 ICEL 2018에서 다수의 연사자들은 OLED 시장이 점점 더 성장함에 따라 OLED의 성능을 개선하기 위한 재료 개발이 필수적이라 역설하였으며 그 대안이 될 재료로 TADF(Thermally Activated Delayed Fluorescence)를 언급하였다.

먼저, Samsung Display의 황석환 수석연구원은 OLED 패널과 재료 시장의 지속적인 성장을 언급하며 새로운 증착 공정용 발광 재료 중 하나로 TADF가 좋은 대안이 될 수 있음을 밝혔다.

황 수석연구원은 형광 청색의 효율은 현재 거의 포화 된 상태이기 때문에 TADF를 적용함으로써 이론적으로 100%의 발광효율을 얻을 수 있으며 값비싼 희토류 금속을 사용하지 않아도 된다는 점등을 장점으로 언급하였다. 이어서 실제 OLED에 적용되기 위해서는 재료의 안정성 향상과 Boron 재료 등을 활용한 색 순도 개선, 높은 triplet 에너지를 갖는 호스트 개발 등이 선행과제라 설명하였다.

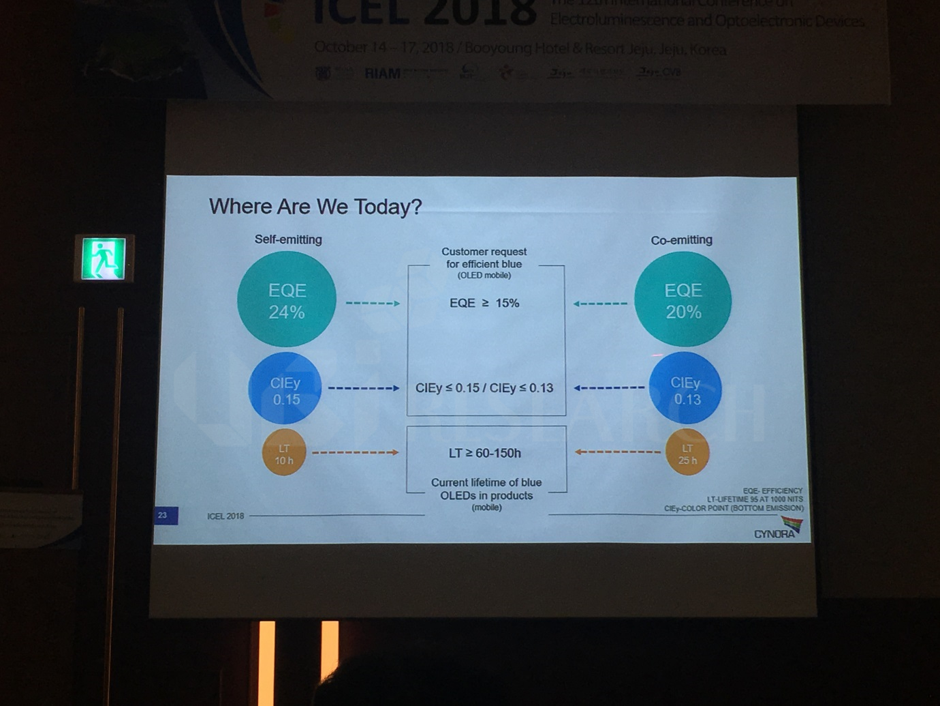

다음으로 TADF를 개발 하고 있는 대표적인 기업인 CYNORA는 현재까지 개발 된 진한 청색 TADF의 성능을 공개하였다.

CYNORA는 진한 청색 TADF의 발광 효율과 색 순도가 업체들이 원하는 수준에 도달하였다며 현재 최종 목표로 수명 향상을 위한 기술 개발을 진행 중이다 라고 언급했다. 또한, 이러한 노하우를 바탕으로 녹색과 적색 TADF를 빠르게 개발 완료할 것이며 현재 녹색 TADF는 몇몇 고객사들에게 샘플로 납품했음을 밝혔다.

이 밖에, Merck도 TADF와 관련 된 포스터 발표를 진행하며 TADF가 형광 청색을 대체 할 수 있는 가장 강력한 발광재료임을 확인시켜 주었다. 청색 TADF가 OLED 시장에 빠르게 진입하여 OLED 성능을 한층 더 업그레이드 시킬 수 있을지 OLED 관련 업체들과 연구기관들의 이목이 집중되고 있다.

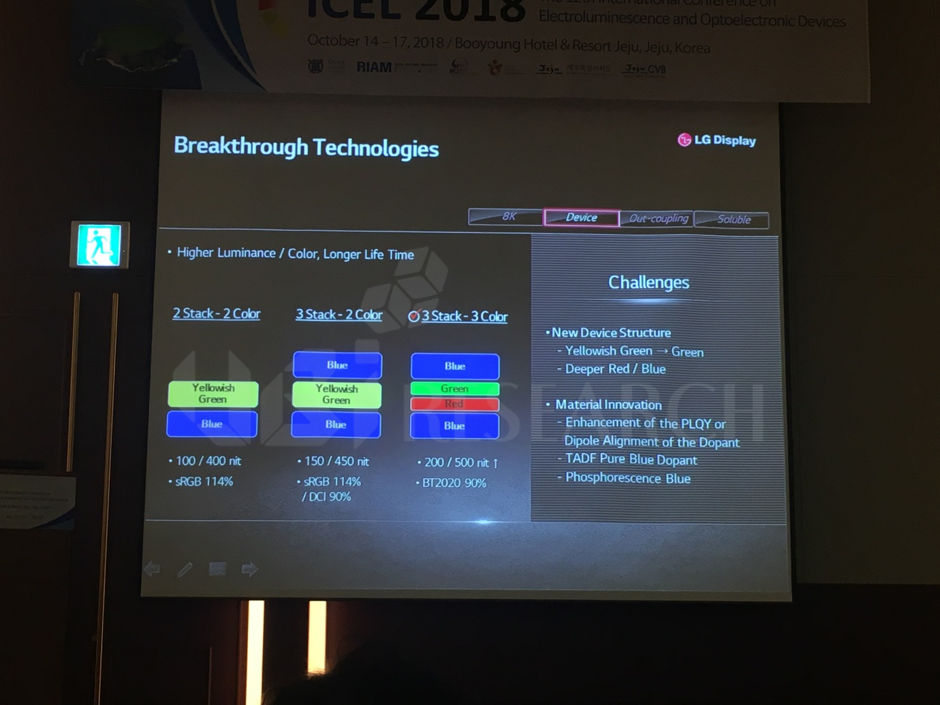

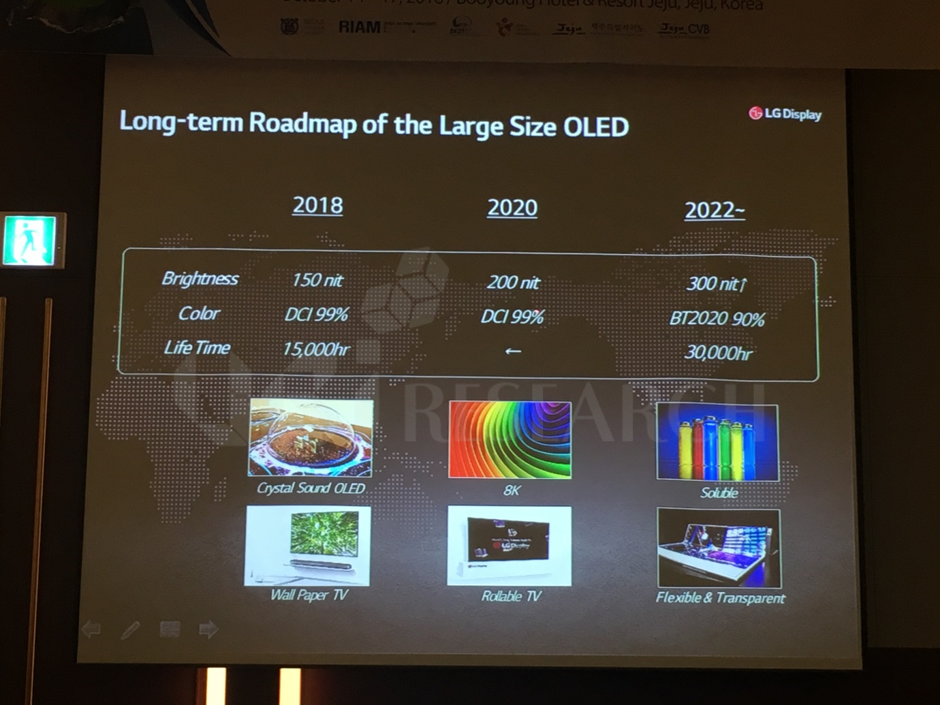

10월 15일부터 제주국제컨벤션센터에서 열리고 있는 ICEL 2018에서 LG Display의 윤수영 연구소장은 OLED TV의 성능 향상과 가격 하락을 위한 도전 과제를 발표하였다.

윤 연구소장은 “2016년 OLED TV 미래 시장 전망과 비교하여 2018년 OLED TV 미래 시장 전망은 더욱 더 긍정적으로 변화하였다”며 “2013년 LG Electronics 단 하나뿐이었던 OLED TV set 업체는 2016년 10개, 2018년 15개로 꾸준히 증가하는 등 다수의 TV set 업체가 OLED를 선택하고 있다”고 밝혔다.

이어서 OLED TV가 많은 발전을 이루었지만 더욱 더 발전해야 한다고 밝히며 도전 과제로 휘도와 색재현율 개선, 8K 해상도 개발, 수명 향상 등의 성능 개선과 가격 하락을 강조하였다.

윤 연구소장은 8K OLED TV를 개발하기 위해 재료 개발과 함께 driver IC와 컨트롤러 등의 부품 개발도 중요과제라고 설명했다. 이어서, 휘도와 색재현율, 수명을 향상하기 위해서는 RGB 발광재료 개선을 TADF나 인광 청색도 좋은 대안이 될 것임을 언급하였으며 out-coupling 향상도 중요하다고 강조하였다.

또한, LCD TV 가격에 대응하기 위한 기술로 solution process OLED를 언급하며 잉크젯 장비와 공정, soluble 재료의 개발도 필요하다고 밝혔다. 이를 위해서는 잉크젯 장비 개발과 대량 생산을 위한 공정 시간 단축도 필요하지만, soluble 재료의 성능과 신뢰성이 무엇보다도 중요할 것이라 언급했다.

또한, LCD TV 가격에 대응하기 위한 기술로 solution process OLED를 언급하며 잉크젯 장비와 공정, soluble 재료의 개발도 필요하다고 밝혔다. 이를 위해서는 잉크젯 장비 개발과 대량 생산을 위한 공정 시간 단축도 필요하지만, soluble 재료의 성능과 신뢰성이 무엇보다도 중요할 것이라 언급했다.

마지막으로, 2020년까지 휘도 향상과 함께 8K OLED TV와 rollable OLED TV를 중점적으로 개발 할 것이며, 2022년 이후에는 300 nit 이상의 휘도와 BT.2020을 만족하는 색재현율, 3만 시간 이상의 수명을 가진 OLED TV 개발을 진행할 것이라 밝혔다.

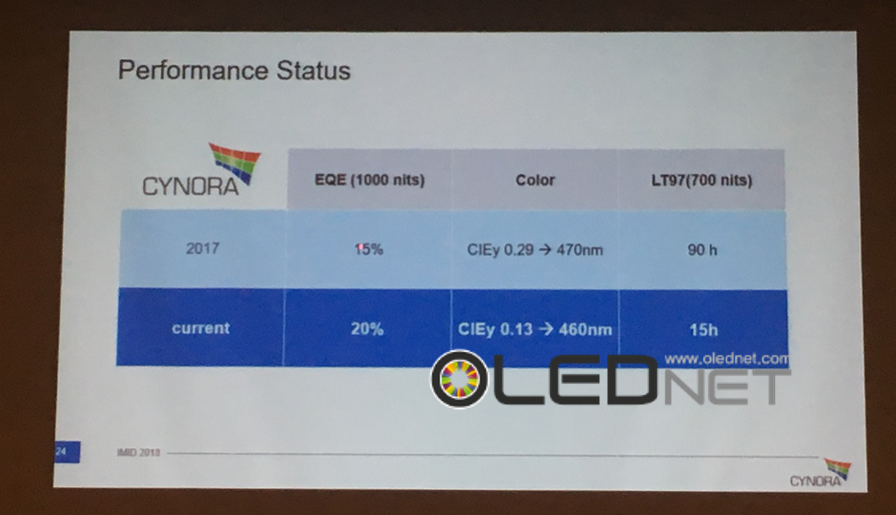

TADF 개발 업체인 CYNORA는 LG Display와 공동 개발 계약을 연장했다고 발표했다. 두 회사는 2 년 동안 진한 청색(deep blue) TADF를 공동 개발한 것으로 알려졌으며, 이번 계약 연장을 통해 TADF 상용화를 위한 협력을 지속한다.

CYNORA에서 현재 개발 중인 최신 진한 청색 TADF 성능은 지난 8월 IMID 2018에서 공개된 바 있다. 당시 언급된 성능 중 CIEy는 0.13, 1000 nits 기준 EQE는 20%, 700 nits에서 LT97은 15시간이다.

