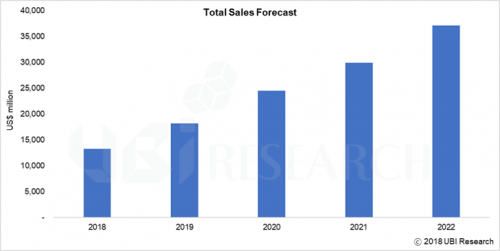

In the 2018 OLED material and component report and Market Track published by UBI Research, the entire market for OLED materials and components market is expected to grow at a CAGR of 29% by 2022, forming a market of US$ 37 billion in 2022.

<Market forecast for OLED materials and components>

The overall OLED material and component market forecasted in this report is calculated based on the panel makers’ available capacity and includes all the materials and components for OLED production.

The total OLED material and component market is counted as US$ 9,794 million in 2017 and is expected to grow by 35% to US$ 13,264 million in 2018.

Major growth drivers are mentioned as capacity expansion of Samsung Display and LG Display inclusive of Gen6 flexible OLED mass production lines of Chinese panel makers.

UBI Research commented “Utilization of Samsung Display in the first quarter of 2018 was poor, but it is turning to normal from the second quarter, and LG Display and Chinese panel makers are also aiming to mass-produce this year. In particular, it will have a major impact on the growth of the materials and components market in 2018 whether Samsung Display’s A4, LG Display’s E5, E6 and BOE’s B7 lines will be in full operation.”

In the 2018 OLED material and component report, the market is forecast for 20 kinds of major materials and components used in OLED for mobile devices and large-area OLED, including substrate glass, carrier glass, PI and organic materials for TFT. In addition, the report covers industry trends and key issues related to the core materials, while Market Track forecasts the expected purchase volume and purchase amount by panel makers.

In the 2018 OLED material and component report and Market Track published by UBI Research, the entire market for OLED materials and components market is expected to grow at a CAGR of 29% by 2022, forming a market of US$ 37 billion in 2022.

<Market forecast for OLED materials and components>

The overall OLED material and component market forecasted in this report is calculated based on the panel makers’ available capacity and includes all the materials and components for OLED production.

The total OLED material and component market is counted as US$ 9,794 million in 2017 and is expected to grow by 35% to US$ 13,264 million in 2018.

Major growth drivers are mentioned as capacity expansion of Samsung Display and LG Display inclusive of Gen6 flexible OLED mass production lines of Chinese panel makers.

UBI Research commented “Utilization of Samsung Display in the first quarter of 2018 was poor, but it is turning to normal from the second quarter, and LG Display and Chinese panel makers are also aiming to mass-produce this year. In particular, it will have a major impact on the growth of the materials and components market in 2018 whether Samsung Display’s A4, LG Display’s E5, E6 and BOE’s B7 lines will be in full operation.”

In the 2018 OLED material and component report, the market is forecast for 20 kinds of major materials and components used in OLED for mobile devices and large-area OLED, including substrate glass, carrier glass, PI and organic materials for TFT. In addition, the report covers industry trends and key issues related to the core materials, while Market Track forecasts the expected purchase volume and purchase amount by panel makers.

유비리서치에서 발간한 2018 부품소재 산업 보고서와 마켓트랙에서는 OLED 전체 부품소재 시장이 2022년까지 연평균 29%로 성장하여 US$ 37,000 million의 시장을 형성할 것으로 전망했다.

<OLED 부품소재 시장 전망>

본 보고서에서 전망한 전체 OLED 부품소재 시장은 panel 업체의 공급가능 물량 기준으로 산출되었으며 OLED에 들어가는 모든 부품소재를 포함한 수치이다.

전체 OLED 부품소재 시장은 2017년 US$ 9,794 million으로 집계되었으며 2018년은 35% 성장한 US$ 13,264 million로 전망된다.

주요 성장요인으로는 삼성디스플레이와 LG Display, 중국 panel 업체들의 Gen6 flexible OLED 양산라인 capa 증가를 꼽았다.