또한, CYNORA는 조명 애플리케이션용 연한 청색(sky blue) TADF와 디스플레이용 녹색 TADF도 개발할 것이라고 언급했다.

CYNORA의 Gildas Sorin CEO는 “현재 CYNORA는 OLED TV용 진한 청색 TADF 개발에 초점을 맞추고있다”라고 말하면서 “그 동안 진행 청색 TADF을 개발하며 축적 된 노하우를 통해 조명 애플리케이션용 연한 청색 TADF와 OLED 디스플레이용 녹색 TADF을 개발 할 것”이라고 밝혔다.

커넥티드 카의 디스플레이는 다양한 정보로서 편의성을 제공하기 위해 점점 커지고 있다. 일반적인 자동차에 사용되는 디스플레이는 클러스터와 CID(center information display), RSE(rear seat entertainment), RMD(room mirror display)가 있다. 커텍티드 카에는 센터페시아의 각종 버튼이 디스플레이가 되고 사이드미러 대신 카메라를 사용하여 디스플레이를 문에 부착하게 된다. 내년부터 출시되는 아우디의 전기자동차 e-tron에는 사이드뷰 디스플레이를 사용한다.

유비리서치 이충훈대표에 의하면 자동차 업체들이 OLED를 디스플레이로 사용하기 위해 적극적으로 OLED 업체들에게 구애를 하고 있는 이유는 디자인과 시인성, 두께 등의 다양한 부분에서 OLED만이 해결해 줄 수 있기 때문이라고 언급했다.

사이드뷰 카메라는 도어에 부착되기 때문에 운전자의 시선에서는 시야각이 매우 좋아야 한다. 특히 야간주행에서는 블랙이 정확하게 디스플레이에 표현되어야지 사물의 형태가 선명해진다. 또한 빠른 속도로 주행중인 자동차의 미러에는 속도에 따라 화면이 빠르게 변하기 때문에 응답속도가 빠른 OLED가 반드시 사용되어야 한다. 기온이 낮은 겨울에는 응답속도가 늦은 LCD는 사용이 불가능하다.

또한 운전자 편의성을 극대화시켜주는 콕핏(cockpit) 디스플레이를 대쉬보드에 장착하기 위해서는 플렉시블 OLED가 반드시 사용되어야 한다.

<벤츠 F015 cockpit display와 아우디 e-tron side view display>

아우디는 올해 처음으로 AMOLED를 뒷자석 리모트용 디스플레이로 사용하여 OLED의 새로운 응용 시장을 개척했다. 아우디는 모두 삼성디스플레이가 만드는 rigid OLED를 사용한다.

이에 비해 TV용 OLED 시장에서 최강자인 LG디스플레이는 RGB OLED를 2층 적층한 플렉시블 OLED로서 클러스터용 디스플레이와 CID용 시장을 노리고 있다. 자동차용 디스플레이 공급업체로서 점유율 2위인 Visteon은 LG디스플레이의 pOLED로서 클러스터 시장을 준비하고 있다. 12.3인치 pOLED는 LTPS 기판으로 만들어지며 스마트폰용 OLED 보다 OLED 공정이 복잡하기 때문에 모듈을 포함한 패널 가격은 55인치 WRGB OLED와 대등한 가격이 될 전망이어서 수량이 적어도 초고가의 프리미엄 시장을 창출할 수 있다.

<Visteon, 12.3인치 pOLED>

유비리서치가 발간한 “자동차용 OLED 디스플레이 보고서”에 의하면 삼성디스플레이와 LG디스플레이가 이끄는 자동차용 OLED 디스플레이 시장은 2023년에는 5.4억달러 시장으로 성장할 전망이다.

Samsung Display는 글로벌 자동차 기업 Audi가 최근 선보인 전기 스포츠 유틸리티 차량(SUV) e-Tron에 7인치 OLED 디스플레이를 공급한다고 3일 밝혔다.

e-Tron은 Audi가 처음으로 양산·판매하는 순수 전기차로 ‘버추얼 익스테리어 미러(virtual exterior mirrors)’ 옵션을 제공해 출시 전부터 큰 화제를 모았다.

Audi의 버추얼 익스테리어 미러는 기존의 사이드 미러 대신에 작은 사이드 뷰 카메라를 장착했다. 운전자는 카메라로 촬영한 영상을 차량 내 A필러(전면유리 옆 기둥)와 도어 사이에 설치돼 있는 OLED 디스플레이를 통해 실시간으로 확인할 수 있다.

<Audi e-Tron에 적용 된 버추얼 익스테리어 미러, Source: news.samsungdisplay.com>

Samsung Display가 공급하는 OLED 디스플레이는 차량 대시보드 좌우에 각각 한 대씩 장착돼 카메라와 함께 기존의 사이드 미러 기능을 대신하며, 터치 센서가 내장돼 있어 스마트폰을 조작하듯이 터치로 화면을 확대하거나 축소할 수 있다.

Audi는 ‘버추얼 익스테리어 미러’는 일반적인 사이드미러와 비교해, 사각지대 없이 보다 넓은 시야를 제공한다고 밝혔다. 흐린 날이나 어두운 곳에서도 보다 원활하게 시야를 확보할 수 있게 해주고 고속도로 주행, 회전, 주차 등 각각의 운전상황에 적합한 ‘뷰 모드’를 제공해, 보다 편리하고 안전하게 운전할 수 있도록 도와준다. 또한 차량 외부로 툭 튀어나온 사이드 미러를 없앰으로써 공기저항 및 풍절음을 감소시킬 뿐만 아니라, 차체 폭을 5.9인치 가량 줄인, 슬림하면서도 아름다운 디자인이 가능하다.

특히 버추얼 익스테리어 미러에 적용된 Samsung Display의 OLED는 소비전력이 적고, 얇고 가벼운 디자인적 특성으로 운전자들에게 최적의 시각적 솔루션을 제공한다. 뿐만 아니라 뛰어난 색재현력과 완벽한 블랙 컬러 표현력, 빠른 응답속도로 저온의 환경에서도 화면이 끌리는 현상 없이 자연스럽고 선명한 영상을 보여준다.

백지호 Samsung Display 전무는 “Samsung Display의 OLED가 Audi의 버추얼 익스테리어 미러에 탑재된 것은 OLED가 차량용 첨단 시스템에 최적화된 제품임을 입증하는 매우 고무적인 일”이라며 “고화질, 디자인 가용성, 저소비전력 등 OLED만의 차별화된 특장점을 활용해 자동차용 디스플레이 시장도 적극적으로 개척해나갈 것”이라고 밝혔다.

중소형 OLED용과 대면적 OLED용 면소스 증착 기술을 개발하고 있는 OLEDON의 황창훈 대표는 최근 77인치 이상 초대형 OLED TV의 제조가 가능한 수직형 면소스 증착 기술을 개발하고 있다고 밝혔다. 황 대표는 수직 면소스 증착 기술을 사용 시, 12세대(3300 x 4000 mm)급 대형 기판의 처짐 문제 없이 77인치 이상의 OLED TV 대량 생산이 가능하다고 관련 기술을 소개하였다.

황 대표 설명에 따르면, 기존의 인라인형 증착기로 75인치 이상의 TV의 생산 시 기판의 처짐이 심하고 다수의 리니어 소스 제어가 어려워 생산 수율이 매우 낮을 수 있다. 황 대표는 이를 해결하기 위해 새로운 개념의 12세대용 대면적 클러스터형 증착 기술이 필요하다고 밝히며, 수직 면소스 증착 기술이 적절한 대안이 될 것임을 언급하였다.

한편, OLEDON은 면소스 증착 기술의 원천특허를 보유하고 있으며, 고해상도 AMOLED 제조용 곡면소스 FMM 증착과 대면적 OLED TV 제조용 수직 면소스 증착 기술과 관련 된 특허를 출원하였다.

2분기 실적 갱신을 하며 OLED TV 덕을 톡톡히 보고 있는 LG전자에 비해 삼성전자는 최근 프리미엄 TV 시장에서 고군 분투하고 있다. 마케팅을 앞세워 QD-LCD로 프리미엄 TV 시장에서 대응해 오다 점차 그 힘을 잃고 있는 것으로 보인다. 2017년부터 IFA, CES등 가전 전시회에서 QLED TV 개발 발표, 프라이빗 부스 전시 등 새로운 시도를 하고 있지만 개발이 더딘 와중 삼성전자의 Micro LED 상용화의 공식 발표로 향후 프리미엄 TV 시장의 구도에 대한 관심이 뜨겁다.

2018 CES와 2018 IFA에서 대중에 공개한 삼성전자의 Micro LED (Mini LED) TV “The Wall”은 상당 수준 발전한 Micro LED 기술을 보여주고 있으며 이에 따라 대만의 관련 업체 들의 주가도 높아지고 있다. 이런 흐름에 대응하는 차원에서 2018 IFA에서 LG전자도 173인치의 Micro LED TV를 전시한 것으로 보인다.

넓은 시야각, 완벽한 블랙의 표현, 빠른 응답 속도 등이 OLED TV의 장점으로 언급되며 프리미엄 TV 시장을 점유해 가고 있다. 산업에서는 아직까지는 Micro 수준이라고 할 수 없는 픽셀을 더 줄이고 가격을 경쟁 가능한 수준으로 하락, 전사에서 오는 신뢰성을 극복하는 등의 한계점 들을 극복한다면 150인치 정도의 초대형 디스플레이 시장을 형성할 수 있을 것으로 예상하고 있다. 이론적으로 Micro LED는 OLED 와 같이 RGB가 스스로 빛을 내는 자발광 디스플레이이며, 작은 부피와 높은 명암비, 사이즈를 줄임으로서 단위 면적당 더 많은 화소수를 넣을 수 있어 고해상도 구현에 유리하다. 또한, 초소형 픽셀사이즈로 구부러지는 디스플레이 구현도 가능한 것으로 알려져 있다.

하지만 여전히 가정용 TV로 생산하기에 Micro LED 는 제조 비용의 문제와 발열등 극복해야될 한계점을 가지고 있어 본격적인 상용화 까지는 시일이 꽤 걸릴것으로 내다 보고 있다. 각종 전시회에서 지속적으로 발전된 제품을 공개하고 있는 만큼 산업의 기대도 큰 것으로 보인다. 또한 동시에 OLED TV 또한, CSO(Crystal Sound OLED) 등 다양한 각도로 진화하고 있어 앞으로의 프리미엄 TV 시장이 기대된다.

(사진: 삼성전자, The wall, 2018 IFA, 출처: 유비리서치)

Apple이 현지시간으로 9월 12일 미국 캘리포니아주에 위치한 애플 파크 스티브 잡스 극장에서 이전보다 더 큰 화면에 헬스케어 기능을 강화한 Apple Watch Series 4를 발표했다.

<Apple Watch Series 4, Source: apple.com>

Apple은 이번 발표에서 Apple watch Series 4에 LTPO라는 새로운 기술을 도입해 전력 효율을 향상시켰다고 밝히며 이목을 끌었다.

LTPO는 low temperature polycrystalline oxide의 약자로써, 전하 이동도가 우수한 poly-Si과 저전력 구동이 용이한 IGZO의 장점만을 활용한 TFT의 일종이다. LTPO TFT는 누설전류가 적고 on/off 특성이 좋기 때문에 소비 전력이 낮고 배터리의 지속 시간은 늘어난다.

<Apple의 LTPO TFT 특허>

또한, Apple은 Apple Watch 4의 본체 규격을 40mm와 44mm로 키우고 bezel을 좁혀 이전 모델들에 비해 display area를 35%와 32%로 늘렸으며, 화면 해상도도 44mm 모델은 368×448 픽셀, 40mm 모델은 324×394 픽셀로 증가시켰다고 설명했다. Apple Watch4의 디스플레이는 LG디스플레이에서 제작한 plastic OLED이며 최대 밝기는 1,000 nit이다.

Apple Watch Series 4의 출시 가격은 GPS 모델이 399달러부터이며 셀룰러 모델이 499달러부터다. 예약 주문은 9월 14일부터 진행되고 제품 출시는 21일부터다.

2018년 8월 30일부터 9월 5일까지 베를린에서 유럽 최대 가전 전시회인 IFA2018이 개최되었다. IFA2018에서 전시된 TV는 OLED TV를 비롯하여 LCD TV와 micro LED TV, laser TV 4종류가 있었으며, 전시 참가 업체는 삼성전자, LG전자, 소니, 파나소닉, 샤프, 도시바, TCL, 하이센스, 창홍, 필립스, 베스텔, 메츠, 그룬딕, 레베 등이 있었다.

유비리서치는 IFA2018에 전시된 전세계 주요 TV 업체들의 전시 제품을 조사하여 OLED TV를 중심으로 “전시 동향 분석 보고서”를 출간하였다.

본 보고서에 따르면 IFA2018에서 TV 전시 주요 특징은 75인치 LCD TV 부상과 8K TV, micro LEDTV 세가지로 요약되었다.

첫째 LCD TV는 75인치가 중점적으로 부각된 이유는 65인치 LCD TV 가격 하락으로 2,000달러 이상의 프리미엄 TV시장에서 수익을 내기 위해서는 75인치 이상의 LCD TV가 필요해졌기 때문이다. 삼성전자 부스에서는 75인치가 65인치에 비해 차이가 별로 나지 않음을 홍보하였다.

두번째 특징은 8K TV이다. 이전 전시회까지는 샤프만이 8K LCD TV를 전시하여 왔으나 IFA2018에서 삼성전자가 8K LCD TV (QLED TV)를 처음으로 전시하며 많은 관람객을 끌었다. 88인치 8K OLED TV도 처음으로 LG전자 전시장에서 공개되었다. 완벽한 블랙과 OLED만의 생동감 있는 화면에 8K 고해상도가 겹쳐 가장 현실감이 있는 TV로 인정받았다. 8K LCD TV는 삼성전자와 샤프 이외에도 베스텔에서도 전시되었다.

<삼성전자 8K QLED TV>

<LG전자 88인치 8K OLED TV>

<베스텔 75인치 8K LCD TV>

세번째는 올해의 화두로 떠오른 micro LED TV다. CES2018에 처음으로 삼성전자가 공개한 micro LED TV는 100인치 이상 크기의 초대형 TV와 퍼블릭 시장을 만들수 있는 제품으로 인지되고 있다, 이 시장에 LG전자도 가세하기 위해 IFA2018에 173인치 4K micro LED TV를 출품하였다.

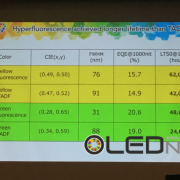

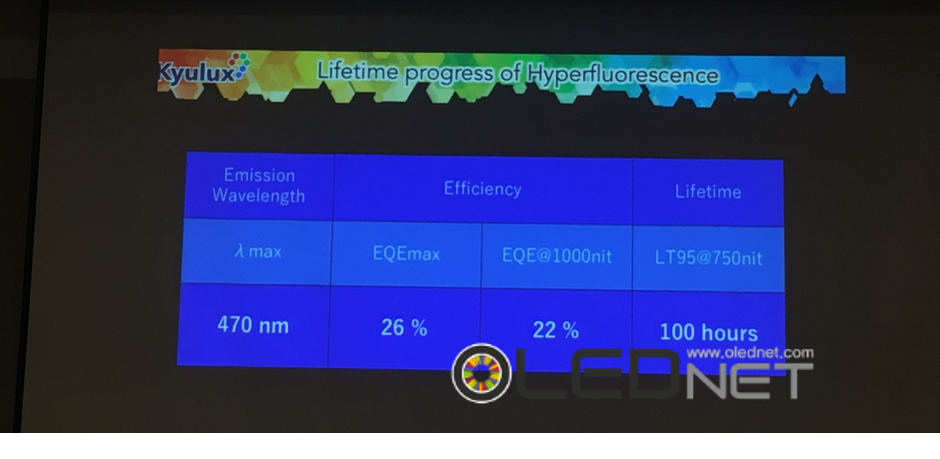

At IMID 2018 in Busan, BEXCO on August 31, Junji Adachi, CEO of Kyulux disclosed the performance of hyperfluorescence, which adds TADF dopant to the existing fluorescent host and dopant.

The color coordinates of the yellow hyperfluorescence revealed by Junji Adachi are (0.49, 0.50), the FWHM (Full Width at Half Maximum) is 76 nm, the EQE is 15.7% on 1000 nit basis, and the LT50 is 62,000 hours by 1000 nit. And the color coordinates of the green hyperfluorescence are (0.28, 0.65), the FWHM (Full Width at Half Maximum) is 31 nm, the EQE is 20.6% on 1000 nit basis, and the LT50 of 1,000 nit is 48,000 hours.

Junji Adachi also revealed the performance of Blue hyperfluorescence, which is currently under development. The maximum emission wavelength of the blue hyperfluorescence is 470 nm, the EQE at 1000 nit is 22%, and the LT50 at 750 nit is 100 hours. In particular, he predicted that the performance of Blue hyperfluorescence would be further improved in the future, saying that it began to improve rapidly in the first half of 2018.

In the following announcement, Dr. Georgios Liaptsis of CYNORA explained about the deep Blue under development, emphasizing that the wavelength should be 460 nm and the CIEy should be within 0.15. He revealed its performance, adding that CYNORA has been carrying out the necessary research to make the lifetime of deep Blue as long as that of sky Blue even with phenomenon that the life span is getting longer as the Blue goes closer to the sky Blue

Fluorescent blue is currently used for the Blue of all OLED applications. Attention is growing whether Blue TADF or Blue Fluorescence can be commercialized to realize better efficiency and lifetime than existing fluorescent blue.

At IMID 2018 held in BEXCO, Busan, Korea on August 29, Kwak Jin-Oh, vice president of Samsung Display, delivered a keynote speech on the theme of ‘The Infinite Evolution with Display’. He emphasized “Display will be the key material to link to the smart world and the creation of a new world and environment will be accelerated.”

Comparing the evolution of living things with the evolution of displays, Kwak pointed out the direction of the next-generation displays such as ‘size diversity from small to large size, adaption in design inclusive of full screen and flexible, and convergence with other technologies’.

In terms of size diversity, Kwak said, “High-resolution displays that can feel realism in small and medium-sized area, and displays that can be immersed like a big screen in a movie theater in large area, are required.”

The design adaptation then was referred to design autonomy as one of the values of next-generation displays. He further emphasized the value of rollable and stretchable displays as well as foldable displays in small and medium sized displays.

Kwak said that Samsung is developing rollable displays as well as foldable displays that are currently attracting great interest. Unlike foldable display, rollable display requires consideration of the stress on the front of the panel. He commented “Because there are many things to consider such as the time when it is rolled up, and the number of times it is rolled and unrolled, the company is conducting research to solve them.”

He also introduced a stretchable display that can implement patterns freely, and explained that it is developing various structures using RGB pixel unit and stretchable unit to implement displays that have high reliability with low stress.

Mentioning about biotechnology at the convergence area, he pointed out that new fusion technologies need to be considered such as measurement of oxygen saturation by transmitting light to hemoglobin or changes in the wake up mode and sleep mode of the display depending on the melatonin change.

Finally, Kwak concluded that display is evolving to create a new society and environment, emphasizing that display is the key material to link between the individual and the smart world in the forthcoming 5G era.

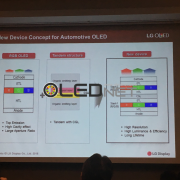

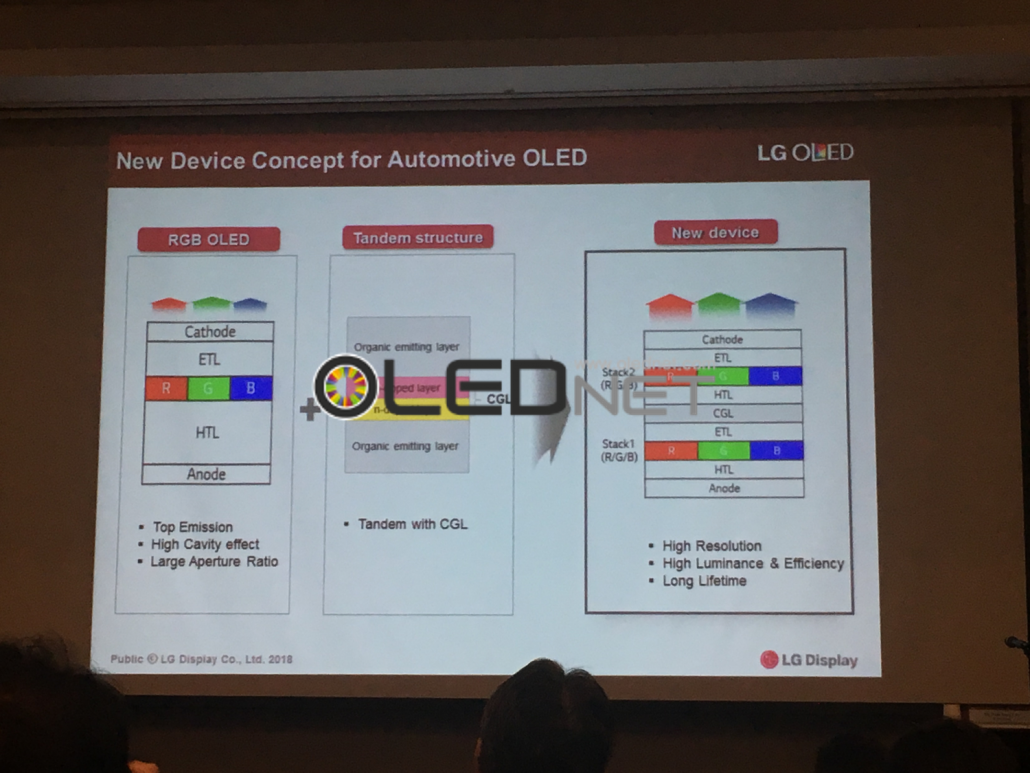

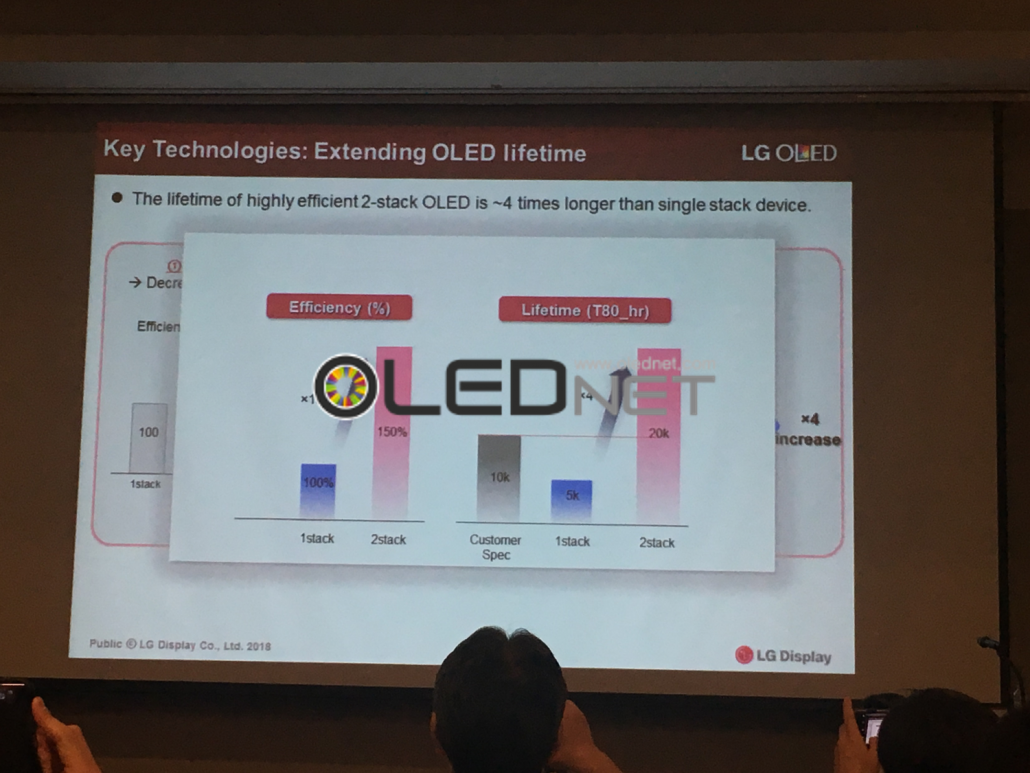

At IMID 2018 held in BEXCO, Busan on August 29, Kim Kwan-Soo, research fellow of LG Display presented about a new OLED technology for automotive displays.

Kim said that RGB OLEDs applied to mobile devices and WRGB OLEDs applied to TVs do not satisfy customers’ needs in terms of life span. To solve this issue, he introduced 2 stack RGB OLED in which RGB OLED has the same tandem structure as WRGB.

Because 2 stack RGB OLED can be thick due to adding a layer of CCL (charge generation layer) to the multi-layer structure, HTL is made thinner than before and the charge balance of the emitting layer is optimized.

As a result, the 2-stack RGB OLED shows 1.5 ~ 2 times higher emitting efficiency than the 1-stack RGB OLED. Its lifetime is increased by 4 times on T80 basis.

However, the 2-stack structure has a disadvantage in that it has higher power consumption than the general structure. Thus, it is necessary to make efforts to solve this disadvantage.

LG Display and Samsung Display introduced a number of applications using OLED at IMID 2018 held in BEXCO, Busan, drawing attention from many visitors. In particular, LG Display displayed its strategies mostly for large OLED applications such as 77-inch transparent OLED and 55-inch video wall OLED, while Samsung Display introduced the small and medium sized OLED applications mainly for automotive and virtual reality devices.

First, the panel thickness of the 77 inch transparent flexible OLED introduced by LG Display is 400 μm, the bending radius is 80 mm, and the luminance is 200 nit based on full white.

LG Display explained that it would improve the required transmittance and durability. Also, it commented that the goal is to reduce bezel to 0.5 mm at its display of 4 FHD OLEDs with 3.8 mm bezel.

In addition, LG Display presented a 1200ppi 4.3-inch WRGB OLED for virtual reality devices. One official explained that WRGB OLED, which represents the resolution by etching the color filter, would be advantageous for higher resolution than RGB using the deposition method.

Meanwhile, Samsung Display exhibited a number of automotive OLEDs, including unbreakable OLED for 6.22 inch steering wheel, 1000R curved OLED for passenger monitor, transparent OLED for HUD, S-curved OLED for CIO and rollable OLED. The concerned official expects the OLED to be widely applied to inside automobiles because it has excellent design autonomy, compared to LCD.