유비리서치는 “1사분기 삼성디스플레이의 가동률은 저조한 편이었지만 2사분기부터 정상화로 돌아서는 추세이며, LG Display와 중국 panel 업체들도 올해 본격적인 양산을 목표로 하고 있다. 특히 삼성디스플레이의 A4와 LG Display의 E5, E6, BOE의 B7라인의 정상가동 여부가 2018년 전체 부품소재 시장 성장여부에 큰 영향을 미칠 것으로 예상된다.”라고 밝혔다.

이번에 발간된 2018 부품소재 산업 보고서에서는 기판용 유리와 carrier 유리, PI, TFT용 유기재료 등을 비롯하여 모바일과 대면적 OLED에 사용되는 핵심 부품소재 20종에 대해 시장 전망하고 있다. 또한 보고서에서는 핵심소재들에 대한 산업동향과 주요 이슈들을 다루고 있으며 마켓트랙에서는 panel 업체별 예상 구매량과 구매금액을 전망하고 있다.

국내 한 벤처기업이 일본 업체가 특허를 독점하고 있는 유기발광다이오드(OLED)용 청색도판트(dopant)를 개발하는 데 성공했다. 도판트는 OLED 내에서 실제로 색을 내는 호스트(host)에 섞어 효율⋅수명을 개선해주는 소재다.

그동안 OLED용 호스트를 개발한 국내 재료 업체는 많았지만, 도판트를 대기업의 지원을 받지 않은 벤처회사가 독자적으로 상용화 수준까지 개발한 사례는 처음이라는 점에서 개가로 평가된다.

OLED용 유기재료 개발업체 머티어리얼사이언스(대표 이순창)는 일본 I사 청색 도판트 특허를 대체할 수 있는 기술을 개발했다고 7일 밝혔다. 지난 2014년 설립된 머티어리얼사이언스는 국내외 OLED 패널 업체에 정공수송층(HTL)·전자수송층(ETL) 등을 공급하고 있다. 총 50여명 임직원 중 절반이 연구개발 인력이다. 지난해 매출은 66억원, 올해는 100억원을 돌파할 것으로 예상된다.

이번에 머티어리얼사이언스가 청색 도판트를 개발함에 따라 OLED 패널 업체들은 I사 외에 청색 호스트 및 도판트를 공급해 줄 수 있는 대안을 갖게 됐다.

일본 I사는 지난 1995년부터 청색 도판트를 개발해왔다. 현재 총 30건 이상(일본 출원 기준)의 청색 관련 특허를 보유하고 있으며, 이 중 8개의 주요 특허는 오는 2034년까지 유효하다.

특히 안트라센(벤젠 고리 세 개가 차례로 접합된 화합물) 구조로 된 청색 호스트와 파이렌을 포함하는 청색 도판트가 조합하는 방식에 대한 특허를 독점하고 있다. 이 때문에 I사 청색 도판트를 구매하는 패널 업체는 반드시 호스트까지 I사 재료를 구매해야만 한다. I사 청색 도판트에 다른 업체 호스트를 섞어 쓸 경우 호스트 물질이 안트라센 골격이면 특허 침해가 불가피하다.

삼성⋅LG디스플레이 모두 I사 청색 도판트 및 호스트를 사용하여 왔다.

머티어리얼사이언스가 개발한 청색 도판트는 I사 조합특허를 완전히 벗어나도록 분자를 설계하였다. 기존에는 OLED의 효율⋅수명을 개선하며 진청색을 얻기 위하여 강력한 전자 받개(electron acceptor)를 분자에 적용하는 방식을 사용하여 왔다.

머티어리얼사이언스는 반대로 전자 주개(electron donor)를 분자에 도입하여 효율과 수명을 개선하면서 진청색 구현을 실현하였다. 이 도판트는 주위의 극성에 따른 발광 파장이 변화되는 용매의존발색현상(solvatochromism)을 크게 감소 시킴으로 호스트의 극성에 따라 발광 파장이 변화하는 현상도 크게 줄었다.

정재호 머티어리얼사이언스 연구원은 “새로운 구조 및 합성 방법을 개발해 기존 도판트와 차별화된 제품을 생산했다”며 “패널 업체들이 다양한 종류의 청색 호스트를 활용할 수 있을 것”이라고 설명했다. 머티어리얼사이언스는 최근 OLED 패널 업체들이 청색 형광체 수명을 늘리기 위해 도입을 추진 중인 열활성화지연형광(TADF) 기술도 개발하고 있다.