He added “Although there are many things to be improved, such as brightness and reliability, it is continuously improving the required performance through the feedback from European customers”.

Furthermore, Samsung Display showcased light field display and 2,000ppi resolution RGB OLED for virtual reality devices.

OLEDON is a company which develops plane source deposition technology for high resolution AMOLED manufacturing. Hwang Chang-Hoon, CEO of OLEDON announced in IMID 2018 that it developed ‘curved plane source FMM deposition technology’ that can be adopted to 2250ppi AMOLED pixels, for the first time in the world.

Conventional linear source FMM deposition technology has a shadow distance of 3um. The available production range is 570ppi AMOLED resolution. On the other hand, the plane source deposition technology already demonstrated in OLEDON can achieve a resolution of 800 to 1200 ppi of AMOLED with a shadow distance of 0.8 to 1.5 μm. Meanwhile, the newly developed ‘curved plane source FMM deposition technology’ is an upgraded technology of the plane source deposition technology which can realize the maximum resolution of AMOLED to 2250ppi with a shadow distance of 0.18 ~ 0.6μm.

The principle is that light is gathered through a concave mirror, a curved surface is applied to the conventional flat plane source, and the light emitting material does not spread, but is precisely deposited at a desired position, thereby reducing the shadow distance.

If this technology is commercialized, it is expected that it can be widely applied not only to mobile devices but also to virtual reality devices.

OLED TV로 프미리엄 TV 사업을 성공적으로 부활시킨 소니가 모바일에도 OLED를 탑재했다. 기존의 Xperia 시리즈와 유사한 살짝 굴곡있는 유리 뒷면과 6인치 디스플레이를 채택했다. 뒷커버의 디자인을 두고 소니는 삼성과 애플등과 비교했을 때 손에 잡기 쉽도록 했다고 발표했다. 최근 iPhone의 M자형 디자인과 유사한 디자인의 스마트폰이 출시되고 있는 것과 비교, 소니는 뒤쪽 하단에 작은 홈을 만들었다. 이 홈의 기능에 대해서는 아직 알려진 바가 없으나 디자인 차별성의 의미로 해석해 본다.

경쟁사의 OLED 채택 스마트폰 출시에 비해 많이 늦었지만 스크린 사이즈를 최대한으로 키우고, 가장 경쟁력 있다고 할 수 있는 부분인 색감, 색재현율 등에서 많은 노력을 하였다. 19메가 픽셀 센서 카메라에는 최근의 트렌드를 반영하며 AI 기능을 더했고 사용자의 편리성을 위해 물리적 버튼도 동기화 했다. Xperia XZ3의 마케팅 포인트 중 하나는 점점 디스플레이 사이즈가 커짐에 따라 한손으로 동작하기 불편함에 대해 “한손으로 동작가능한 디자인”으로 보인다. 디스플레이의 끝 부분에 두번 탭을 통해 바로가기 메뉴등을 실행할 수 있도록 했다. Xperia XZ3은 2018년 9월 말부터 한국을 제외하고 다양한 국가 및 지역에서 출시될 예정이다.

OLED TV에 이어 소니의 감성을 담은 스마트폰을 기다려온 소비자들에게는 신규제품에 대한 희소식이고, 디스플레이 산업에 또한 그동안 모바일 사업에서 부진을 겪어온 소니가 OLED 채용으로 TV사업에서와 같은 부활을 할 수 있을지 지켜 볼 수 있는 제품이 아닐까 생각한다.

JOLED, the world’s first to successfully commercialize solution process OLED products, announced that it had raised a total of 47 billion yen as a third-party capital increase.

According to JOLED, Denso will invest 30 billion yen, Toyota Tsusho 10 billion yen, Sumitomo chemical 5 billion yen and SCREEN Finetech Solutions 2 billion yen. JOLED is known to cooperate with Denso to develop automotive displays and Sumitomo chemical to develop OLED materials for solution process.

In particular, Denso has been mainly using TFT-LCD for automotive displays, but it is expected to lead the development for applying lightweight and easy-to-shape OLED to automobile interior through this investment.

It is expected that this funding will accelerate the establishment of production system for the mass-production of JOLED’s solution process OLED. JOLED announced on July 1 that it would set up a “JOLED Nomi Office” in Nomi-city, Ishikawa, and aim to operate in 2020.

Major production products are medium-sized (10 to 32-inch) solution process OLEDs that will be used for cars or high-end monitors. Also, Toshiaki Arai, chief technologist of JOLED announced that they would target the middle-sized OLED market with solution process OLED, at the 2018 OLED Korea conference hosted by UBI Research in March.

8월 31일 부산 BEXCO에서 열리고 있는 IMID 2018에서 Kyulux의 CEO, Junji Adachi는 기존의 형광재료 host와 dopant에 TADF dopant를 첨가하는 hyperfluorescence의 성능들을 공개했다.

Junji Adachi가 공개한 노란색 hyperfluorescence의 색좌표는 (0.49,0.50), 반치폭은 76 nm, 1,000 nit 기준 EQE는 15.7%, 1000 nit 기준 LT50은 6만 2천시간이며, 녹색 hyperfluorescence의 색좌표는 (0.28,0.65), 반치폭은 31 nm, 1000 nit 기준 EQE는 20.6%, 1,000 nit 기준 LT50은 4만 8천시간이다.

이 자리에서 Junji Adachi는 현재 개발 중인 청색 hyperfluorescence의 성능도 공개했는데, 최대 발광 파장은 470 nm, 1000 nit 기준 EQE는 22%, 750 nit 기준 LT50은 100시간이라고 밝혔다. 특히, 2018년 상반기부터 청색 hyperfluorescence의 성능이 빠른 속도로 향상되기 시작했다며 앞으로 성능이 더욱 더 향상 될 것으로 기대했다.

이어진 발표에서 CYNORA의 Dr. Georgios Liaptsis는 현재 개발 중인 진한 청색(deep blue)을 설명하며 파장은 460 nm, CIEy는 0.15 이내가 되야 한다고 강조했다. 연한 청색(sky blue)로 갈수록 수명이 길어지는 특징이 있는데, CYNORA는 진한 청색으로 연한 청색만큼의 수명을 가질 수 있도록 연구를 진행하고 있다고 설명하며 성능을 공개했다.

현재 모든 OLED application의 청색은 형광 청색이 사용되고 있다. 청색 TADF나 청색 hyperfluorescence가 상용화 되어 기존의 형광 청색보다 더 개선 된 효율과 수명을 보여줄 수 있을지 귀추가 주목된다.

8월 29일 부산 BEXCO에서 개최된 IMID 2018 에서 곽진오 Samsung Display 부사장은 ‘The Infinite Evolution with Display’를 주제로 기조연설을 진행하며, “디스플레이가 스마트 세계를 연결해줄 핵심 소재가 될 것이며 새로운 세계와 환경의 창조를 가속화 할 것”이라 강조했다.

곽 부사장은 생물의 진화와 디스플레이의 진화를 비교하며 ‘소형부터 대형까지 디스플레이 크기의 다양성(size diversity)과 full screen, flexible 등 디자인 적응(adaption in design), 다른 기술들과의 통합(convergence)’ 등 차세대 디스플레이가 나아갈 방향을 제시했다.

크기의 다양성에서 곽 부사장은 “중소형 부분에서는 현실감을 느낄 수 있는 고해상도의 디스플레이가, 대형 부분에서는 영화관의 큰 화면처럼 몰입 할 수 있는 디스플레이가 요구된다”라고 밝혔다.

이어서 디자인 적응에서는 차세대 디스플레이의 가치 중 하나로 디자인 자율성을 언급하며, 중소형 디스플레이는 폴더블 디스플레이 뿐만 아니라 롤러블과 스트레처블 디스플레이의 가치를 강조했다.

곽 부사장은 현재 이슈가 되고 있는 폴더블 디스플레이 뿐만 아니라 롤러블 디스플레이도 개발하고 있다고 언급했다. 폴더블 디스플레이와 다르게 패널 전면에 가해지는 스트레스를 고려해야 하는 롤러블 디스플레이는 말려져 있는 시간과 말았다 펴지는 횟수 등 고려해야 하는 사항이 많기 때문에, 이를 해결하기 위한 연구를 진행하고 있다고 발표했다.

또한 디스플레이 패널을 자유자재로 형태를 구현할 수 있는 스트레처블 디스플레이도 소개하며, 낮은 스트레스와 함께 높은 신뢰성을 갖는 디스플레이 구현을 위해 RGB 픽셀 유닛과 스트레처블 유닛을 활용한 다양한 구조들을 개발하고 있다고 설명했다.

융합 부분에서는 바이오 기술들을 거론하며 헤모글로빈에 빛을 투과해 산소포화도를 측정하거나.멜라토닌 변화에 따라 디스플레이의 wake up 모드와 sleep 모드 변화 등 새로운 융합 기술도 고려해야 한다고 언급했다.

마지막으로 곽 부사장은 앞으로 열릴 5G 시대에서 디스플레이가 개인과 스마트 세계를 연결할 핵심 소재임을 강조하며 새로운 사회와 환경을 창조하기 위해 디스플레이는 지속적으로 진화하고 있다고 설명하고 발표를 마무리했다.

소니가 IFA2019에서 공개한 AF9 시리즈 OLED TV는 차세대 고화질 프로세스 X1 Ultimate로서 약 2배의 리얼타임 화상처리 능력을 실현하여 현실 세계에 가까운 깊은 검정색과 밝은 흰색 표현이 가능하도록 했다.

음향 처리부분에서는 acoustic surface audio+ 기술로서 본체 후면 좌우의 actuator에 더하여 가운데에도 actuator를 설치하였다. 여기에 배면 스탠드에 서브 우퍼를 좌우 설치하여 3.2 채널 98W의 임장감을 표현하는 고화질 사운드를 완성하였다.

9월부터 유럽에 판매 예정이며 65인치 가격은 3,999 유로, 55인치는 2,999유로이다.

일본에서 OLED TV를 판매하고 있는 회사는 엘지전자와 소니, 파나소닉, 토시바 4개사이다. 이들 회사들에서 OLED TV 가격이 가장 높은 회사는 소니이지만 판매량은 가장 높은 것으로 알려져 있다.

소니의 일본애 시장뿐만 아니라 해외 시장에서도 높은 브랜드 인지도를 바탕으로 OLED TV 사업을 확충할 예정이다. 내년에는 8K OLED TV 판매도 계획하고 있다.

LG Display와 Samsung Display가 부산 BEXCO에서 열리고 있는 IMID 2018에서 OLED를 활용한 다수의 application을 선보이며 관람객들의 이목을 집중시켰다. 특히, LG Display는 77인치 transparent flexible OLED와 55인치 video wall OLED 등 대형 OLED application 위주로 전시한 반면, Samsung Display는 자동차용과 가상현실 기기용 OLED 등 중소형 OLED application을 주로 선보이며 뚜렷하게 서로 다른 사업 전략을 선보였다.

먼저, LG Display에서 77 inch transparent flexible OLED의 패널 두께는 400 um, 곡률 반경은 80 mm, 휘도는 full white 기준으로 200 nit다. LG Display는 부족한 투과도와 내구성을 더 개선시킬 것이라 언급했다. 또한, 3.8 mm narrow bezel을 가진 4장의 FHD OLED를 전시하며 bezel을 0.5 mm 까지 줄이는 것이 목표라고 설명했다.

이 밖에 LG Display는 가상현실 기기용 1200ppi 4.3 인치 WRGB OLED를 선보였다. 관계자는 color filter를 에칭하여 해상도를 나타내는 WRGB OLED가 증착 방식을 이용하는 RGB보다 고해상도에 유리할 것이라고 설명했다.

한편, Samsung Display는 6.22인치 steering wheel용 unbreakable OLED와 동승자 모니터용 1000R curved OLED, HUD용 투명 OLED, CID용 S-curved OLED, rollable OLED 등 OLED를 활용한 다수의 자동차용 OLED를 전시했다. 업체 관계자는 OLED가 LCD보다 디자인 자율성이 매우 뛰어나기 때문에 자동차 내부에 폭 넓게 적용될 수 있을 것이라 기대했다.

아직 개발 중인 단계로 휘도와 신뢰성 등 개선해야 할 사항은 많지만, 현재 유럽의 고객사들과의 피드백을 통해 지속적으로 성능을 개선하고 있다고 설명했다.

이 밖에, Samsung Display는 light field display와 가상현실 기기용 2000ppi 해상도의 RGB OLED 등을 선보였다.

고해상도 AMOLED 제조용 면소스 증착기술을 개발하고 있는 OLEDON의 황창훈 대표는 2250ppi의 AMOLED 화소의 증착이 가능한 곡면 소스 FMM 증착기술을 세계 최초로 개발하였다고 IMID 2018에서 발표했다.

기존의 리니어 소스 FMM 증착기술은 섀도우거리가 3 um으로서 생산 가능한 AMOLED의 해상도는 570ppi 수준이다. 반면, OLEDON에서 이미 선보인 바 있는 면소스 증착기술은 섀도우거리가 0.8~1.5 um 으로서 AMOLED의 해상도를 800~1200ppi까지 구현할 수 있다. 한편, 이번에 새로 개발된 곡면소스 FMM 증착기술은 섀도우거리가 0.18~0.6 um로서 AMOLED의 최대 해상도를 2250ppi까지 구현 가능한 면소스 증착기술의 업그레이드 기술이다.

원리는 오목거울을 통해 빛을 모으는 것처럼, 기존의 평평한 면 소스에 곡면을 가해 발광재료가 퍼지지 않고 원하는 곳에 정확히 증착 되어 섀도우 거리를 줄일 수 있는 방식이다.

이 기술이 상용화 된다면 mobile 기기 뿐만 아니라 가상현실 기기 등 폭넓게 적용될 수 있을 것으로 기대를 모으고 있다.

2018년 8월 부산에서 개최된 imid는 점점 전시의 규모를 키워가고 있음을 보여주었다. 대한민국 디스플레이 산업을 이끄는 삼성디스플레이와 엘지디스플레이는 모두 투명 디스플레이를 전시하였다. 엘지디스플레이는 77인치 탑에미션 방식의 투과율40% 투명 디스플레이와 55인치 FHD OLED 패널 3장을 이어붙인 비디오 월을 전시하였다. 비디오 월은 베젤이 3.5mm 에 불과하며 이 외에도 VR OLED 패널을 전시 지속적인 개발을 통해 성능이 향상되고 있음을 보여주었다.

삼성디스플레이 역시도 투명 디스플레이를 전시하였는데, 엘지디스플레이가 대형 OLED 산업을 이끈다면 삼성디스플레이는 중소형 OLED 산업을 이끄는 위치에 있음을 대변 하듯, 자동차용 사이즈의 투명 디스플레이를 전시하였다. 투명 OLED 디스플레이 사용을 통해 HUD 디자인 발전 가능성을 시사하였으며 이 외에도 다양한 자동차용 플렉서블 OLED 디스플레이를 전시하였다. 이를 통해 삼성디스플레이가 본격적으로 자동차용 OLED 패널 사업을 하고자 하는 의지를 엿볼 수 있었다. 또한 616ppi의 3.5인치 OLED패널을 사용한 VR과 1200ppi의 2.43인치 OLED 패널을 사용한 VR 을 전시하였다.

두 패널 회사들 외에도 머크, 희성소재를 비롯한 다양한 재료와 장비 업체에서도 학회 전시 참여를 통해 학계와 산업에 기여함과 동시에 사업을 소개하는 장소로 활용하고 있었다. 세계 최고의 OLED 산업리서치 업체인 유비리서치도 이번 기회를 통해 2018년 새롭게 구성한 Market Track등의 보고서를 소개하고 있다.

8월 29일 부산 BEXCO에서 열린 IMID 2018에서 LG Display의 김관수 연구위원(research fellow)은 자동차용 디스플레이에 적용될 새로운 OLED 기술에 대해 발표했다.

김 연구위원은 현재 모바일 기기에 적용되고 있는 RGB OLED와 TV에 적용되고 있는 WRGB OLED는 수명 측면에서 고객사들의 요구를 만족시키지 못하고 있기 때문에, 이를 해결하기 위한 방법으로 RGB OLED를 WRGB처럼 tandem 구조를 갖는 2 stack RGB OLED를 소개했다.

2 stack RGB OLED는 다층구조에 CGL(charge generation layer) 층이 더해져 두께가 두꺼울 수 있기 때문에 HTL을 기존보다 얇게 만들고 발광층의 charge balance를 최적화하였다.

그 결과 1 stack RGB OLED보다 1.5배에서 2배 향상된 발광효율과 함께 수명이 T80 기준으로 4배 이상 증가하는 효과가 나타났다고 보고했다.

하지만 2 stack 구조는 일반 구조에 비해 소비 전력이 높은 단점이 있어 이를 해결하기 위한 노력이 필요하다고 지적했다.

유럽 최대 가전 전시회인 IFA의 엘지전자 TV 부스는 역시 OLED가 TV의 주력을 차지하였다. CES2018에는 전시되지 않았던 88인치 8K OLED TV가 공개상에서 최초로 모습을 드러내었다.

88인치 8K OLED TV는 OLED의 화려한 색상과 완벽한 블랙에 초고해상도가 더해져서 입체감이 한층 살아난 최상의 TV임을 보여주고 있다. 엘지전자 관계자에 의하면 프리미엄 TV 해상도가 4K를 넘어 이미 8K 시장으로 진입을 시작했기 때문에 OLED TV도 이에 대응할 수 있는 제품이 필요한 시기가 되었다고 언급했다.

LG디스플레이는 88인치 이외 75인치와 64인치 8K OLED 패널을 개발중에 있으며 내년에는 이들 제품들이 모두 시장에 나올 수 있을 것으로 기대된다. 현재 개발중인 8K OLED 패널은 모두 bottom emission 구조이다.

엘지전자는 CES2018에서 화질 프로세스 알파9으로 좋아진 OLED TV의 화질 소개에 중점을 두고많은 장소를 할애하였으나 88인치 8K OLED에 장소를 양보하고 간결하게 전시 공간을 꾸몄다.

OLED TV 성능 소개를 “Crisp and Smooth Motion”과 “Clean, Sharp, and Vibrant Images” 두 가지로 압축하였다. 이들 성능들은 화질 분야에서 최고로 인정받고 있는 소니와 경쟁할 수 있는 수준에 도달하였음을 나타내고 있다.

OLED TV 성능 소개를 “Crisp and Smooth Motion”과 “Clean, Sharp, and Vibrant Images” 두 가지로 압축하였다. 이들 성능들은 화질 분야에서 최고로 인정받고 있는 소니와 경쟁할 수 있는 수준에 도달하였음을 나타내고 있다.

2018년 8월 부산에서 개최된 imid는 점점 전시의 규모를 키워가고 있음을 보여주었다. 대한민국 디스플레이 산업을 이끄는 삼성디스플레이와 엘지디스플레이는 모두 투명 디스플레이를 전시하였다. 엘지디스플레이는 77인치 탑에미션 방식의 투과율40% 투명 디스플레이와 55인치 FHD OLED 패널 3장을 이어 붙인 비디오 월을 전시하였다. 비디오 월은 베젤이 3.5mm 에 불과하며 이 외에도 VR OLED 패널을 전시 지속적인 개발을 통해 성능이 향상되고 있음을 보여주었다.

삼성디스플레이 역시도 투명 디스플레이를 전시하였는데, 엘지디스플레이가 대형 OLED 산업을 이끈다면 삼성디스플레이는 중소형 OLED 산업을 이끄는 위치에 있음을 대변 하듯, 자동차용 사이즈의 투명 디스플레이를 전시하였다. 투명 OLED 디스플레이 사용을 통해 HUD 디자인 발전 가능성을 시사하였으며 이 외에도 다양한 자동차용 플렉서블 OLED 디스플레이를 전시하였다. 이를 통해 삼성디스플레이가 본격적으로 자동차용 OLED 패널 사업을 하고자 하는 의지를 엿볼 수 있었다. 또한 616ppi의 3.5인치 OLED패널을 사용한 VR과 1200ppi의 2.43인치 OLED 패널을 사용한 VR 을 전시하였다.

두 패널 회사들 외에도 머크, 희성소재를 비롯한 다양한 재료와 장비 업체에서도 학회 전시 참여를 통해 학계와 산업에 기여함과 동시에 사업을 소개하는 장소로 활용하고 있었다. 세계 최고의 OLED 산업리서치 업체인 유비리서치도 이번 기회를 통해 2018년 새롭게 구성한 Market Track등의 보고서를 소개하고 있다.

세계 최초로 solution process OLED 제품화에 성공한 JOLED가 23일 제 3자 할당 증자로 총 470억엔을 조달했다고 발표했다.

JOLED에 따르면 Denso가 300억엔, Toyota Tsusho가 100억엔, Sumitomo chemical이 50억엔, SCREEN Finetech Solutions이 20억엔을 투자할 것이며, Denso와는 자동차용 디스플레이 개발을, Sumitomo chemical과는 solution process용 OLED 재료 개발에 협력 할 것으로 알려졌다.

특히 Denso는 그 동안 자동차용 디스플레이용으로 주로 TFT-LCD를 사용했으나, 이번 투자를 통해 가볍고 곡면화가 용이한 OLED를 자동차 내부에 적용하기 위한 개발에 앞장 설 것으로 기대를 모으고 있다.

이번 자금 조달을 통해 JOLED의 solution process OLED 양산을 위한 생산 체제 구축이 가속화 될 것으로 기대된다. JOLED는 7월 1일에 이시카와현 노미시에 ‘JOLED 노미 사업소’를 개설하고 2020년 가동을 목표로 하고 있다고 밝힌 바 있다.

주력 생산 제품은 자동차나 하이 엔드 모니터용 중형 (10~32 인치) solution process OLED로써, 지난 3월 유비리서치가 개최 한 2018 OLED Korea conference에서 Toshiaki Arai chief technologist는 solution process OLED로 중형 OLED 시장을 공략할 것을 밝히기도 했다.

<2018 OLED Korea conference에서 밝힌 JOLED의 개발 로드맵>

<Vivo’s full screen smart phone with in-display fingerprint scanner, Android authority>

The competition for front fingerprint recognition of smart phones is expected to become hot.

In the smart phone with the existing home button, the front fingerprint sensor was installed on the home button. Fingerprint security enhances security, but recently, full screen Smartphone without home button has been released and fingerprint sensor has been moved to the back of Smartphone. This has caused disadvantages such as an uncomfortable hand shape when touching a finger to the fingerprint sensor and fingerprints on the camera lens.

In order to improve these points and to implement a complete full-screen Smartphone, the development of integrating full-screen fingerprint recognition with display is continuing.

The method of full-screen fingerprint recognition is largely examined by both optical and ultrasonic methods. The optics are inexpensive and easy to mass-produce, but the OLED substrate must be transparent because the sensor is to be located below the OLED panel. Therefore, it is applicable to rigid OLED using glass as a substrate, but it is difficult to apply to flexible OLED using colored PI as a substrate. The ultrasonic method is most stable in accuracy and durability, but it has a disadvantage of high manufacturing cost.

Currently, Chinese set makers have begun to launch smart phones with optical front fingerprint recognition. The Galaxy S10, which will be released next year by Samsung Electronics, is being watched for the adoption of ultrasonic full-screen fingerprint recognition. LG Display is also developing a display with front fingerprint recognition.

As such, the sales for full-screen smart phones with front fingerprint recognition are expected to be started in earnest. Competition in the smartphone market is expected to become more intense in the second half.

<전면지문인식을 탑재한 디스플레이가 적용된 VIVO의 스마트폰, Android authority>

스마트폰의 전면지문인식경쟁이 뜨거워질 것으로 예상된다.

기존 홈버튼이 있는 스마트폰에는 홈버튼에 전면 지문인식 센서를 탑재하여 제품이 출시되었다. 지문을 이용한 보안강화로 소비자들의 큰 호응을 얻었지만 최근 홈버튼이 없는 풀스크린 스마트폰 위주로 제품이 출시가 되며 지문인식 센서도 스마트폰의 뒷면으로 옮겨졌다. 이로 인해 지문인식 센서에 손가락을 터치할 때 불편한 손모양과 옆에 위치한 카메라렌즈에 지문이 묻는 등 단점이 발생했다.

이러한 점들을 개선하고 완벽한 풀스크린 스마트폰을 제조하기 위해 전면지문인식을 디스플레이와 일체화 시키려는 개발이 지속되고 있다.

전면 지문인식은 크게 광학식과 초음파식이 검토되고 있다. 광학식은 가격이 저렴하고 양산에 용이하지만, 센서가 OLED panel 하부에 위치해야 하므로 OLED 기판이 투명해야한다. 따라서 glass를 기판으로 사용하는rigid OLED에는 적용이 가능하지만 유색PI를 기판으로 사용하는 flexible OLED에는 적용이 어려운 상황이다. 초음파식은 정확성과 내구성이 가장 안정적이지만 제조가격이 비싸다는 단점이 있다.

현재 중국 set업체들은 광학식 전면 지문인식을 채택한 스마트폰 출시를 시작하였으며, 삼성전자에서 내년 출시예정인 galaxy S10에 초음파식 전면지문인식을 채택 여부가 관심을 모으고 있다. 또한 LG 디스플레이도 전면지문인식을 탑재한 디스플레이를 개발 중에 있는 것으로 알려졌다.

이처럼 풀스크린에 전면지문인식을 탑재한 스마트폰 출시가 본격화 될 것으로 기대되는 가운데 하반기 스마트폰 시장의 경쟁이 더욱 치열해 질 것으로 기대된다.

Samsung Electronics announced its sales of KRW 58.48 trillion and operating profit of KRW 14.87 trillion through the earnings conference call of the second quarter, 2018 on July 31. Its sales decreased by 4% YoY and the operating profit increased by KRW 800 billion. Sales decreased 3% QoQ and operating profit fell by KRW 800 billion QoQ.

According to Samsung Electronics, the display panel business recorded sales of KRW 5.67 trillion and operating profit of KRW 140 billion, due to slowing demand for flexible OLED panels and declining sales of LCD TV panels. Despite improved utilization of rigid OLED, OLED division’s earnings declined QoQ due to continued weak demand for flexible products.

Competition with LTPS LCD is expected to intensify at rigid OLED in the second half of 2019, but earnings are to improve on increased sales following the recovery of flexible product demand. Sales and operating profit are projected to improve in the second half on the back of production of flexible OLED for Apple’s new iPhone models from 2Q.