<발광재료 시장 전망, 유비리서치>

유비리서치에 따르면 OLED 유기재료 시장은 2021년까지 33억6000만달러(약 3조8000억원) 규모로 성장할 전망이다. 이 중 청색 재료의 매출 비중은 11.5%를 차지한다.

A Korean venture company has succeeded in developing blue dopant for Organic Light Emitting Diodes (OLED) that a Japanese company has had its exclusive patent for. The dopant is an element that improves efficiency and life time by mixing with host that actually colors within the OLED.

In the meantime, many domestic material companies have developed OLED host, but it is the first case that a venture company has independently developed dopant on a commercial scale without receiving any support of large corporations.

Material Science (CEO Lee Soon-chang), an organic material developer for OLED has developed a technology that can replace Japanese I Company’s patent for blue dopant. Established in 2014, Material Science is supplying HTL( Hole Transporting Layer) and ETL (Electron Transfer Layer) to OLED panel makers.

Half of the 50 employees are R&D personnel. Last year, its sales were 6.6 billion won, and it is expected to exceed 10 billion won this year.

This time, due to the development of blue dopant by Material Science, OLED panel companies have an alternative to supply blue host and dopant besides I Company.

Japanese I Company has been developing blue dopant since 1995. At present, the company has more than 30 patents related to blue dopant (based on Japanese application for a patent), and its major 8 patents are valid until 2034. In particular, it has an exclusive patent for the combination method of blue dopant that includes blue host and pyrene with an anthracene structure (a compound in which three benzene rings are sequentially bonded). For this reason, the panel makers which purchase dopant from I Company must buy its host. If they mix I Company’s blue dopant with another company’s host, it is inevitable to infringe the patent in the case a host material has an anthracene skeleton.

Both Samsung Display and LG Display have been using I Company’s blue dopant and host.

The blue dopant developed by Material Science is designed to make molecules that are completely out of I Company’s compound patent. Conventionally, the method of applying an electron acceptor to a molecule has been used to improve the efficiency and lifetime of OLED and have a blue color.

On the other hand, Material Science introduces electron donor into molecules to improve the efficiency and lifetime while generating dark blue color. This dopant greatly reduces the solvent-dependent color development (solvatochromism) where emission wavelength changes due to the polarity of the surroundings. Therefore, the change of emission wavelength is also greatly reduced.

Jung Jae-ho, a researcher at Material Science said, “We have developed a new structure and a synthesis method, which makes it possible to produce its differentiated dopant.” “Panel companies are now able to utilize various types of blue hosts”. In addition, Material Sciences has been recently developing TADF(Thermally Activated Delayed Fluorescence) that OLED panel makers are struggling to introduce for the longer life of blue-emitting phosphors.

<OLED emitting material market forecast, UBi Research>

According to UBi Research, the OLED organic market is expected to reach $ 3.36 billion by 2021 (about 3.8 trillion won). And blue materials account for 11.5% of total sales.

![]()

CYNORA, a leader in TADF (thermally activated delayed fluorescence) materials for OLEDs, has reached new performance records with its newest blue emitter material. With the current performance, the company is getting close to commercialization of its first product by the end of 2017.

Despite urgent requests by the OLED display panel makers for a high-efficiency blue emitter material in the last few years, no material supplier has yet been able to produce such a material. High-efficiency blue emitters are needed to reduce power consumption and increase the display resolution further. At SID 2017, CYNORA presented a blue emitter with a performance that was very close to the requirements of the panel makers. Using TADF technology, the company has achieved 15% EQE at 1000 cd/m² with an emission peak at < 470 nm and a LT97 of > 90 hours (at 700 cd/m²) on a device level.

“CYNORA’s latest patent-protected materials show a performance in the range of the customer´s specifications for blue” said Thomas Baumann, CYNORA´s CSO, “This is the best overall performance of a high-efficiency blue emitter so far from what CYNORA has seen. In the finalization of CYNORA’s product development, CYNORA will now focus on moving the emission peak slightly towards 460 nm.”