Samsung Electronics plans to expand its share of OLEDs for mobile devices by strengthening its differentiated technology and cost competitiveness, and to strengthen its capacity for new products such as foldable OLEDs. Samsung official said that foldable OLED will contribute to growth from next year rather than immediate performance in the second half of the year.

IT • Mobile (IM) division posted sales of KRW 24 trillion and operating profit of KRW 2.67 trillion. Operating profit fell 34.2 percent from KRW 4.06 trillion in the same period a year ago, and also fell sharply from the previous quarter (KRW 3.77 trillion). In 2Q, handset sales reached 78 million units, of which 90% are smart phones. 5 million units of tablet were sold. The average selling price (ASP) of the handsets is in the second half of US$ 220. The Consumer Electronics (CE) division posted sales of KRW 10.4 trillion and operating profit of KRW 510 billion in the second quarter of the year. Overall sales and operating profit of the first half of the year were KR W 20.14 trillion and KRW 0.79 trillion, respectively. TV profits improved thanks to robust sales of high value-added products such as QLED TVs amid the global sports events. On the other hand, SEC’s facility investment in the second quarter was KRW 8 trillion. By business, semiconductor area accounted for KRW 6.1 trillion and KRW 1.1 trillion was invested for display area. In the first half, a total of KRW 16.6 trillion was invested; including KRW 13.3 trillion in semiconductors and KRW 1.9 trillion in display.

LG Display delivered 30 OLED lighting units, made by its employee volunteers, and baby products to 30 unmarried mothers.

This volunteer activity was carried out by the talent services of OLED lighting employees. OLED lighting business division donated 30 flexible OLED lighting panels, and the product planning team customized the lightings for breastfeeding for unwed mothers.

On July 27, the employee volunteers assembled light fixtures, which were customized by woodworking parts through social enterprises, and panels as finished products. In addition, various items needed for a baby and cheer letters for the unwed mothers were packed together. The packaged gift sets were delivered to 30 unmarried mothers living at the unmarried mothers’ facilities through the Eastern Social Welfare Society on July 30.

OLED lighting reduces light flickering and blue light, which affect eye health. And its mild light protects you from eye fatigue. It is also regarded as an eco-friendly product because it generates less heat and has no harmful substances. Since it is the organization that best knows the characteristics of OLED lighting, it suggested the service of delivering the OLED lighting for breastfeeding, made by its members, suitable for the baby-care environment.

Kim Yong-Jin, manager of the OLED lighting sales team who participated in the volunteer service, said “I feel it was worthwhile to deliver the OLED lighting directly to the necessary neighbors although I have dealt with it for business. When I see the neighbors who were delighted with little help, I have to think once again that service activity is so much fun.

<Source: LG Display>

Samsung Electronics는 7월 31일 진행된 2018년 2분기 실적 컨퍼런스 콜을 통해 매출 58조 4800억원, 영업이익 14조 8700억원을 기록했다고 발표했다. 전년 동기 대비 매출은 4% 감소했고 영업이익은 8000억원 증가했다. 전분기 대비 매출은 3%, 영업이익은 8000억원 줄었다.

Samsung Electronics에 따르면, 디스플레이 패널 사업은 flexible OLED 패널 수요 둔화와 LCD TV 패널 판매 감소로 실적이 감소하며 매출 5조 6,700억원, 영업이익 1,400억원을 기록했다. OLED 부문은 rigid OLED 가동률이 개선되었음에도 불구하고, flexible 제품 수요 약세가 지속돼 전분기 대비 실적이 감소했다

하반기에는 rigid OLED에서 LTPS LCD와 경쟁이 심화될 것으로 예상되나, flexible 제품 수요 회복에 따른 판매 확대로 실적이 개선될 것으로 전망된다. 애플 아이폰 신모델용 flexible OLED를 2분기부터 생산함에 따라 하반기에 매출과 영업이익이 개선 될 것으로 예상된다.

Samsung Electronics는 차별화된 기술력과 원가 경쟁력 강화를 통해 모바일용 OLED 점유율을 확대하고 foldable OLED 등 신규 제품군 역량을 강화할 계획이다. foldable OLED는 당장 하반기 실적보다는 내년 이후 성장에 기여할 것이라고 언급했다.

IT·모바일(IM) 부문의 2분기 매출은 24조원, 영업이익은 2조 6,700억원을 기록했다. 영업이익은 전년 동기(4조600억) 대비 34.2% 줄었으며 전 분기(3조7700억원)보다도 크게 감소했다. 2분기 휴대폰 판매량은 7,800만대로, 이 중 90%가 스마트폰이다. 태블릿은 500만대가 판매됐다. 단말기 평균판매가격(ASP)은 220달러대 후반이다.

소비자가전(CE) 부문의 2분기 매출은 10조 4,000억원, 영업이익은 5,100억원을 기록했다. 상반기 전체로는 매출 20조 1,400억원, 영업이익 7,900억원이다. 글로벌 스포츠 이벤트 특수 속에 QLED TV 등 고부가 제품 판매 호조로 TV 이익이 개선되었다.

한편 삼성전자의 2분기 시설투자 규모는 8조원이었다. 사업별로는 반도체 6조 1,000억원, 디스플레이 1조 1,000억원 수준이다. 상반기 누계로는 반도체 13조 3,000억원, 디스플레이 1조 9,000억원 등 총 16조 6,000억원이 집행됐다.

LG디스플레이가 30일, 미혼모 30명에게 임직원 봉사자들이 직접 제작한 OLED조명등과 아기 용품을 전달했다.

이번 봉사활동은 OLED조명담당 임직원들의 재능봉사로 진행됐다. OLED조명사업사업담당에서 플렉서블OLED조명패널 30개를 기증하고 상품기획팀에서 미혼모의 수유등을 맞춤 디자인했다.

지난 27일, 임직원 봉사자들이 사회적 기업을 통해 맞춤 제작한 목공 부품으로 등기구와 패널을 완성품으로 조립했다. 또한, 아기에게 필요한 각종 물품들과 미혼모를 위한 응원 편지도 작성해 함께 포장했다. 포장된 선물세트는 30일, 동방사회복지회를 통해 미혼모시설에 생활중인 미혼모 30명에게 전달됐다.

OLED 조명은 눈 건강에 영향을 미치는 빛 깜빡임 현상과 청색광이 적고 은은한 빛을 내 눈의 피로를 줄여준다. 또한 발열이 적고 유해물질이 없어 친환경제품으로도 손꼽힌다. OLED조명의 특성을 가장 잘 아는 조직이기에 아기를 돌보는 환경에 적합한 수유등을 직접 만들어 전달하는 봉사를 제안했고 구성원 모두 재능을 더해 완성할 수 있었다.

봉사활동에 참여한 OLED 조명영업1팀 김용진 책임은 “업무로 늘 접하던 OLED조명이지만 꼭 필요한 이웃에게 직접 전달할 수 있어서 보람을 느꼈다”며 “작은 도움에도 기뻐하는 이웃들을 보니 봉사가 이렇게 즐거운 것이었나 다시 생각하게 됐다”고 소감을 밝혔다.

<Source: LG Display>

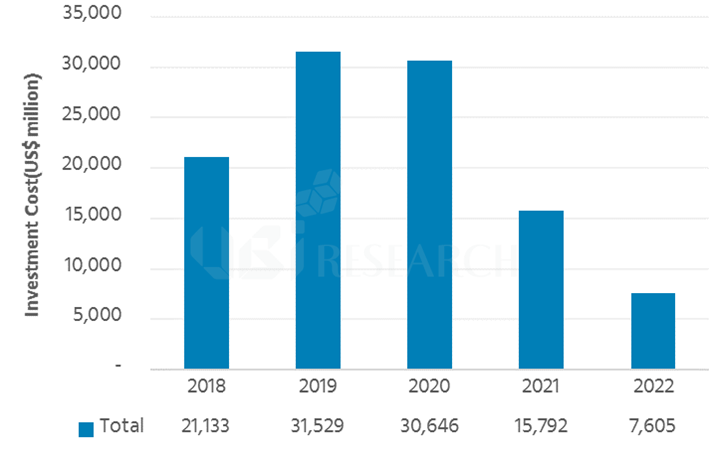

In the “2018 OLED Equipment Report” recently published by UBI Research, the required investment cost was analyzed for the QD-OLED that Samsung Display started to develop.

QD-OLED, which is being developed by Samsung Display, is a method of displaying three colors of RGB by separating green and red from the light emitted from blue OLED through QD (quantum dot) material. The light passing through the QD material once again passes through the color filter and displays a richer color.

QD-OLED is similar to the manufacturing method of WDRGB OLED produced by LG Display. First, both companies use oxide TFTs. At WRGB OLED, blue is applied twice and red and green are deposited between them. In contrast, QD-OLED is fabricated by depositing only blue material twice. Both methods use the open mask with an empty center.

For both QD-OLED and WRGB OLED, the color filter manufacturing cost is assumed to be same; however, QD-OLED should be equipped with additional equipment to coat QD materials.

According to the report, it is expected that the investment cost is to be equal because the similar equipment can be used for module, cell, encapsulation and evaporator. Since WRGB OLED is bottom emission type, it is formed together when backplane is formed including TFT. However, QD-OLED adopts top emission method. A color filter is separately formed on the top glass substrate and the QD layer is patterned thereon. Therefore, QD-OLED requires higher investment cost than WRGB OLED.

The report describes that based on 8Generation 26K, the investment cost for QD-OLED is estimated to be US$ 1.1 billion, which is 1.03 times higher than WRGB OLED (US$ 1.07 billion). In contrast, the required investment cost to manufacture OLED by inkjet method, which JOLED is promoting commercialization, is projected as US$ 0.88 billion, which is to be about 80% of QD-OLED.

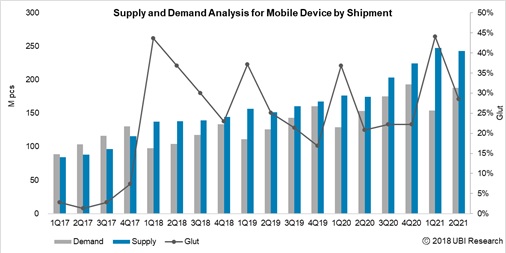

UBI Research recently published “2Q18 AMOLED Display Market Tracks”, which includes market updates of the second quarter of 2018. The report covers OLED display panel makers’ investment status, OLED display market forecasts from 2018 to 2022, OLED demand and supply trends, and competitiveness analysis of OLED Smartphone business for Samsung Display and other OLED display panel makers.

The market update, published with the Excel spreadsheet, describes the production line status and the added line status through future investments of the 15 OLED display panel makers worldwide. Also, it describes not only the major OLED application market such as smart phones and TVs, but also the market forecast by country.

The demand for OLED mobile sets (including smart phones and smart watches) in the first quarter of 2018 dropped to 98 million units from 130 million units in the fourth quarter of last year, due to the lower-than-expected performance of the premium smartphone market, where Samsung Electronics’ Galaxy S series and Apple’s iPhone occupy most of the market. OLED mobile set market is to recover gradually until 3Q, when Apple’s new smartphone model is launched, and by the end of 2018, the demand is expected to recover as to the similar level of the same period of last year. In addition, Samsung Display is anticipated to have a positive impact on the recovery of the Smartphone market in the second half of the year by securing competitiveness by lowering the sales price of rigid OLED panel for mobile phone to about US$ 25 to compete with LCD in China.

Consumers' smartphone replacement cycle is getting longer due to the reason that there is no revolutionary change in the new model compared to the past, and the Smartphone penetration in most of the countries except for India, South America and Africa is reaching the limit. Accordingly, the outlook for the downturn is mostly forecasted in the recent smartphone market. There is a growing interest in technology and design to apply a different form factor to revive the market. In this regard, Samsung Electronics' foldable OLED smartphone, which is scheduled to be released later this year or early next year, is expected to create a new momentum. Attention is focused on whether a folding- type flexible display (Dynamic Flexible Display) will be succeeded as a new type of smartphone from the existing edge-type flexible display (Static Flexible Display).

UBI Research predicts that the OLED Smartphone market will grow from 430 million units in 2018 to 900 million units in 2022, and the market for foldable OLED Smartphone is to be from about 1million units in 2019 to 18million units in 2022. This reflects the expansion of OLED panel production lines by panel makers such as LG Display and BOE, besides Samsung Display. It will be updated as new applications are developed in future and the Smartphone market moves forward.

In OLED panel market, OLED panel for Smartphone still occupies 91% of the whole market. Samsung Display has accounted for 90% of total OLED panel market performance and LG Display is followed with about 7.8% share.

OLED TVs, which are continuously increasing in demand worldwide compared to the Smartphone market, are expected to be in short supply this year. LG Display, the only OLED TV panel supplier, will continue to invest in production for the next five years. With the recent approval of new production facility for OLED TV panel in Guangzhou, the full-scale equipment move-in is expected this year. In Paju P10 investment plan, it was confirmed that LG Display will invest in OLED TV panel production line instead of LCD line investment which was examined before. Thus, the OLED TV market is projected to grow to US $ 5.6 billion.