“CYNORA’s progress in the last few months makes us very confident that CYNORA can commercialize CYNORA’s first highly efficient blue emitter by the end of this year, as planned” said Andreas Haldi, CMO at CYNORA. “But CYNORA’s goal is to become a leading OLED material supplier by providing emitters of all display colors. Therefore, CYNORA is planning to follow up on the blue emitter with a green emitter by 2018 and a red emitter by 2019.”

Source = UDC

Hyunjoo Kang / jjoo@olednet.com

Universal Display Corporation( UDC ), enabling energy-efficient displays and lighting with its Universal PHOLED technology and materials, today reported financial results for the second quarter ended June 30, 2016.

For the second quarter of 2016, the Company reported net income of $21.8 million, or $0.46 per diluted share, on revenues of $64.4 million. This includes $1.8 million of currency exchange loss related to the BASF OLED patent acquisition. For the second quarter of 2015, the Company reported a net loss of $11.8 million, or $0.25 per diluted share, on revenues of $58.1 million. The 2015 net loss reflected a $33.0 million write-down of inventory, primarily of an existing host material and associated work-in-process. Excluding this item and its associated $1.9 million reduction of income tax expense, adjusted net income for the second quarter of 2015 was $19.4 million, or $0.41 per diluted share (see “reconciliation of non-GAAP Measures” below for further discussion of the non-GAAP measures included in this release).

“Our second quarter 2016 revenues and net income increased year-over-year, and we maintained our strong margin profile. We are confident that the underlying growth fundamentals of our long-term outlook remain robust, but near-term, we expect our revenue growth will be delayed by about six months,” said Sidney D. Rosenblatt, Executive Vice President and Chief Financial Officer of Universal Display.

Rosenblatt continued, “We expect strong revenue growth in 2017. At that time, new OLED production from the multi-year capital expenditure cycle is slated to start contributing to our revenues. Ahead of this wave of high-volume capacity, we have been working to expand and broaden our team and core competencies to advance our strategic initiatives and increase our competitive edge. We expect these initiatives, along with new OLED capacity, coupled with our pipeline of new materials, new technologies and new agreements, to bolster our long-term growth plan.”

Financial Highlights for the Second Quarter of 2016

The Company reported revenues of $64.4 million, compared to revenues of $58.1 million for the same quarter of 2015, an increase of 10.8%. Material sales were $22.3 million, down 8.3% compared to the second quarter of 2015, primarily due to a $2.0 million decline in host material sales. Royalty and license fees were $42.0 million, up from $33.7 million in the second quarter of 2015. The Company recognized $37.5 million in Samsung Display Co., Ltd. (SDC) licensing revenue in the second quarter of 2016, up from $30.0 million in the same quarter of 2015.

The Company reported operating income of $34.0 million in the second quarter of 2016, compared to an operating loss of $4.8 million for the second quarter of 2015. Excluding the inventory write-down of $33.0 million, adjusted operating income was $28.2 million for the second quarter of 2015. Operating expenses were $30.4 million, compared to $62.9 million in the second quarter of 2015 and cost of materials was $5.7 million, compared to $39.1 million in the second quarter of 2015, both of which included the inventory write-down of $33.0 million in the second quarter of 2015.

The Company’s balance sheet remained strong, with cash and cash equivalents and investments of $332.0 million as of June 30, 2016. During the second quarter, the Company added $96.0 million in intangible assets in the form of intellectual property purchases and certain other assets from BASF, increasing the portfolio to more than 4,100 issued and pending patents worldwide. During the second quarter, the Company generated $36.2 million in operating cash flow.

Financial Highlights for the First Six Months of 2016

The Company reported revenues of $94.1 million, compared to revenues of $89.3 million for the first half of 2015, or an increase of 5.4%. Material sales were $46.6 million, down 8.8% compared to $51.1 million in the first half of 2015, primarily due to a $7.0 million decline in host sales. Royalty and license fees were $47.4 million, up from $38.1 million in the first half of 2015.

The Company reported operating income of $36.7 million in the first half of 2016, compared to an operating loss of $3.1 million for the first half of 2015. Excluding the inventory write-down of $33.0 million, adjusted operating income was $30.0 million for 2015. For the first half of 2016, we reported net income of $23.8 million, or $0.51 per diluted share, compared to a net loss of $10.5 million, or $0.23 per diluted share, for the same period of 2015. Excluding the inventory write-down and the associated $1.9 million reduction of income tax expense, adjusted net income was $20.7 million, or $0.45 per diluted share, for the first half of 2015.

Operating cash flow for the first half of 2016 was $36.2 million, a decrease of 51.8% compared to $75.2 million for the first half of 2015 which included an upfront $42.0 million license and royalty payment.

2016 Guidance

While the OLED industry is still at a stage where many variables can have a material impact on its growth, based upon the most recent and best information on hand, the Company believes it is prudent to revise its 2016 revenues guidance. The Company now expects 2016 revenues to be in the range of $190 million to $200 million.

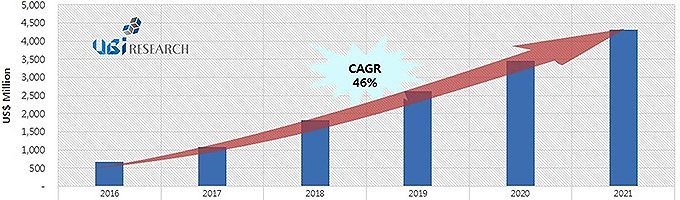

OLED Emitting Materials Market Forecast, Source: UBI Research’s 2016 OLED Emitting Materials Annual Report

Hyunjoo Kang / Reporter / jjoo@olednet.com

This year’s global OLED emitting materials market is expected to record US$ 677 million, approximately a 16% increase compared to 2015.

According to 2016 OLED Emitting Materials Annual Report, published by UBI Research, the global OLED emitting materials market is to grow at CAGR of 46%, and record US$ 4,323 million in 2021. The reasons for continued rapid growth include AMOLED equipped smartphone and large area OLED panel mass production increase. AMOLED panel equipped Galaxy S7 series is expected to be a hit this year, and AMOLED application of mainstream Galaxy series is also expected to increase compared to last year.

Furthermore, LG Display is planning to greatly increase this year’s large area OLED panel production. Chinese panel companies are also to actively begin AMOLED panel mass production from this year. Accordingly, the amount of OLED materials entering the global display market will increase.

The global demand for OLED emitting materials in 2016 is estimated to be approximately 38 tonnes. Of this, the amount expected to be used in Korea is approximately 36 tonnes, about 93% of the total demand. Basically, just the amount used by the 2 Korean OLED panel companies, Samsung Display and LG Display, is 93% of the global market. 64% of the total demand is Samsung Display, and 29% is LG Display.

In terms of revenue, of this year’s US$ 677 million, Samsung Display and LG Display are expected to occupy 94%.

As key Chinese panel companies, including BOE, are carrying out or planning AMOLED mass production line, China’s emitting materials demand is estimated to increase from 2017. Accordingly, of global OLED demand, China’s proportion is expected to increase each year, and Korea’s to decrease.

OLED Emitting Material 시장 전망(출처=유비산업리서치 2016 Emmiting Materials Annual Report)

강현주 기자 / jjoo@olednet.com

올해 글로벌 OLED 발광재료( Emitting Material ) 시장은 전년대비 약 16% 성장한 미화 6억7700만 달러(한화 약 7700 억원) 규모를 형성할 전망이다.

유비산업리서치가 발간한 ‘2016 OLED 발광재료 보고서(2016 OLED Emitting Materials Annual Report)’에 따르면 2016년부터 전세계 OLED 발광재료 시장은 연평균 46%의 성장률을 그리며 2021년 43억2300만 달러(한화 약 4조 9250억 원) 규모에 달할 것으로 예상된다.

이처럼 OLED 발광재료 시장이 고성장을 지속하는 요인에는 AMOLED 장착 스마트폰 및 대면적 OLED 패널 양산 증가 등이 있다.

올해 AMOLED 패널을 장착한 갤럭시 S7 시리즈의 흥행이 예상될 뿐 아니라 보급형 갤럭시 시리즈의 AMOLED 적용도 지난해보다 증가할 예정이다.