In the 2Q earnings release conference call hosted on the 25th July, Kim Sang-don, LG Display CFO, said, “Looking back at the first half of 2018, the market was in a difficult situation due to the slump in prices, the traditional off-peak season and increased display supply from China. We expected the market conditions to be stabilized in the first half of this year from the bad market condition of the second half of last year, but it has continued to decline more rapidly and steeply. However, with starting the second half of 2018, it has been observing that the price is rising since July owing to upcoming favorable seasonality and customer restocking.”

“Although the market situation has changed favorably in the second half of the year, it is different from the past supply and demand cycle because of the uncertainty of forecasts. Moreover, the oversupply and asymmetric competition in the display market are unavoidable.” LG Display announced that it will maintain its conservative strategy in the second half of the year as the unpredictability is still high.

LG Display’s sales revenue in the second quarter of 2018 was KRW 5,611 billion, decreased by 15% compared to the second quarter of 2017. Operating loss in the second quarter of 2018 recorded KRW 228 billion. This compares with the operating loss of KRW 98 billion in the first quarter of 2018 and the operating profit of KRW 804 billion in the second quarter of 2017. The company suffered a large deficit due to a continued and steep decline in panel prices and lower demand in panels following the previous quarter. Although the shipment was increased by 2% QoQ, the selling price per area (m2) was decreased by 4%.

As a positive indicator, the TV panel price fell sharply, but the overall panel price decline was only 1% due to the competitive position of OLED panels. The market is anticipated to turn into positive situation in the third quarter, compared to the first half of the year, since panel shipments are expected to increase with the orders to restock the inventory.

LG Display, which is currently conducting both LCD and OLED business with small and medium sized panels and large area panels, mentioned clearly about its future strategic direction including the direction for the second half of the year as “concentrating on OLED business and focusing on high value of LCD business” in this conference call.

LG Display announced that it will focus more on differentiated LCD features and technologies in the IT sector such as narrow bezel, IPS borderless, and oxide technology, as well as high-value-added products such as larger-size TV panels and commercial displays, considering that a structural oversupply in panels and fierce competition among display makers are expected to continue down the road.

In addition, LG Display will achieve a turnaround to profit in the OLED TV sector in the third quarter of 2018. By making its final decision to invest in its Gen 10.5 OLED panel production line in Paju, Korea, and by starting mass production in the latter half of 2019 at its Gen 8.5 OLED production line now under construction in Guangzhou, China, LG Display will accelerate the expansion of the global large-size OLED market. Furthermore, additional production facilities for OLED 8.5 generation are known to be considered with the plan that the rationalization of LCDs during the year is also to be implemented although there was no direct mention of the timing and specific lines. For the plastic small and medium-sized OLED panel business, which is experiencing difficult times, compared to large area OLED, for which LG is expanding the production capacity in response to increasing demand, it said that they are preparing for future markets with the necessary strategic technologies with the emphasis of mobile and automotive markets. The E6-1 line, which has been mentioned as a production plant for Apple, is expected to begin mass production in the fourth quarter of this year, revealing the possibility of a possible supply of display to the iPhone OLED model in 2018. In addition, demand for OLED panels is increasing in the automobile market, and it is expected that full-scale business will start in the second half of next year. At the current order backlog, it is confirmed that OLED panels are in the late stage of about 10%. This means that much of the work has already been done. Finally, LG Display is well aware of the lack of funding and funding shortfalls over its competitors in relation to its future preparations. The company plans to reduce its capex by about 3trillion won by 2020, with a substantial portion of depreciation and amortization It is possible through internal working capital management and it plans to borrow the rest. LG Display confirmed that it has not reviewed the rights issue several times in the market, and LG Display has thoroughly prepared a variety of OLED portfolios, revealing its commitment to success by differentiating it from its competitors in the area of latecomers.

유비리서치에서 최근 발간한 “2018 OLED 장비 보고서”에서 삼성디스플레이가 개발을 시작한 QD-OLED 투자 비용이 얼마나 필요한지를 분석하였다.

삼성디스플레이가 추구하고 있는 QD-OLED는 청색 OLED에서 나오는 빛을 QD(quantum dot) 재료를 통하여 녹색과 적색을 분리하여 RGB 3색을 나타내는 방식이다. QD 재료를 통과한 빛은 다시한번 칼라 필터를 통과하며 보다 풍부한 색감을 나타내게 된다.

QD-OLED는 LG디스플레이가 제조하고 있는 WRGB OLED와 제조 방식과 유사한 부분이 매우 많다. 우선 TFT는 양사 모두 oxide TFT를 사용하고 있다. WRGB OLED는 청색이 두 번 도포되며 그 사이에 적색과 녹색이 증착 된다. 이에 비해 QD-OLED는 청색 재료만 두 번 증착하여 제작된다. 두 방식 모두 증착용 마스크는 가운데가 비어 있는 오픈 마스크를 사용한다.

QD-OLED와 WRGB OLED의 칼라필터 제조 비용을 동일할 것으로 추정되나 QD-OLED는 QD 재료를 코팅하는 장비가 추가로 도입되어야 한다.

보고서에 의하면 모듈과 cell, encapsulation, 증착기는 유사한 장비가 사용될 수 있어 투자 비용 역시 대등할 것으로 예상된다. 하지만 WRGB OLED는 bottom emission 방식이어서 TFT를 포함한 backplane 제조시에 같이 형성되나 QD-OLED는 top emission 방식을 추구하고 있어 상판 유리 기판에 칼라필터를 별도로 제작하고, 그 위에 다시 QD층을 패터닝하여 만든다. 따라서 QD-OLED는 WRGB OLED에 비해 다소 높은 투자 비용이 필요해진다.

8세대 26K 기준으로 투자비를 계산하였을 때 QD-OLED는 1.1 billion$로서 WRGB OLED 1.07 billion$에 비해 1.03배 높을 것으로 예상된다. 이에 비해 JOLED에서 사업화를 추진중인 잉크젯 방식의 OLED 제조에 필요한 투자 금액은 0.88 billion$로서 QD-OLED의 80% 수준이 될 것으로 본 보고서는 기술하고 있다.

유비리서치는 최근 2018년 2분기 시장 업데이트를 포함하는 “2Q 18 AMOLED Display Market Tracks”를 발간하였다. 이번에 발간한 내용은 OLED 디스플레이 패널 업체들의 투자 현황과 2018년부터 2022년까지의 OLED 디스플레이 시장전망, OLED 수요와 공급 트렌드, 그리고 삼성디스플레이와 전세계 OLED 디스플레이 패널 업체들과의 OLED 스마트폰 사업에 대한 경쟁력 분석을 포함하고 있다.

엑셀 스프레드시트에 Data의 형태로 발간된 시장 업데이트는 전세계 15개의 OLED 디스플레이 패널 업체들의 생산 라인 현황과 향후 투자를 통해 추가되는 라인 현황과 스마트폰, TV등 주요 OLED 어플리케이션 시장과 국가별 시장 전망 등을 주요 내용으로 다루고 있다.

삼성전자의 갤럭시S 시리즈와 Apple의 iPhone이 대부분의 시장을 점유하고 있는 프리미엄 스마트폰 시장이 예상치를 밑도는 실적으로 인해 2018년 1분기 전체 OLED 모바일 세트(스마트폰, 스마트 와치 등 포함) 시장의 수요는 작년 4분기 130백만대에서 98백만대로 감소했다. OLED 모바일 세트 시장은 Apple의 신규 스마트폰 모델이 출시되는 3분기까지 서서히 수요를 회복하여 2018년 말 경에는 작년 같은 시기 수요를 회복할 전망이다. 또한 삼성디스플레이가 중국시장에서 LCD와의 경쟁을 위해 모바일 용 Rigid OLED 패널의 가격을 약 25불 수준으로 낮춰 경쟁력을 확보함에 따라 하반기 스마트폰 시장의 회복에 긍정적인 영향을 줄 것으로 기대된다.

과거에 비해 신규 모델의 혁신적인 변화가 없는 등의 이유로 소비자들의 스마트폰 교체 주기가 길어지고 인도와 남미, 아프리카 등 제3세계 국가들을 제외한 대부분의 지역에서의 스마트폰 보급률이 거의 한계점에 다다라 최근 스마트폰 시장의 침체에 대한 전망이 대부분이다. 시장의 반등을 위해서 이전과는 다른 폼 팩터(Form factor)를 적용하기 위한 기술과 디자인에 대한 관심이 높아지고 있다. 이와 관련하여 올해 말 혹은 내년 초 출시를 예상하고 있는 삼성전자의 Foldable OLED 스마트폰을 놓고 기존의 엣지 형태의 플렉서블 디스플레이에서 (Static Flexible Display) 접는 형태의 플렉서블 디스플레이가 (Dynamic Flexible Display)가 새로운 스마트폰의 형태로서 성공할 것인가에 대해 관심이 집중되고 있다.

유비리서치는 2018년 4.3억만대의 OLED 스마트폰 시장이 2022년 약 2배의 9억대 수준으로 성장, Foldable OLED 스마트폰 시장은 2019년 약 1백만대에서 2022년 18백만대까지 성장할 것으로 기대하고 있다. 이는 LG디스플레이와 BOE등 삼성디스플레이 외 패널업체들의 OLED 패널 양산 라인 확대를 반영한 것으로 향후 신규 어플리케이션의 개발과 스마트폰 시장의 움직임에 따라 업데이트 할 예정이다.

OLED 패널 시장은 여전히 스마트폰 용 OLED 패널이 전체 시장의 91%를 점유하고 있으며 업체를 기준으로는 삼성디스플레이가 전체 OLED 패널 시장 실적의 90%를, LG 디스플레이가 뒤를 이어 약 7.8%를 차지하고 있는 것으로 나타났다.

스마트폰 시장에 비해 전세계 적으로 꾸준히 수요가 증가하고 있는 OLED TV는 올해도 수요에 비해 공급이 부족할 것으로 분석되며 유일한 OLED TV용 패널 공급업체인 LG디스플레이는 향후 5년간 생산확대를 위해 지속적인 투자를 진행할 예정이다. 최근 광저우 OLED TV 패널용 생산 공장의 승인으로 본격적으로 설비 반입 등이 진행될 예정이며 파주 P10 투자계획에도 지난해 LCD 생산라인 투자 검토에서 OLED TV용 패널 생산라인 투자를 진행하고 있는 것으로 확인됨에 따라 OLED TV 시장은 2022년 5,6 B달러 규모로 성장할 전망이다.

最近、UBI Researchが発行した『AMOLED製造・検査装置産業レポート』では、Samsung Displayが開発を始めたQD-OLEDへの投資額がどれくらいなのかを分析した。

Samsung Displayが目指しているQD-OLEDは、青色OLEDから放出される光が量子ドット(Quantum Dot、QD)材料を通って緑色と赤色に分離され、RGBの3色を実現する方式で製造される。QD材料を通り抜けた光は、再びカラーフィルターを通り、さらに豊かな色を表現できるようになる。

このようなQD-OLEDの製造方式は、LG DisplayのWRGB OLEDと似ている部分が多い。まず、TFTは2社ともにOxide TFTを使用している。WRGB OLEDは青色が2回塗布され、その間に赤色と緑色が蒸着される。それに比べ、QD-OLEDは青色材料のみ2回蒸着して製造される。蒸着用マスクは、両方ともオープンマスク(Open Mask)を使用する。

QD-OLEDとWRGB OLEDのカラーフィルターの製造費は同様であると考えられるが、QD-OLEDの場合、QD材料をコーティングする装置を追加導入しなければならない。

本レポートによると、モジュールとセル、封止、蒸着装置は、同じ装置が使用される可能性があり、投資額もほぼ同様になると予想される。しかし、WRGB OLEDは背面発光方式のため、TFTを含めたバックプレーンを製造する際に同時に形成される反面、QD-OLEDは前面発光方式のため、上部のガラス基板にカラーフィルターを個別に形成し、その上に再度QD層をパターニングして製造する。その結果、QD-OLEDにはWRGB OLEDより高い投資額が必要となる。

第8世代の26Kを基準に投資額を計算してみると、QD-OLEDは11億米ドルで、10億7,000万米ドルのWRGB OLEDに比べて1.03倍高くなることが見込まれる。一方、JOLEDが事業化を進めている印刷方式OLEDの製造に必要な投資額は8億8,000万米ドルで、QD-OLEDの80%程度になるとみられる。

Daejeong Yoon(ydj7211@ubiresearch.com)

<KOLON Industries(左)とSKC(右)の透明PIフィルム、参考:KOLON Industries>

<KOLON Industries(左)とSKC(右)の透明PIフィルム、参考:KOLON Industries>

Foldable OLEDの量産が今年末に開始されると期待される中で、Foldable OLEDの主要材料の一つであるカバーウィンドウの競争が激しくなる見込みだ。Foldable OLEDはディスプレイが折りたたれる特性から、従来のカバーウィンドウに使用されていたガラスは割れるため、続けて使用することができない。

従って、割れないカバーウィンドウとして透明PIと薄板ガラスの開発が、積極的に進められている。特に透明PIフィルムに関しては、Sumitomo Chemicalと韓国のKOLON IndustriesやSKCの競争が予想される。Sumitomo Chemicalは、Samsung Electronicsが来年発売予定のFoldableスマートフォンに採用されるFoldable OLEDカバーウィンドウ向け透明PIフィルムを供給する最初のメーカーになるという。