LG Display에서도 올해 대면적 OLED panel 생산을 2015년보다 크게 늘릴 계획이다. 중국의 패널 업체들도 2016년부터 본격적인 AMOLED 패널 양산에 돌입할 예정이다.

이에 따라 전세계 디스플레이 시장에 투입되는 OLED 발광재료의 양도 늘어나게 된다.

2016년 전세계에서 사용될 OLED 발광재료 수요는 약 38 톤으로 관측된다. 이 중 한국에서 사용될 것으로 예상되는 OLED 발광재료양은 전체 수요의 93%에 달하는 약 36 톤에 이를 전망이다.

한국의 두 OLED 패널 제조사인 삼성디스플레이와 LG디스플레이가 사용하는 양만 전세계 93%라는 얘기다. 삼성디스플레이가 전체 수요의 64%, LG디스플레이가 29%의 비중이다.

금액 기준으로는 올해 시장 규모 6억7700만 달러 중 삼성디스플레이와 LG디스플레이가 차지하는 비중은 94%에 이를 것으로 예상된다.

BOE 등 주요 중국 패널 업체들도 AMOLED 양산라인 투자를 진행 또는 계획하고 있어 2017년부터는 중국의 발광재료 수요가 늘어날 예정이다. 이에 따라 글로벌 OLED 발광재료 수요 중 중국의 비중은 해마다 늘어나고 한국의 비중은 줄어들 전망이다.

Source : UDC

Hyunjoo Kang / Reporter / jjoo@olednet.com

UDC (Universal Display) that is dominating the global OLED emitting materials market, recorded 11% reduced OLED emitting materials revenue in 2015 compared to 2014. Despite the decreased revenue, it maintained its top place in the market.

According to 2016 OLED Emitting Material Annual Report, published by UBI Research, UDC recorded approximately $ 113 million in 2015 OLED emitting materials revenue. In 2014, this company’s OLED emitting materials revenue recorded $ 127 million and led the global market, and maintained its position in 2015.

In particular, this company is a dominating presence in dopant materials sector. In 2015, UDC occupied 82% of the dopant materials sector, and the rest of the companies share the remaining 18%. Based on the phosphorescent patents, it is supplying phosphorescent red and green dopant to Samsung Display and LG Display.

Following UDC’s top place in 2015 global OLED emitting materials market in terms of revenue, Idemitsu Kosan ranked 2nd, and this was followed by Novaled, Dow Chem., and Samsung SDI. In 2013, Dow Chem. was at the top of the market, but since 2014 UDC overtook the leadership. In 2016, LG Display’s OLED TV mass production line operation rate, materials structure of Galaxy Note series to be mass produced in H2, and other factors are expected to affect the OLED emitting materials market.

UDC is scheduled to announce 2016 Q1 performance on 5 May (local time).

By Choong Hoon Yi

At 2015 OLED Evaluation Seminar (December 4) hosted by UBI Research, Sung-Kee Kang, DS Hi-Metal’s CSO, reported that OLED display market has to expand through OLED TV and new applications in order for OLED emitting materials companies to grow.

Presenting under the title of ‘OLED Organic Material Technology, Industry Trend’, Kang introduced the current OLED emitting material value chain. He explained that within OLED emitting materials market, there are too many players considering the current volume and overall OLED display market expansion is a necessity. However, he added that for OLED display to compete against LCD display, OLED TV market has to expand successfully, and new application that utilizes OLED’s characteristics is needed.

In order to expand the market, development of OLED emitting materials and other materials is urgently in demand that meet the required conditions. Kang emphasized that at present new technology seeds promotion for the next OLED is needed as well as development of OLED emitting materials, and other flexible/transparent related materials with new functions.

Considering LG’s active OLED TV marketing, Apple’s interest in OLED panel application, and possibility for Samsung to apply AMOLED to all models among others, OLED market is anticipated to rapidly grow. Together with this, the industries of OLED emitting material and component/other materials with new functions are also expected to considerably grow.

유비산업리서치가 개최한 ‘2015 OLED 결산 세미나’에서 덕산 네오룩스 CSO 강성기 전무는 OLED용 발광 재료 업체들이 성장하기 위해서는 OLED TV와 새로운 어플리케이션을 통한 OLED 디스플레이 시장 확대가 되어야 한다고 발표했다.

강성기 전무는 ‘OLED용 유기소재 기술, 산업 동향’이라는 주제로 발표하면서 현재 OLED 발광 재료 value chain을 소개했다. 이에 강 전무는 ‘OLED 발광 재료 시장은 현재 규모에 비해 player가 많아서 전반적인 OLED 디스플레이 시장 확대가 필수적’이라고 강조했다. 하지만 OLED 디스플레이가 LCD 디스플레이에 경쟁력을 갖추기 위해서는 OLED TV시장이 성공적으로 확대되어야 하며, OLED의 특징을 활용한 새로운 어플리케이션 시장 창출이 필요하다고 덧붙였다.

OLED 시장을 확대하기 위해서는 OLED TV와 flexible, transparent등에 필요한 요구 조건을 갖추고 있는 OLED용 발광 재료와 부품 소재의 개발이 시급하다. 강성기 전무는 ‘지금은 OLED용 발광 재료, flexible/transparent관련 신 기능 소재 개발과 함께 Next OLED를 위한 신기술 seeds 육성이 필요한 상황’이라고 강조하였다.

LG의 본격적인 OLED TV 마케팅과 Apple의 OLED panel 적용에 대한 관심, Samsung 스마트폰의 전모델 AMOLED 적용 가능성 등 앞으로 OLED 시장이 급격히 성장할 것으로 기대되는 가운데 OLED 발광재료와 신기능 부품/소재 산업 또한 크게 성장할 것으로 기대된다.

지난 9월 30일(현지시간), 듀폰디스플레이는 대면적에 적용할 수 있는 용액공정용 OLED 재료에 대한 생산시설 규모를 늘리고 가동을 시작했다고 발표했다.

듀폰의 OLED재료는 OLED 디스플레이를 더 밝고, 더 선명하고, 지속 시간도 길면서 현재 OLED TV 패널보다 저렴하게 개발할 수 있도록 설계되었다. 새로 가동을 시작한 시설은 듀폰의 본사 소재지 미국 Wilmington 근처인 Newark의 DuPont Stine-Haskell 연구센터에 있다.

듀폰디스플레이의 글로벌 사업부장인 Avi Avula는 “OLED 재료는 OLED TV 성능에 매우 중요한 요소이다. 듀폰이 현재 시장에서 가장 뛰어난 용액공정 OLED 재료를 가지고 있다.”고 말했다. 또한 “우리의 비전은 OLED가 디스플레이의 표준이 되는 것이고, 이를 실현시키기 위해서는 2020년까지 대면적 OLED TV용 패널단가를 $ 1,000 이하로 생산하는 것에 초점을 맞추고 있다.”고 덧붙였다.

한편 듀폰디스플레이는 올해 용액공정 재료 성능으로 red 효율은 22 cd/A, green은 70 cd/A, blue는 5.5 cd/A를 표했으며, 이는 증착 재료에 비해 각각 76%, 82%, 11% 수준이다.

On 30 September (local time), DuPont Displays announced the opening of a state-of-the-art, scale-up manufacturing facility designed to deliver production scale quantities of advanced materials that enable large-format, solution-based printed OLED displays.

These materials are designed to help manufacturers develop OLED displays that are brighter, more vivid, longer lasting and significantly less expensive than the OLED TVs on the market today. The facility is located at the DuPont Stine-Haskell Research Center (Stine-Haskell) in Newark, Del., near DuPont’s global headquarters in Wilmington, US.

DuPont’s new scale-up facility is sized to meet the future growth expectations of the OLED TV industry, which analysts predict will increase by over 70 percent for the next several years and will require large quantities of highly sophisticated OLED materials. This new OLED facility at Stine-Haskell has large-scale formulation systems and can support simultaneous production of multiple product lines.

“Materials are critical to the performance of an OLED TV and we are confident that DuPont has the best performing solution OLED materials available in the market today,” said Avi Avula, global business director, DuPont Displays. “Our vision is that OLEDs will become the display standard and to make that vision a reality, we are focused on helping our customers bring the cost of large sized OLED TVs down to less than $1000 by 2020.”