しかし、透明PIフィルムのカバーウィンドウは、ガラスのカバーウィンドウの硬度と外観特性を満たせないため、改善が必要な状況にある。Samsung DisplayはSumitomo Chemicalの透明PIフィルムの他にも、多くのメーカーの透明PIフィルムを検討している。

Sumitomo Chemicalの透明PIフィルムと激しく競い合っているメーカーは、韓国のKOLON IndustriesとSKCである。KOLON Industriesは約10余年前から透明PIフィルムを開発しており、現在唯一透明PIフィルム量産設備を備えているメーカーである。SKCもフィルムの製造技術力を基に、2017年末に透明PIフィルムの設備投資を行った。

他に、薄板ガラスをFoldable OLED用カバーウィンドウとして開発する動きも出ている。主要メーカーにはAsahi GlassとドイツのSCHOTTがあり、厚さ0.1mm以下の実現に向けて開発を進めている。しかし、薄板ガラスも折りたたまれた状態では、耐久性に問題があると知られている。

Foldableスマートフォンの発売時期が迫ってきている中、OLEDパネルメーカーとカバーウィンドウ材料メーカーがどのような材料と構造、特性のFoldable OLED用カバーウィンドウを採用するかに業界の関心が集まっている。

**

OLED材料メーカーのMaterial Scienceは、来月の8月から赤色プライム層材料を中国最大のOLED製造メーカーに、量産供給することを16日明らかにした。

赤色プライム層材料は、赤色を発する発光層(EML)と正孔輸送層(HTL)の間に蒸着され、発光効率を高める材料である。陰極から出た電子がEMLを過ぎてHTLまで侵入しないように防ぐことで、OLED発光効率を高くするため、OLED機器の使用時間を増やすことができる。

Material Scienceが開発した赤色プライム層材料は、2016年に中国LTOPTOと設立した合弁会社LTMSで生産して供給する予定だ。合弁パートナーのLTOPTOは、LCD用液晶とOLED原料などを生産する化学会社である。

LTMSは昨年の2017年上半期に、中国陝西省西安に量産設備を構築し、今回の契約によって8月から稼働を開始する。LTMSは現在、月産500㎏規模の生産設備を備えているが、今後、中国内のOLEDメーカーと追加供給の契約が締結されれば、月産1tまで生産設備を拡大する予定だ。月500㎏という生産能力は、第6世代OLEDの生産ライン6本(マザーガラス投入基準で月9万枚)に供給できる規模である。

UBI Researchが発行した『AMOLED Emitting Material Market Track_1Q18』によると、赤色プライム層材料市場は、2018年から2022年まで年平均成長率35%を記録し、2022年には2億4,800万米ドル規模になるとみられる。

Daejeong Yoon(ydj7211@ubiresearch.com)

삼성디스플레이에서 언브레이커블 OLED panel을 공개하여 주목받고 있다.

삼성디스플레이는 깨지지 않는 스마트폰용 패널을 개발해, 美 산업안전보건청 공인 시험기관인 UL(美 보험협회시험소, Underwriters Laboratories Inc.)로부터 인증을 받았다고 23일 밝혔다.

<삼성디스플레이의 언브레이커블 OLED, 삼성디스플레이>

삼성디스플레이는 플렉시블 OLED 패널에 플라스틱 소재의 커버 윈도우를 부착해, 기판과 윈도우 모두 깨지지 않는 완벽한 언브레이커블(Unbreakable) 패널을 완성했다.

현재 상용화된 플렉시블 디스플레이는 깨지지 않는 플라스틱 기판을 사용하지만, 유리 소재의 커버 윈도우를 부착해 강한 충격을 받을 경우 윈도우가 깨지는 문제가 발생한다.

UL에 따르면 삼성디스플레이가 개발한 언브레이커블 디스플레이는 美 국방부 군사 표준규격(US Military Standard)에 맞춰 실시한 내구성 테스트를 완벽하게 통과했다. 1.2미터 높이에서 26회 실시한 낙하 테스트에서 제품의 전면부, 측면부, 모서리 부분 모두 파손 없이 정상적으로 작동했으며, 극한의 저온(-32도)/고온(71도) 테스트에서도 문제 없이 작동했다.

특히 美 국방부 군사 표준규격보다 더 높은 1.8미터 높이에서 실시한 낙하 테스트에서도 삼성디스플레이의 언브레이커블 패널은 손상 없이 정상적으로 작동했다.

삼성디스플레이 관계자는 “최근 개발되고 있는 플라스틱 윈도우는 깨지지 않는 내구성에 유리와 흡사한 투과율과 경도를 갖추고 무게까지 가벼워 휴대용 전자기기에 특히 적합하다”며 “앞으로 언브레이커블 패널이 스마트폰은 물론 안전기준이 까다로운 차량용 디스플레이나 군사용 모바일 기기, 학습용 태블릿PC, 휴대용 게임기 등 다양한 전자제품에 활용될 것으로 기대하고 있다”고 밝혔다.

삼성관계자의 말처럼 언브레이커블 OLED가 적용될 수 있는 분야는 다양할 것으로 기대되고 있다. 하지만 커버윈도우가 glass가 아닌 film인 만큼 이미 유리에 시각과 촉각이 적응 되어있는 소비자들에게 어떤 반응을 얻을지가 관건이다. 또한 스마트폰의 경우 2~3년 간격으로 주로 교체되고 있고 커버가 깨졌을 시 디스플레이를 교체해주는 등의 교체수요도 중요하다. 하지만 언브레이커블 OLED가 상용화가 된다면 이러한 교체수요는 감소될 수 있지만 다른 한편으로는 깨지지 않는 다는점이 소비자들의 구매욕을 끄는 큰 마케팅 포인트가 될 수 있다.

언브레이커블 OLED가 적용된 제품들이 실제 시장에서 얼마만큼의 성과를 거둘 수 있을지 향후 set 업체와 display업체들의 움직임이 기대된다.

작성 : 장현준 선임(hyunjun@ubiresearch.com)

김상돈 LG Display CFO는 25일에 주최한 컨퍼런스 콜에서 “2018년 상반기를 돌아보면 전통적인 비수기 시즌과 중국 발 디스플레이 공급 증가로 인해 판가 하락으로 어려운 시장 상황이었다. 작년 하반기부터 좋지 않던 시장 상황이 올해 상반기 안정될 것으로 예상하였으나 오히려 더 빠르고 가파르게 하락하였다.”고 말했다. 하지만, 2018년 하반기는 계절적 특수성과 고객의 재고 확충 맞물려 7월부터 가격이 상승하는 모습을 보이고 있다고 밝혔다. .

하반기에 진입하여 시장의 상황이 우호적으로 변경되고 있으나 예측 불확실성으로 과거 시장과는 차이가 있으며 더욱이 앞으로 디스플레이 시장의 공급과잉이랑 비대칭 경쟁 구도는 불가피한 상황임을 전했다. 이에 대해, 시장의 변동성 확대가 예상 됨에 따라 LG Display는 하반기에도 보수적인 전략을 유지할 것임을 밝혔다.

LG Display의 2018년 2분기 매출은 5조6112억원, 영업손실은 2281억원을 기록했다. 전년 동기 대비 매출은 15% 감소했고 영업이익은 8040억원에서 지난 분기에 이어 패널 출하의 예상 대비 하회 등의 어려운 시장 상황을 반영하여 계속적으로 큰 폭 적자를 면하지 못하였다. 출하 면적은 전분기 대비 2% 증가 하였지만 면적(m2)당 판가는 4% 감소하였다.

긍정적인 지표로는 TV 패널 판가 하락이 컸으나 OLED 패널의 경쟁력 우위 포지션으로 인해 전채 패널 판가 하락은 1%에 그쳤다. 3분기에는 면적 기준 출하 큰 폭으로 증가, 업계의 재고 보충을 위해 주문 증가 예상 등 상반기 대비 시장상황이 긍정적일 것으로 보고 있다.

현재 LCD와 OLED 중소형과 대형 패널 사업 모두를 하고 있는 LG Display는 이번 컨퍼런스콜을 통해 “OLED 사업에 집중, LCD 사업은 고부가 가치에 집중” 이라는 하반기와 향후 LG Display의 전략적 방향에 대해 명확히 언급하였다.

현재 IT 산업이 역 장하고 있어 LCD 산업이 어렵지만, 좁은 베젤(Narrow Bezel) 혹은 베젤의 삭제(Borderless)등 차별화 기술을 통해 하이엔드 부분과 초대형 커머셜 고부가 가치 제품을 중심으로 사업을 진행할 것임을 전달했다.

OLED는 LG Display가 향후 현재 산업 1위 자리를 유지하고 성장하기위해 중요한 사업으로 3분기중 OLED TV는 흑자 전환을 예상하고 있으며 최근 승인이 확정된 중국 광저우의 생산라인과 파주 P10공장의 10.5세대 OLED 생산라인 투자를 앞당겨 OLED 대형 시장을 드라이브 할 것이라는 입장이다. 또한 직접적으로 시기와 특정 라인에 대한 언급은 없었지만 연내 LCD 합리화 계획을 진행하여 OLED 8.5세대 추가 생산 공장 증설 계획도 내비쳤다.

증가하는 수요에 대응해 생산 규모를 늘리고 있는 대형 OLED 사업에 비해, 힘든 시기를 겪고 있는 플라스틱 중소형 OLED 패널 사업에 대해서는 모바일과 자동차 시장을 강조하며 필요한 전략 기술로 미래 시장에 대한 준비를 진행하고 있음을 전달했다.

Apple향 생산공장으로 거론되어온 E6-1라인은 올해 4분기 양산을 시작할 것으로 언급한 것을 미루어 최근 2018년 iPhone OLED 모델에 디스플레이 공급과 관련한 사실 가능성을 짐작할 수 있는 것으로 드러났다. 또한 자동차 시장에서도 OLED 패널의 수요가 증가하고 있으며 내년 하반기 본격적인 비즈니스가 시작될 전망임을 밝혔으며 현재 수주 잔고에서 OLED 패널은 약 10% 후반 수준으로 이미 상당 부분 진행되고 있음을 확인 하였다.

마지막으로, LG Display의 미래 준비와 관련하여 경쟁사 대비 예산 부족과 펀딩 부족의 우려를 잘 알고 있으며 2020년까지 기존에 계획한 Capex에서 약 3조원 줄인 수준으로 진행할 계획이며 이 중 상당부분은 감가상각비와 내부 운전자본관리를 통해 가능하며 나머지는 차입할 계획임을 밝혔다. 시장에서 몇차례 언급된 유상증자는 검토하고 있지 않음을 확인하였으며 LG Display는 OLED의 다양한 포트폴리오를 철저히 준비하여 후발주자인 분야에서도 경쟁기업 대비 차별화를 통한 사업 성공의 의지를 밝혔다.

작성: Hana Oh (hanaoh@ubiresearch.com)

OLED材料メーカーのMaterial Scienceは、来月の8月から赤色プライム層材料を中国最大のOLED製造メーカーに、量産供給することを16日明らかにした。

赤色プライム層材料は、赤色を発する発光層(EML)と正孔輸送層(HTL)の間に蒸着され、発光効率を高める材料である。陰極から出た電子がEMLを過ぎてHTLまで侵入しないように防ぐことで、OLED発光効率を高くするため、OLED機器の使用時間を増やすことができる。

Material Scienceが開発した赤色プライム層材料は、2016年に中国LTOPTOと設立した合弁会社LTMSで生産して供給する予定だ。合弁パートナーのLTOPTOは、LCD用液晶とOLED原料などを生産する化学会社である。

LTMSは昨年の2017年上半期に、中国陝西省西安に量産設備を構築し、今回の契約によって8月から稼働を開始する。LTMSは現在、月産500㎏規模の生産設備を備えているが、今後、中国内のOLEDメーカーと追加供給の契約が締結されれば、月産1tまで生産設備を拡大する予定だ。月500㎏という生産能力は、第6世代OLEDの生産ライン6本(マザーガラス投入基準で月9万枚)に供給できる規模である。

UBI Researchが発行した『AMOLED Emitting Material Market Track_1Q18』によると、赤色プライム層材料市場は、2018年から2022年まで年平均成長率35%を記録し、2022年には2億4,800万米ドル規模になるとみられる。

LG Display가 7월 25일에 진행한 2018년 2분기 실적발표에서 파주 10.5세대 공장(P10)에서 대면적 LCD가 아닌 대면적 OLED를 우선 생산키로 한 방침을 확정했다.

LG Display는 이날 대형 OLED 사업이 안정화를 띔에 따라 생산에 속도를 올려 실적 부진을 만회하겠다는 전략을 밝혔다. 김상돈 LG Display CFO는 “내년 400만대, 2020년 700만대, 2021년 1000만대 판매 목표를 가지고 있다”고 언급하며, 중국 광저우 8.5세대 공장이 내년 하반기 가동을 시작하고 LCD 공장까지 OLED 공장으로 전환하면 OLED TV 패널 생산량이 빠르게 증가할 것으로 기대했다.

대면적 LCD 대신 대면적 OLED로의 사업 집중에 따라, 대면적 OLED와 관련된 발광재료 업체들의 실적 개선도 기대된다. 현재 LG Display의 대면적 OLED용 재료를 공급하는 업체로는 Merck와 Noveled, LG Chemical, Heesung Material, Idemitsu Kosan 등이 있다.